On July 15 (Wednesday), Canada’s central bank AKA Bank of Canada (BoC) cut overnight rate by 25 basis points (bps) from 0.75% to 50%. This is the second rate-cut this year. First rate-cut took place in January. Not only rate-cut, but lower growth forecasts.

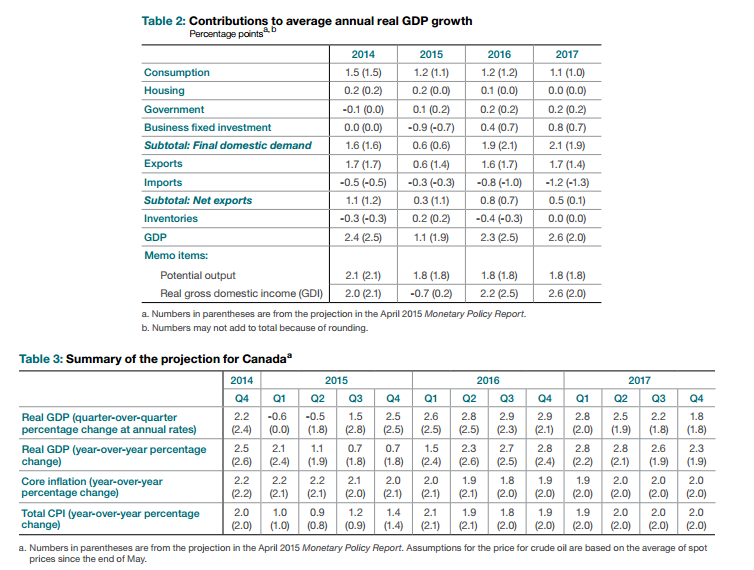

BoC expects Gross Domestic Product growth to be 1.1% year-over-year (Y/Y) this year, down from its 1.9% forecast in April. Policy makers said that Gross domestic product probably “contracted modestly” in the first half. However, they did not call it recession. ‘‘The lower outlook for Canadian growth has increased the downside risks to inflation,’’ policy makers said.

Bank also reduced the net exports contribution to GDP by 0.8% to 0.6% from 1.4%. A stronger U.S. economy and a weaker Canadian dollar should contribute to higher export growth.

There has been a big shift in the inflation tone over the past few months:

April: “Risks to the outlook for inflation are now roughly balanced”

May: “the Bank’s assessment of risks to the inflation profile has not materially changed”

This time (July): “The lower outlook for Canadian growth has increased the downside risks to inflation”

“The Bank anticipates that the economy will return to full capacity and inflation to 2 per cent on a sustained basis in the first half of 2017.” In the April’s forecasts, the bank expected the economy to return to full capacity at the end of 2016. I can tell that the Bank is running scared.

Damages from low oil prices has been extensive. Canada is the world’s fifth-largest oil producer and lower oil prices will definitely not help the economy. The damages from lower oil prices shrank the economy in the first half of the year.

Recently after Iran deal has been reached, oil prices fell sharply. It’s currently trading around $48. If the the deal is finalized, it won’t be very good for Canada economy since Iran might want to double its oil production, leading to much lower oil prices.

The bank also said “Additional monetary stimulus is required at this time to help return the economy to full capacity and inflation sustainably to target.” If conditions get worse, they will cut rates again.

Oil is not the only problem for Canada. Other concerns are potential bubbles in housing and consumer debt.

According to BoC’s Monetary Policy Report (June), “the vulnerability associated with household indebtedness remains important and is expected to edge higher in the near term in response to the ongoing negative impact on incomes from the sharp decline in oil prices and a projected increase in the level of household debt.” (Page 30).

Over the past few years, housing prices in Canada have skyrocketed. Lower borrowing costs will just add fuel to the fire (DEBT + HIGH PRICES IN HOUSING MARKET WITH LOW INTEREST RATES = NOT A GOOD COMBINATION) . There just might be a bubble in the housing market. But, BoC does not think so.

The next BoC meeting is on September 9th, about a week before the U.S. Federal Reserve meeting, the day that many believe lift-off from the zero interest rate policy will take place. CPI and non-farm payrolls data for July and August will decide whatever the Fed will hike or not.

Rate-cuts and plunging commodity prices, especially crude oil, has caused sell-off in Loonie. Ever since the first rate-cut of the year (January), Loonie (CAD) has weakened significantly. With strengthening dollar (USD), USD/CAD has skyrocketed. When looked at monthly chart, USD/CAD has developed ‘Cup and Handle’ formation. While this is a sign to short USD/CAD, I would be very careful because fundamentals for CAD are too weak. If I were to short it, I would put my stop above the resistance line (Bold Red line).