This article was initially posted on The Ticker, Baruch College’s (the college I currently attend) independent, student-run newspaper.

After a defeat in a constitutional reform referendum, Italian Prime Minster Matteo Renzi has resigned as he previously promised in case of a “no” vote to the constitutional revision plan. This referendum was meant to strengthen Renzi’s hand by stripping the Senate of its many legislative powers and speeding up the decision-making process.

With 59.1 percent of the votes being “no,” an anti-establishment political force took control once again, following the example of the Brexit referendum and Donald Trump’s election. Renzi, a centrist, was accused of failing to restart the country’s flagging economy, which has barely grown since adopting the euro in 1999.

The referendum raises questions about Italy’s ability to work efficiently. Since 1946, Italy has had 41 different prime ministers and has gone through repeated political turmoils.

In response to the referendum, Brexit campaign leader Nigel Farage, who is also a vocal supporter of Donald Trump, tweeted, “This vote looks to me to be more about the euro than constitutional change.”

Parallel to Brexit and Trump’s victory, the Italian referendum showed voters the rhetoric of populist parties like the Five Star Movement, which campaigned against the constitutional reforms.

Renzi’s collapse comes after the defeat of a far-right candidate in Austria. It is a blow to the wave of anti-establishment anger across the western countries. Norbert Hofer, a far-right candidate from the Freedom Party of Austria, lost by seven points to independent candidate Alexander Van der Bellen. While the far-right may have lost this election, the rise of populism is gaining the support of the Freedom Party for the next national election in Austria, set to be held before spring 2018.

Matteo Salvini, the leader of Italy’s far-right Northern League, tweeted, “Viva Trump, viva Putin, viva la Le Pen e viva la Lega!” which translates to “Long live Trump, long live Putin, long live Le Pen and long live the Northern League!”

In addition to supporting the Trump presidency, the Five Star Movement and the Northern League favor rougher immigration policies. Both parties have promised to hold a referendum on Italy’s membership in the eurozone and renegotiate Italy’s public debt.

Markets have mostly cooled off from the aftershocks of the Brexit and the Italian referendum results, but elections in several key European countries next year’s might not make recovery easy for investors. Renzi’s departure could lead to an early election.

Italy is now another country on the list of European Union members that are likely to hold a general election in 2017, joining France, Germany, Netherlands and the United Kingdom.

Italy’s election would be held in early 2017. The potential victory of the populist party will create uncertainty about the economic prospects of the eurozone’s third biggest member state.

Italy’s banking sector, currently with $4 trillion in assets, is suffering from low profitability, lack of economic growth, ultra-low interest rates and a surplus of bad loans. The FTSE Italia All-Share Banks Sector Index is also down 51 percent over the past year. A change in the government could mean further delays in solutions to the banks’ problems.

Banca Monte dei Paschi di Siena — the world’s oldest and Italy’s third largest bank — recently failed the EU bank stress test.

The bank’s stock is down 83 percent since 2007 as bad loans progressively increase. The bank is now desperately looking to raise capital and sell 28 billion euros in bad loans.

The only solution Italy has at this moment is to “rely on the EU to provide more fiscal rescue packages, to prevent Monte Dei Paschi from becoming insolvent,” said Kenneth Tjonasam, the director of portfolio management at Baruch’s student-run fund, Investment Management Group.

Italy’s debt as a percentage of its gross domestic product stands at 133 percent, second only to Greece’s 183 percent. Unlike Greece, Italy is so-called “too big to fail,” as it is also the world’s third largest government bond market.

The French vote is also crucial. National Front Leader Marine Le Pen called Brexit a “victory for freedom,” and her party is leading strongly in the polls. The two-step election for Europe’s second largest economy is scheduled for April 23 and May 7, 2017.

Even if the Five Star Movement and the Northern League win the election, they still have to hold a referendum on Italy’s membership in the eurozone and actually win it. If they do, “Italexit” and “Frexit” could be enough to destroy the entire currency bloc.

Around the same time, British Prime Minister Theresa May is expected to invoke Article 50, triggering a two-year countdown to Britain’s official exit from the European Union.

Even if the euro-skeptic parties fail to gain power, anti-establishment sentiments in the country will not go away.

“The Italy referendum ‘no’ vote is only a small speed bump to the ideal of a far-right movement that’s taking place across northern EU countries. The time frame to restore the Italians to path of stability, both politically and financially is uncertain,” Tjonasam added.

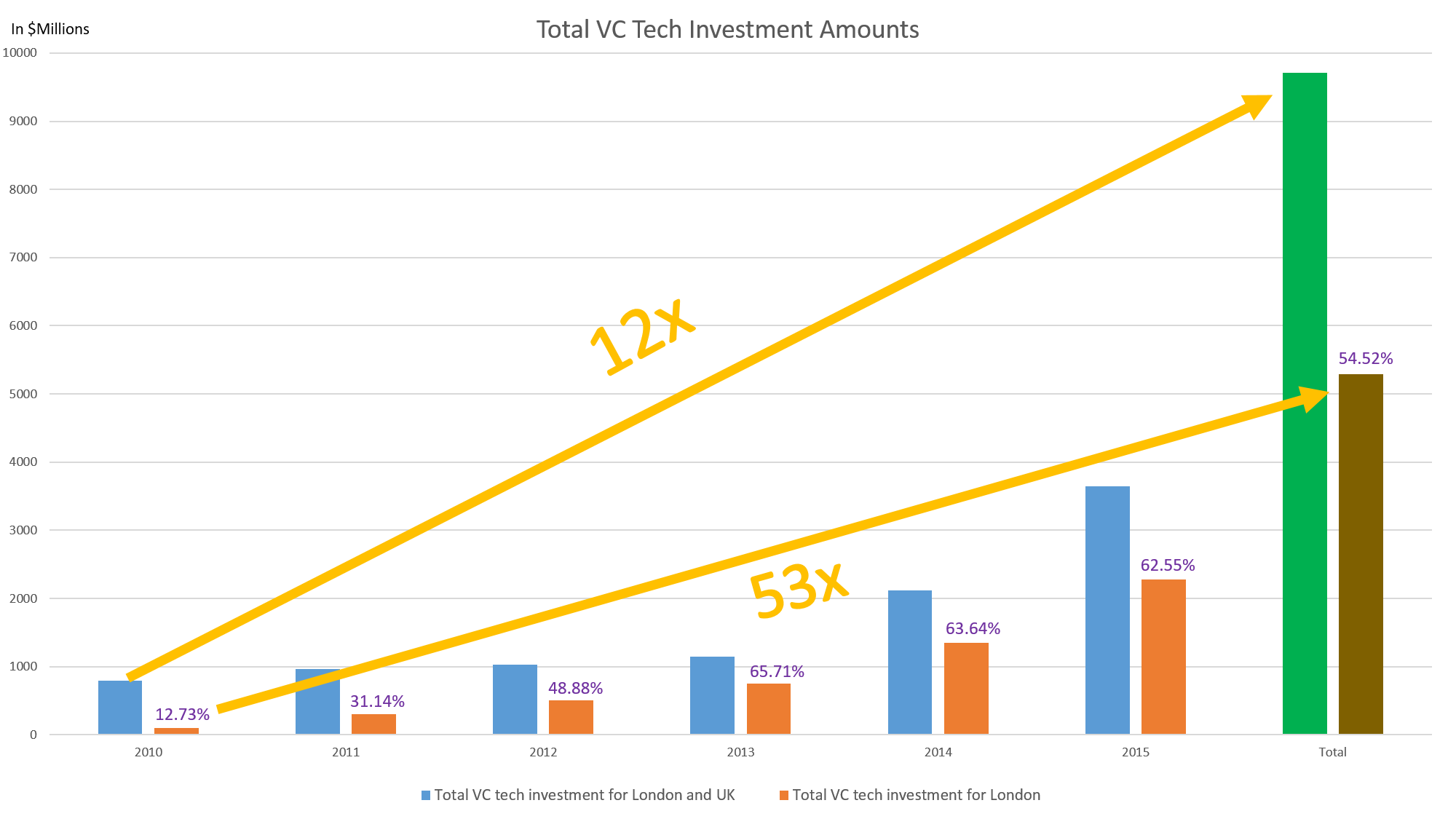

Silicon Valley is the fintech capital of the world. London is the fintech capital of Europe. After the Brexit vote, the rise of fintech in UK might be under a threat.

Total venture capital investment in technology for UK increased to over $3.6 billion in 2015, 71.43% increase from 2014. Of that, London-based tech start-ups accounted for 62.55%

Total VC Tech Investment Amounts UK/London 2010-2015

In the last 5 years, UK technology companies have collectively raised $9.7 billion, with London-based companies accounting for 54.52% of it or $5.3 billion.

Since 2010, investment in the British firms soared over 12-fold, while investment in the London-based firms soared over 53-fold.

Brexit can halt the growth of UK fintech industry.

Why is that? UK could lose its “passport.”

Many companies in EU, including fintech, use mechanism known as “passporting” to access Europe (European Economic Area) by getting licensed in a EU nation and be able to sell their products/services across the bloc. If the passporting privilege is lost, companies will have to submit application in every single country it wishes to operate in, which is time consuming and cost prohibitive.

Not only fintech companies, but also international banks would have to find a new legal home base. Large U.S. banks, such as Goldman Sachs (GS), Citi (C), and JP Morgan (JPM), employing thousands of people, would have to move its operations to other cities, such as Paris or Frankfurt.

Fintech companies could take the same direction as the banks. It is possible they will move to Ireland (Dublin). Ireland is European home (EU base) to Apple (AAPL), Google (GOOGL, GOOG), Microsoft (MSFT), Dell, Twitter (TWTR), Airbnb, and more. The corporate tax rate, which is one of the most important part of Irish investment attraction, is 12.5%, one of the lowest in Europe. That’s very low compared to United Kingdom’s 20% rate and Europe average of 20.24%.

One other important part of Irish investment attraction is its KDB (Knowledge Development Box). Certain intellectual propriety income, such as patent/copyright, are subject to just 6.25% tax, half of its famous 12.5% corporate tax rate. Not only that, but there is also 25% tax credit for research and development spending.

The KDB is clearly aimed at incentivizing innovate R&D. It provides 50% deduction in tax rate from qualifying profits. In other words, 50% allowance. No wonder so many U.S. tech companies are using Ireland as their European base.

In Europe, overall fintech investment increased 120% between 2014 and 2015. The number of deals increased by 51%. Both should continue to increase as states like Ireland continue to attract start-ups and talent. However, if UK files for Article 50 and other EU members plans to follow the same path, it is very possible the increased uncertainty over the EU cartel will scare away start-ups and international investors.

There’s also the issue of free movement of labor. One in three UK start-up workers are outsiders. Of the 34% workers from outside the UK, 20.7% are from the EU. 66% hold UK passport. The most common non-UK nationalities were Irish, American, and Spanish.

Brexit is likely to make it costlier and complicated for start-ups to attract and retain talent. Will the UK allow the free movement of labor? I don’t think so. One-third of leave voters stated the main reason for wanting to leave the EU “offered the best chance for the UK to regain control over immigration and its own borders.” Plus, other EU members, such as Ireland, probably want start-ups and talents to come to their cities, not stay in the UK.

In 2014, financial and related services employed nearly 2.2 million people, 7% of the UK workforce. The industry contributed 11.8% of UK economic output in 2014. London, the financial center of the UK and the world, accounted for 714,000 of the employment.

The British fintech firms employ about 61,000 people (2015 data), 2.8% of the financial and related services employment and 5.7% of financial services employment (both of which 2014 data).

The stakes are definitely high here.

Peer-to-peer (P2P), money-transfer and payments start-ups would be hardest hit by Brexit and by the end of EU passporting.

In April 2015, London-based P2P lending company, Funding Circle secured the largest single deal of the year with a $150 million funding, valuing the startup at over $1 billion, going straight into the “unicorn” club, private companies valued at $1 billion or more. The company is online marketplace that allows investors to lend money to small and medium-sized businesses.

In 2014, UK P2P business lending market size was 998 million euros ($1.1 trillion), 42.70% of total UK alternative finance market size. As I said above, “The stakes are definitely high here.”

Brexit could reduce lending, especially to 5.4 million small businesses in the UK accounting for 99.3% of all private sector business. Collectively small businesses account for 50% of GDP (Gross Domestic Product) and 60% of employment.

Many of these businesses will encounter financial problems, leading to layoffs of employees and so on (domino effect).

In addition to above, money-transfer and payments start-ups could also be hit hard as they will lose their “passporting” privilege. 54% of UK fintech firms focus on banking and payments. To sum up what I said about “passporting” above, if you’re regulated in UK, you’re regulated across the EU.

Other EU members, such as Ireland, will try to use Brexit to their advantage. They will try to make its laws more attractive to entice fintech firms away from London.

There is also chance the UK will get to keep its fintech firms, only if it differentiates itself with streamlined regulation, tax breaks, and increased support for innovation.

The UK will have to renegotiate the financial regulation with the EU. But I don’t believe they will get what they want. EU is already playing hard-ball. UK has more to lose than the EU.

Article 50 won’t likely be triggered until late this year or early next year. If by then, anti-Brexit campaign gains momentum and the presence of pro-remain politicians increase in the UK government, it is likely UK will not leave EU.

If you have any views, I would love to know in the comments below. If you have any questions about any issues related to Brexit, I would be happy to answer them ASAP. Don’t be surprised if the answer is 5 paragraphs long. Thank you.

On June 23rd, Britain people will vote to stay in or leave (Brexit) the European Union. The verdict matters a lot since it is a life-changing decision. I will briefly address some of the pros and cons of Brexit, but will further address it after the vote, especially if UK leaves EU.

Brexit Pros:

The European Union costs United Kingdom 350 million pounds ($503 million) a week. That’s $26.2 billion a year, 4.6 times less the UK education budget of $121.1 billion in 2015. That $26.2 billion is 1% of 2015 GDP of $2.63 trillion. That $26.2 billion is 2.45% of 2015 total spending of $1.07 trillion.

Note: That 350 million pounds a week cost is before “the rebate.” In 2015, Britain actually paid under 250 million ($359 million) pounds a week. But hey, UK does not control the rebates. The cost of membership has been increasing over the years, especially after the financial crisis.

What happened with Greece and is still happening, is a warning sign of more economic troubles to come in Europe. That possibly will continue to increase the cost of EU membership.

Under EU fundamental right of free movement, Britain cannot prevent anyone from another member state coming in to the country. This has resulted in a huge increase in immigration into Britain from Europe.

In 2015, 270,000 EU citizens immigrated to the UK and 85,000 EU citizens emigrated aboard. Net-migration was 185,000.

2.94 million people living in the UK in 2014 were citizens of another EU member country. Those people account for 4.7% of the UK population.

2.2 million citizens of another EU member country are in work, 7.02% of working population. Majority of EU member citizens are coming to the UK for work reasons. 61% of the migration who came for work reasons were EU citizens.

See how EU citizens coming to the UK for work reason started to accelerate in 2013. This can be related to economic difficulties such as Greece, Spain, Portugal and Italy. As I mentioned above, “What happened with Greece and is still happening, is a warning sign of more economic troubles to come in Europe.” That should lead to even more upsurge in migration for work reason, making it more competitive for UK citizens to find jobs and possibly lowering wages.

If UK decides to leave EU, the country would be able to reform immigration laws without input from the EU and increase jobs and wages for UK citizens (hopefully they have the skills).

Brexit Cons:

EU membership makes UK attractive for international investment and provides access to trade deals with more than 50 countries around the world (expensivemakeup, isn’t it?). Because EU institutions have the ability to prevent the UK from negotiating its own trade deals outside Europe, it would have to re-negotiate some trade deals, with EU and non-EU countries including the US, China, Japan and India. It is extremely possible the Brexit will impair confidence and investment for few years.

In 2015, the EU accounted for (pdf download) 43.7% of exports and 53.1% of imports

In 2014, the EU accounted for 496 billion pounds ($712 billion) of the stock of inward Foreign Direct Investment (FDI), 48% of the total. Globally, the UK is the third largest country in terms of its absolute value of inward FDI stock ($1.7 trillion), followed by China ($2.7 trillion) and U.S. ($5.4 trillion).

Why is FDI so important? It has the potential for job creation and productivity, increasing both output and wages.

If UK were to leave EU, it would dampen FDI due to uncertainty of the future. Firms would reduce investment in UK, leading to lay offs and so on (domino effect).

3.3 million UK jobs are linked to UK exports to other EU countries. Auto industry would be particularly at risk. In 2015, 77.3% of cars built in the UK were exported, a record high. EU demand grew 11.3%, with 57.5% of exports destined for the continent. In 2014, the motor vehicle manufacturing accounted for 7.9% (pdf download) of total manufacturing, up from 5.4% in 2007. The end of free trade agreements would definitely hurt UK automotive industry.

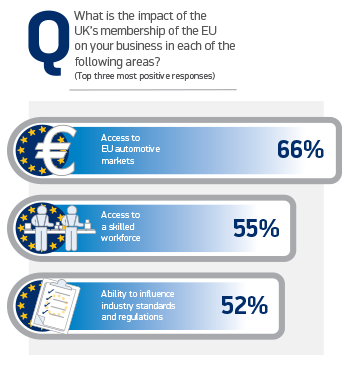

If UK were to leave the Single Market (EU), locating production in the UK would be less attractive because it would become more costly to ship to EU members. 77% of members of SMMT (Society of Motor Manufacturers and Traders) – the voice of the UK motor industry – believes remaining in EU would be the best for their business. 9% believes Brexit is the best path. 14% doesn’t know, like economists don’t know the real impact of Brexit due to a large base of issues and views.

66% believes EU important to them because of its access to EU automotive markets.

Why The EU Is Important To SMMT Members

Brexit would send a ripple effect. For the government (less tax revenue), for businesses (rising costs) and for consumers (lower income).

There’s also the issue of UK citizens in the other EU member countries. They have the right to live, work, vote, run a business, buy a property, and use public services such as health. Some, if not all, of these rights could vanish if UK leaves the EU.

Sure, UK will try to protect them. Since one of the main goals of Brexit is stop the inflows of immigrants into UK from EU, EU might retaliate against it.

UK (the wife) has been married to EU (the husband) for 43 years (UK joined EU in 1973). Part of her wants to get out of the cage. Other part of her wants to keep some of the benefits. If Brexit, it will be very expensive and messy divorce, but may be for the good.

There are so many views on this “monumental” and “out-of-focus” complicated issue. Not every issue is covered in this article. If UK is the first country to leave EU, I will do much more research and analyze it.

If you have any views, I would love to know in the comments below. If you have any questions about any issues related to Brexit, I would be happy to answer them ASAP. Don’t be surprised if the answer is 5 paragraphs long. Thank you.

This article was initially posted on The Ticker, Baruch College’s (the college I currently attend) independent, student-run newspaper. I’m re-posting the article with small changes.

The European Central Bank cut all rates and expanded its quantitative easing program. Amid growing concerns about economic growth and inflation, the 19-country eurozone’s central bank cut its rates to an all-time low. The refinancing rate, the rate of interest that banks must pay when they borrow funds from the ECB, was decreased by 5 basis points to zero percent. The marginal lending facility, the rate at which the central bank offers overnight credit to banks, was decreased by 5 basis points to 0.25 percent.

The deposit rate was cut further into negative territory. As expected by markets, the central bank cut its deposit rate by 10 basis points to negative 0.4 percent. The purpose of lower interest rates is to boost lending by encouraging banks to lend more to businesses and consumers, which in turn boosts spending and investment. In 2014, household consumption expenditure and investment accounted for 56.5 percent of GDP and 18 percent of GDP, respectively. QE was expanded from 20 billion euros to 80 billion euros ($89 billion) starting in April.

Under QE, the eurozone central bank pumps money into the region by buying assets, such as bonds, in the expectation that the proceeds will be invested in the European economy. In addition to bonds issued by financial institutions, QE will now include bonds issued by non-financial corporations.

“Rates will stay low, very low, for a long period of time, and well past the horizon of our purchases,” said Draghi, president of the central bank, referring to the QE. Its asset purchase program, or the QE, is expected to run until at least March 2017.

Policymakers have come under growing pressure to increase monetary stimulus after the eurozone slipped back into negative inflation in February.According to an early estimate by statistics office Eurostat, annual inflation dropped to negative 0.2 percent in February, down from 0.3 percent in January, the worst reading since February of last year.

That is far below the central bank’s inflation target of just under 2 percent. Draghi stated, “While very low or even negative inflation rates are unavoidable over the next few months, as a result of movements in oil prices, it is crucial to avoid second-round effects by securing the return of inflation to levels below, but close to, 2 percent without undue delay.”

Low energy prices were the main factor behind the drop in headline inflation. Energy prices fell 8 percent, down from a contraction 5.4 percent in January. Core inflation, which excludes food and energy, dropped 0.8 percent, down from 1 percent in January—the lowest since April of last year.

Lower core inflation reading suggests that the low energy prices are already feeding into the price of other goods and services, creating what Draghi called second-round effects that could lead to even lower inflation and eventually lead to deflation.

“Inflation rates are expected to remain at negative levels in the coming months and to pick up later in 2016,” said Draghi. The central bank lowered its inflation forecast for this year to 0.1 percent from the 1 percent previously predicted. In 2017, the inflation is forecasted to be at 1.3 percent. The previous forecast was for 1.6 percent.

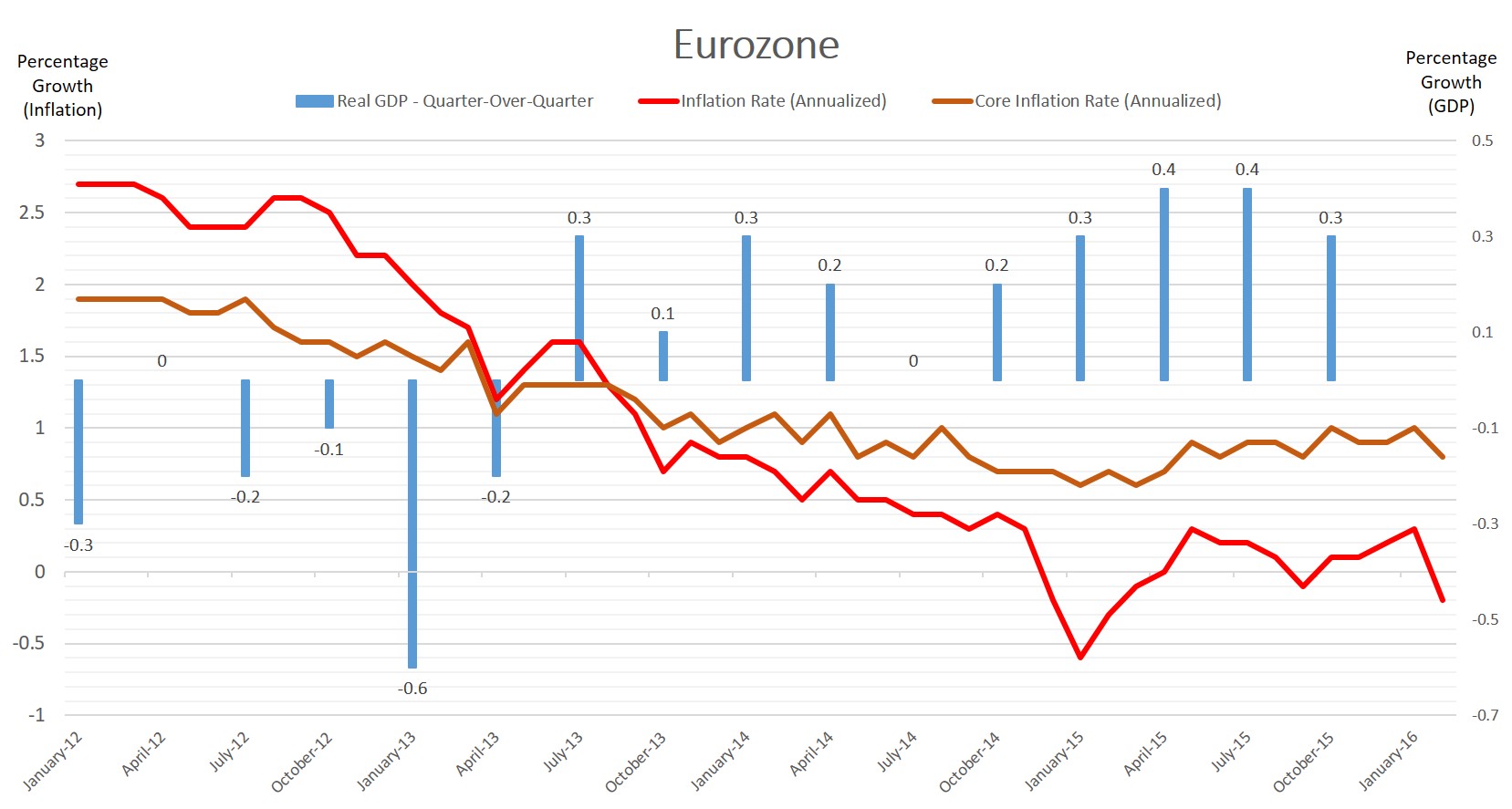

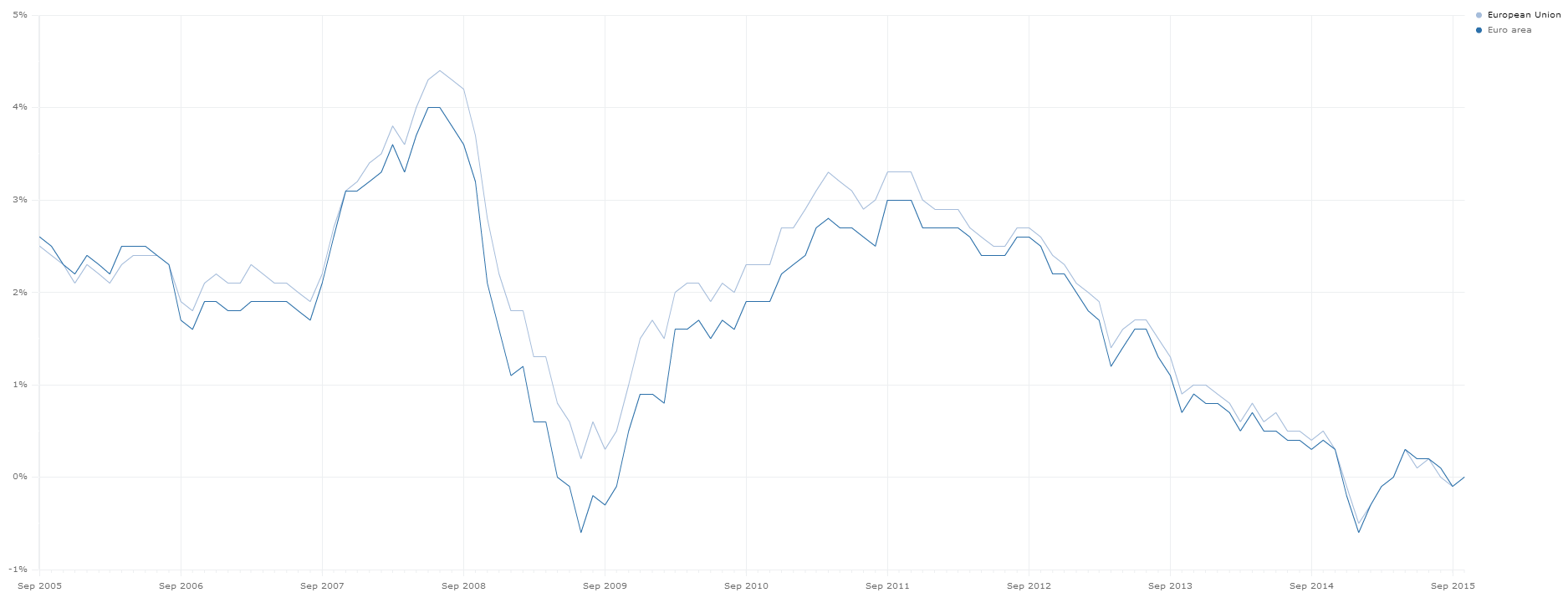

Eurozone Inflation and Real GDP Source: Eurostat

Reflecting weaker economic prospects around the globe and low energy prices, the growth outlook was also lowered.Gross domestic product is projected to expand 1.4 percent this year, lower than a previous forecast of 1.7 percent.

In 2017, it is projected to expand 1.7 percent, lower than a previous forecast of 1.9 percent. Kenneth Tjonasam, a 27-year-old Baruch College senior majoring in finance, believes the central bank is running out of viable solutions.

He stated, “I believe the ECB moves are unprecedented. I’m starting to think they have run out of viable patient solutions to address the slow growth in aggregate demand.”

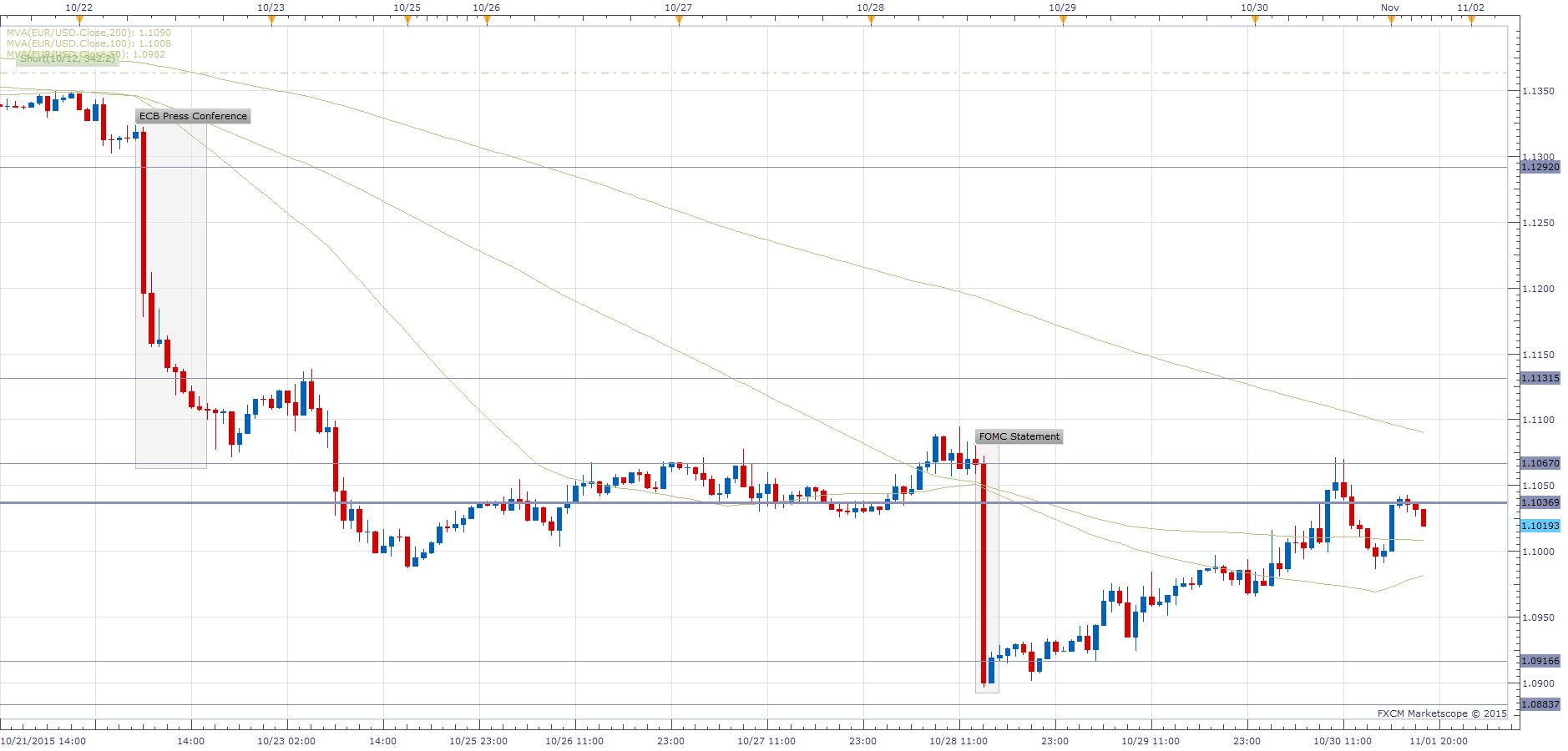

European markets soared and the euro weakened in a reaction to the rate cuts and expansion of QE, but they reversed when Draghi suggested no further rate cuts. “We don’t anticipate that it will be necessary to reduce rates further,” said Draghi. Then, European markets fell back and the euro soared.

EUR/USD Reaction to ECB

In order to further ease private sector credit conditions, the central bank also decided to offer eurozone financial institutions ultra-cheap four-year loans. The central bank said the interest rate on the loans “can be as low as the rate on the deposit facility,” meaning the eurozone banks could get paid to take the loans.

The purpose is to boost lending to consumers and companies. There is no guarantee they will borrow the money.

The European Central Bank will meet again on April 21. No further stimulus is expected at the moment.

12….11…10…9….IGNITION SEQUENCE START….6….5….4….3….2….1….0….ALL ENGINES RUNNING….LIFTOFF….WE HAVE A LIFTOFF!

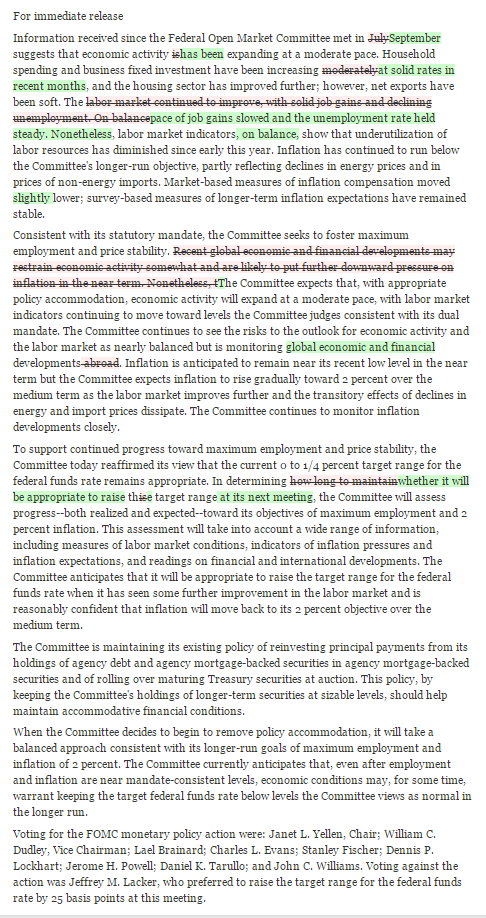

The Fed finally raised rates after nearly a decade. On December 16, the Fed decided to raise rates – for the first time since June 2006 – by 0.25%, or 25 basis points. It was widely expected by the markets and I only expected 10bps hike. Well, I was wrong on that.

The Federal Open Market Committee (FOMC) unanimously voted to set the new target range for the federal funds rate at 0.25% to 0.50%, up from 0% to 0.25%. In the statement, the policy makers judged the economy “has been expanding at a moderate pace.” Labor market had shown “further improvement.” Inflation, on the other hand, has continued to “run below Committee’s 2 percent longer-run objective” mainly due to low energy prices.

Remember when the Fed left rates unchanged in September? It was mainly due to low inflation. What’s the difference this time?

In September, the Fed clearly stated “…survey—based measures of longer-term inflation expectations have remained stable.”

Now, the Fed clearly states “…some survey-based measures of longer-term inflation expectations have edged down.”

So…umm…why did they raise rates this time?

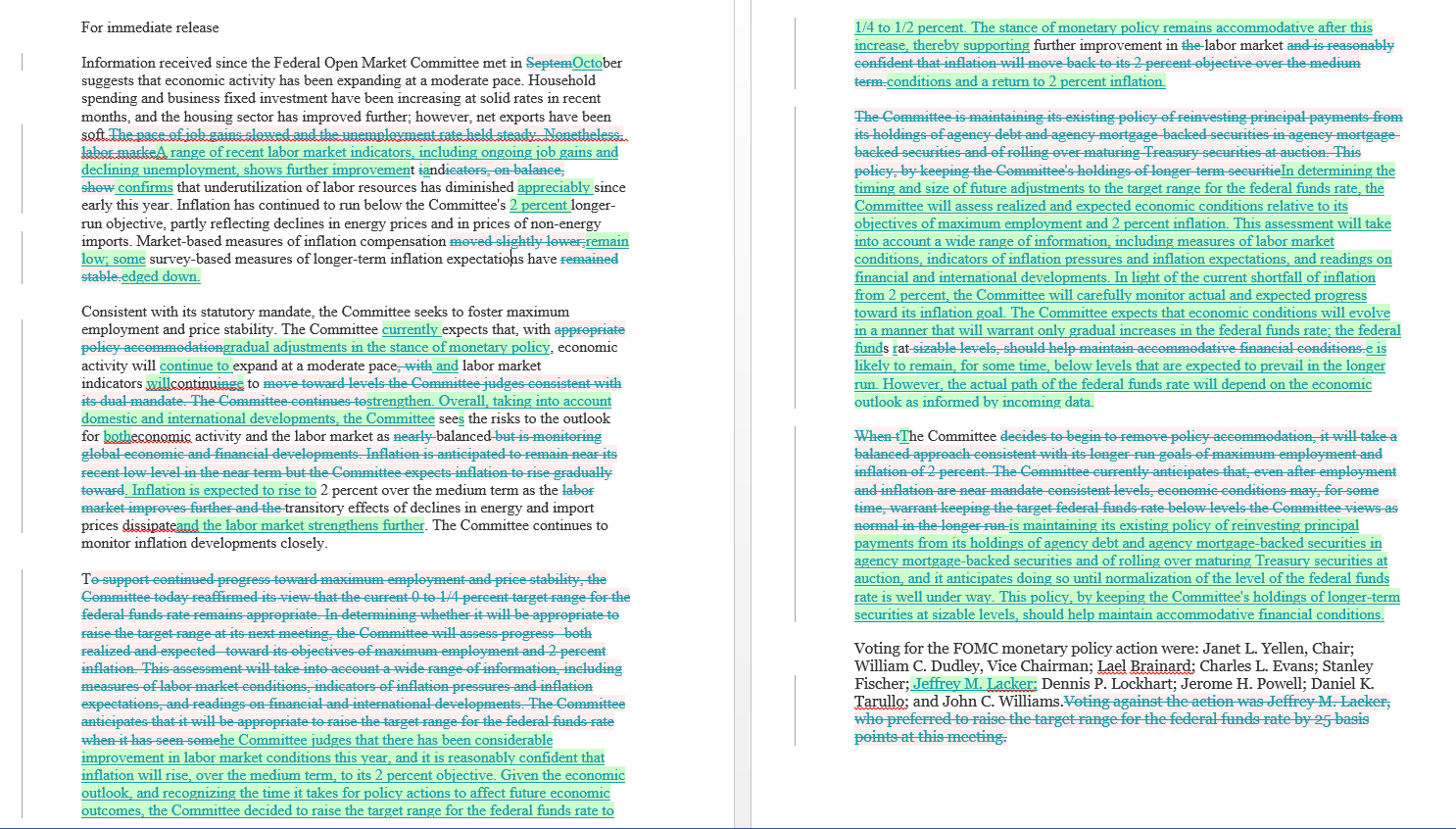

Here is a statement comparison from October to December:

Fed Statement Comparison – Oct. to Dec. Source: WSJ

On the pace of rate hikes looking forward, the FOMC says:

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

They clearly stated one of the things they look for, which is inflation expectations. But, they also did state that “inflation expectations have edged down.”

It seems to me that the Fed did not decide to raise rates. The markets forced them. Fed Funds Futures predicted about 80% chance of a rate-hike this month. If the Fed did not raise rates, they would have lost their credibility.

I believe the Fed will have to “land” (lower back) rates this year, for the following reasons:

Growing Monetary Policy Divergence

On December 3, European Central Bank (ECB) stepped up its stimulus efforts. The central bank decided to lower deposit rates by 0.10% to -0.30%. The purpose of lower deposit rates is to charge banks more to store excess reserves, which stimulates lending. In other words, free money for the people so they can spend more and save less.

ECB also decided to extend Quantitative Easing (QE) program. They will continue to buy 60 billion euros ($65 billion) worth of government bonds and other assets, but until March 2017, six months longer than previously planned, taking the total size to 1.5 trillion euros ($1.6 trillion), from the previous $1.2 trillion euros package size. During the press conference, ECB President Mario Draghi said the asset eligibility would be broadened to include regional and local debt and signaled QE program could be extended further if necessary.

ECB might be running out of ammunition. ECB extending its purchases to regional and local debt raises doubts about its program.

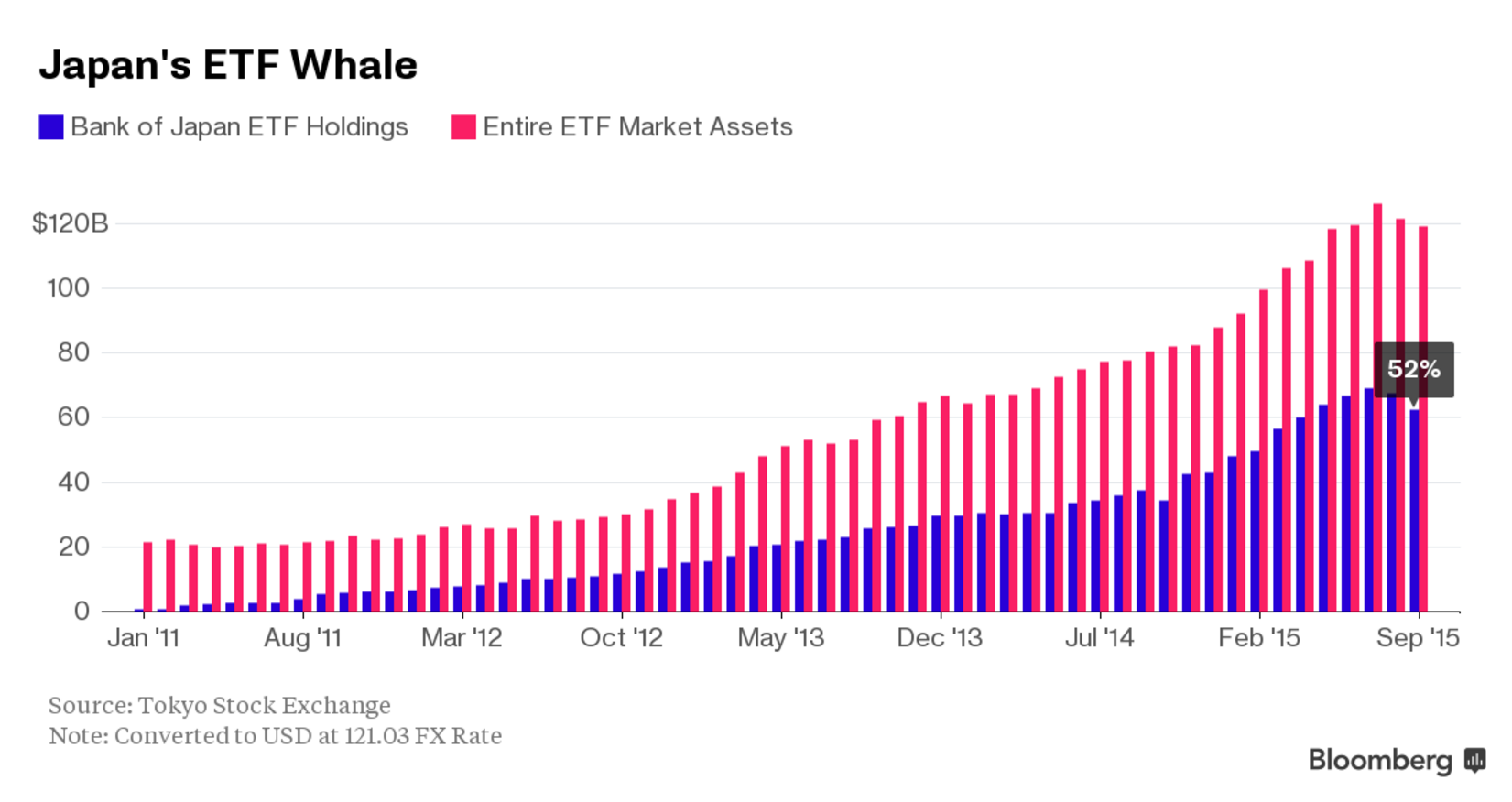

Not only ECB is going the opposite direction of the Fed. Three weeks ago, Bank of Japan (BoJ) announced a fresh round of new stimulus. The move was hardly significant, but it is still a new round of stimulus. The central bank decided to buy more exchange-traded fund (ETF), extend the maturity of bonds it owns to around 7-12 years from previously planned 7-10 years, and increase purchases of risky assets.

The move by BoJ exposes the weakness of its past actions. It suggests the bank is also out of ammunition. Already owning 52% or more of the Japan’s ETF market and having a GDP-to-Debt ratio around 245%, it is only a matter of time before Japan’s market crashes. Cracks are already beginning to be shown. I expect the market crash anytime before the end of 2019.

So, what are the side-effects of these growing divergence?

For example, the impact of a US dollar appreciation resulting from a tightening in US monetary policy and the impact of a depreciation in other currencies resulting from easing in its monetary policies. Together, these price changes will shift global demand – away from goods and services produced here in the U.S. and toward those produced abroad. In others words, US goods and services become more expensive abroad, leading to substitution by goods and services in other countries. Thus, it will hurt the sales and profits of U.S. multinationals. To sum up everything that is said in this paragraph, higher U.S. rates relative to rates around the global harms U.S. competitiveness.

Emerging Markets

Emerging markets were trouble last year. It is about to get worse.

International Monetary Fund (IMF) decided to include China’s currency, renminbi (RMB) or Yuan, to its Special Drawing Rights (SDR) basket, a basket of reserve currencies. Effective October 1, 2016, the Chinese currency is determined to be “freely usable” and will be included as a fifth currency, along with the U.S. dollar, euro, Japanese yen, and pound sterling, in the SDR basket.

“Freely useable” – not so well defined, is it?

Chinese government or should I say People’s Bank Of China (PBOC), cannot keep its hands off the currency (yuan). It does not want to let market forces take control. They think they can do whatever they want. As time goes on, it is highly unlikely. As market forces take more and more control of its exchange-rate, it will be pushed down, due to weak economic fundamentals and weak outlook.

China, no need to put a wall to keep market forces out. Let the market forces determine the value of your currency. It is only a matter of time before they break down the wall.

In August, China changed the way they value their currency. PBOC, China’s central bank, said it will decide the yuan midpoint rate based on the previous day’s close. In daily trading, the yuan is allowed to move 2% above or below the midpoint rate, which is called the daily fixing. In the past, the central bank used to ignore the daily moves and do whatever they want. Their decision to make the midpoint more market-oriented is a step forward, but they still have a long way to go.

China saw a significant outflows last year. According to Institute of International Finance (IFF), an authoritative tracker of emerging market capital flows, China will post record capital outflows in 2015 of more than $500 billion. The world’s second largest economy is likely to see $150 billion in capital outflow in the fourth quarter of 2015, following the third quarter’s record $225 billion.

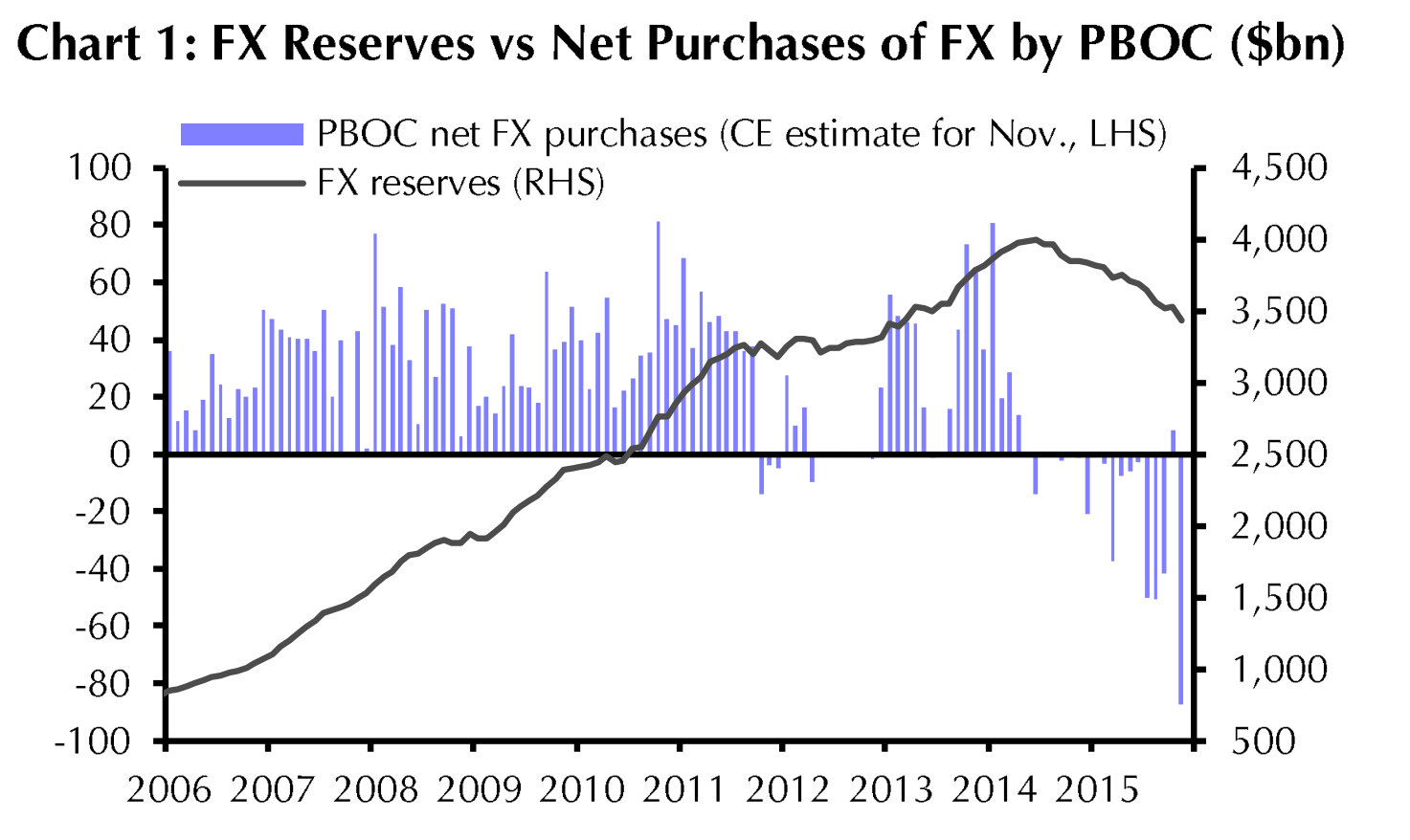

Ever since the devaluation in August, PBOC has intervened to prop yuan up. The cost of such intervention is getting expensive. The central bank must spend real money during the trading day to guide the yuan to the level the communists want. Where do they get the cash they need? FX reserves.

China’s foreign-exchange reserves, the world’s largest, declined from a peak of nearly $4 trillion in June 2014 to just below $3.5 trillion now, mainly due to PBOC’s selling of dollars to support yuan. In November, China’s FX (forex) reserves fell $87.2 billion to $3.44 trillion, the lowest since February 2013 and largest since a record monthly drop of $93.9 billion in August. It indicates a pick-up in capital outflows. This justifies increased expectations for yuan depreciation. Since the Fed raised rates last month, I would not be surprised if the capital flight flies higher, leading to a weaker yuan.

Depreciation of its currency translates into more problems for “outsiders,” including emerging markets (EM). EMs, particularly commodities-linked countries got hit hard last year as China slowed down and commodity prices slumped. EMs will continue to do so this year, 2016.

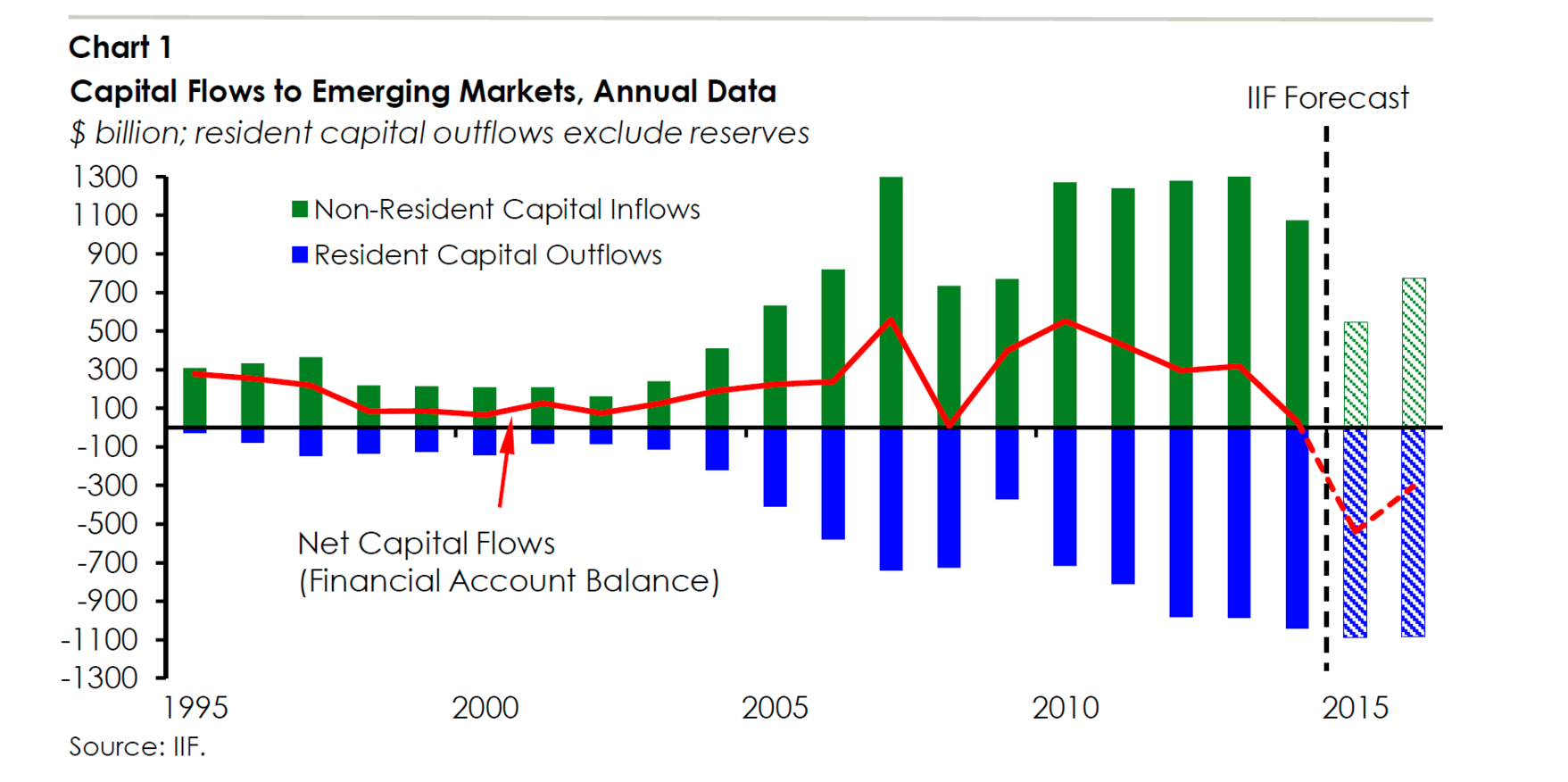

The anticipation of tightening in the U.S. and straightening dollar put a lot of pressure on EM. EM have seen a lot of significant capital outflows because they carry a lot of dollar denominated debt. According to the October report from IFF, net capital flows to EM was negative last year for the first time in 27 years (1988). Investors are estimated to pull $540 billion from developing markets in 2015. Foreign inflows will fall to $548 billion, about half of 2014 level and lower than levels recorded during the financial crisis in 2008. Foreign investor inflows probably fell to about 2% of GDP in emerging markets last year, down from a record of about 8% in 2007.

Capital Flows to Emerging Markets, Annual Data Source: IFF, taken from Bloomberg

Also contributing to EM outflows are portfolio flows, “the signs are that outflows are coming from institutional investors as well as retail,” said Charles Collyns, IIF chief economist. Investors in equities and bonds are estimated to have withdrawn $40 billion in the third quarter, the worst quarterly figure since the fourth quarter of 2008.

A weaker yuan will make it harder for its main trading partners, emerging markets and Japan, to be competitive. This will lead to central banks of EM to further weaken their currencies. Japan will have no choice but to keep extending their QE program. And to Europe. And to the U.S. DOMINO EFFECT

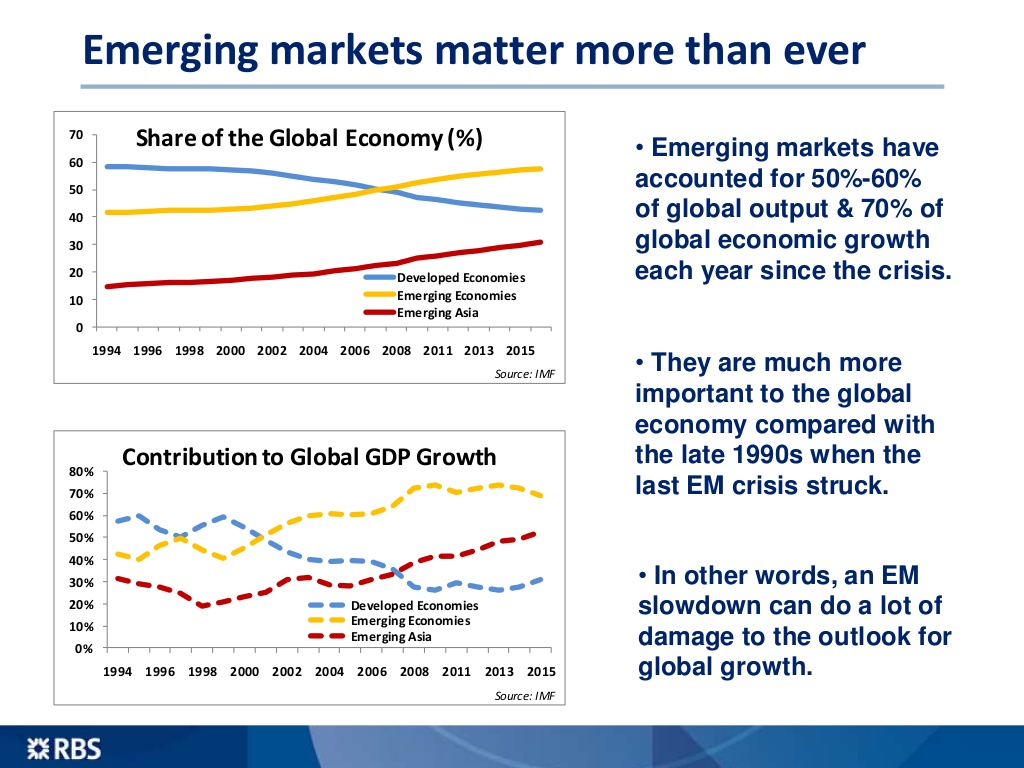

Why are EMs so important? According to RBS Economics, EMs have accounted for 50%-60 of global output and 70% of global economic growth each year since the 2008 crisis.

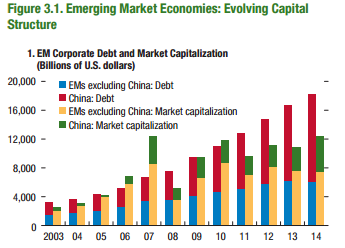

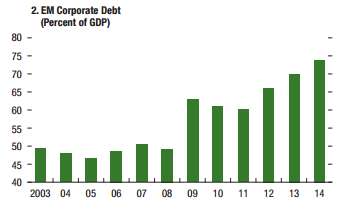

Some EM investors, if not all, will flee as U.S. rates rise, compounding the economic pain there. Corporate debt in EM economies increased significantly over the past decade. According to IMF’s Global Financial Stability report, the corporate debt of non-financial firms across major EM economies increased from about $4 trillion in 2004 to well over $18 trillion in 2014.

When you add China’s debt with EM, the total debt is higher than the market capitalization. The average EM corporate debt-to-GDP ratio has also grown by 26% the same period.

EM Corporate Debt (percent of GDP) – Page 84

The speed in the build-up of debt is distressing. According to Standard & Poor’s, corporate defaults in EM last year have hit their highest level since 2009, and are up 40% year-over-year (Y/Y).

According to IFF (article by WSJ), “companies and countries in EMs are due to repay almost $600 billion of debt maturing this year….of which $85 is dollar-denominated. Almost $300 billion of nonfinancial corporate debt will need to be refinanced this year.”

I would not be surprised if EM corporate debt meltdown triggers sovereign defaults. As yuan weakens, Japan will be forced to devalue their currency by introducing me QE which leaves EMs with no choice. EMs will be forced to devalue their currency. Devaluations in EM currencies will make it much harder (it already is) for EM corporate borrowers to service their debt denominated in foreign currencies, due to decline in their income streams. Deterioration of income leads to a capital flight, pushing down the value of the currency even more, which leads to much more capital flight.

“Firms that have borrowed the most stand to endure the sharpest rise in their debt-service costs once interest rates begin to rise in some advanced economies. Furthermore, local currency depreciations associated with rising policy rates in the advanced economies would make it increasingly difficult for emerging market firms to service their foreign currency-denominated debts if they are not hedged adequately. At the same time, lower commodity prices reduce the natural hedge of firms involved in this business.”

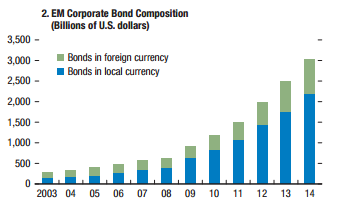

According to its Global Financial Stability report, EM companies have an estimated $3 trillion in “overborrowing” loans in the last decade, reflecting a quadrupling of private sector debt between 2004 and 2014.

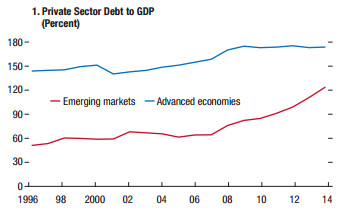

EM Corporate Bond Composition (Billions of U.S. dollars) – Page 86Private Sector Debt to GDP (Percent – Page 11

Rising US rates and a strengthening dollar will make things much worse for EMs. Jose Vinals, financial counsellor and director of the IMF’s Monetary and Capital Markets Department, said in his October article, “Higher leverage of the private sector and greater exposure to global financial conditions have left firms more susceptible to economic downturns, and emerging markets to capital outflows and deteriorating credit quality.”

I believe currency war will only hit “F5” this year and corporate defaults will increase, leading to the early stage of sovereigns’ defaults. I would not be surprised if some companies gets a loan denominated in euros just to pay off the debt denominated in U.S dollars. That’s likely to make things worse.

Those are some of the risks I see that will force the Fed to lower back the rates. I will address more risks, including lack of liquidity, junk bonds, inventory, etc, in my next article. Thank you.

EXTRA: Market reactions,

EUR/USD:

EUR/USD – Hourly Chart

USD/JPY:

USD/JPY – Hourly

10-Year Treasury Index:

10-Year Treasury Index ( “TNX” on thinkorswim platform) – Hourly

2-Year U.S. Treasury Note Futures:

2-Year U.S. Treasury Note Futures ( “/ZT” on thinkorswim platform) – Hourly

On October 22 (Thursday), European Central Bank (ECB) left rates unchanged, with interests on the main refinancing operations, marginal lending, and deposit rate at 0.05%, 0.30% and -0.20, respectively. But the press conference gave an interesting hint. Mario Draghi, the President of ECB, was most dovish as he could be, “work and assess” (unlike “wait and see” before).

The central bank is preparing to adjust “size, composition and duration” of its Quantitative Easing (QE) program at its December meeting, “the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting”, Draghi said during the press conference. They are already delivering a massive stimulus to the euro area, following decisions taken between June 2014 and March 2015, to cut rates and introduce QE program. In September 2014, ECB cut its interest rate, or deposit rate to -0.20%, a record low. Its 1.1 trillion euros QE program got under way in March with purchases of 60 billion euros a month until at least September 2016.

When ECB cut deposit rate to record low in September 2014, Mr. Draghi blocked the entry to additional cuts, “we are at the lower bound, where technical adjustment are not going to be possible any longer.” (September 2014 press conference). Since then, growth hasn’t improved much and other central banks, such as Sweden and Switzerland, cut their interest rates into much lower territory. Now, another deposit rate-cut is back, “Further lowering of the deposit facility rate was indeed discussed.” Mr. Draghi said during the press conference.

The outlook for growth and inflation remains weak. Mr. Draghi – famous for his “whatever it takes” line – expressed “downside risks” to both economic growth and inflation, mainly from China and emerging markets.

Given the extent to which the central bank provided substantial amount of stimulus, the growth in the euro area has been disappointing. The euro area fell into deflation territory in September after a few months of low inflation. In September, annual inflation fell to 0.1% from 0.1% and 0.2% in August and July, respectively. Its biggest threat to the inflation is energy, which fell 8.9% in September, down from 7.2% and 5.6% in August and July, respectively.

As the ECB left the door open for more QE, Euro took a dive. Euro took a deeper dive when Mr. Draghi mentioned that deposit rate-cut was discussed. Deposit rate cut will also weaken the euro if implemented. After the press conference, the exchange rate is already pricing in a rate-cut. Mentions of deposit rate-cut and extra QE sent European markets higher and government bond yields fell across the board. The Euro Stoxx 50 index climbed 2.6%, as probability of more easy money increased. Swiss 10-year yield fell to fresh record low of -0.3% after the ECB press conference. 2-year Italian and Spanish yields went negative for the first time. 2-year German yield hit a record low of -0.32.

Regarding the exchange rate (EUR/USD), I expect it to hit a parity level by mid-February 2016.

As I stated in the previous posts, I expect more quantitative easing by ECB (and Bank of Japan also). I’m expecting ECB to increase its QE program to 85 billion euros a month and extend it until March 2017. When ECB decides to increase and extend the scope of its QE, I also expect deposit rate-cut of 10 basis points.

ECB will be meeting on December 3 when its quarterly forecasts for inflation and economic growth will be released. The only conflict with this meeting is that U.S. Federal Reserve policy makers meets two weeks later. ECB might hold off until the decision of the Fed, but the possibility of that is low.

EUR/USD Reaction:

EUR/USD – Hourly Chart

U.S. Federal Reserve:

On October 28 (Wednesday), the Federal Reserve left rates unchanged. The bank was hawkish overall. It signaled that rate-hike is still on the table at its December meeting and dropped previous warnings about the events abroad that poses risks to the U.S. economy.

It does not make sense to drop “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” (September statement) I’m sure the events abroad has its risks (spillover effect) to the U.S. economy and the Fed will keep an eye on them.

In its statement, it said the U.S. economy was expanding at a “moderate pace” as business capital investments and consumer spending rose at “solid rates”, but removed the following “…labor market continued to improve…” (September statement). The pace of job growth slowed, following weak jobs report in the past several months.

Let’s take a look at the comparison of the Fed statement from September to October, shall we?

The Fed badly wants to raise rates this year, but conditions here and abroad does not support its mission. Next Federal Open Market Committee (FOMC) meeting takes place on December 15-16. By then, we will get important economic indicators including jobs report, Gross Domestic Product (GDP), retail spending and Consumer Price Index (CPI). If we don’t see any strong rebound, rate-hike is definitely off the table, including my prediction of 0.10% rate-hike for next month.

The report caused investors to increase the possibility of a rate increase in December. December rate-hike odds rose to almost 50% after the FOMC statement.

Greenback (US Dollar) Reaction:

U.S. Dollar ( “/DX” on thinkorswim platform) – Hourly Chart

Reserve Bank of New Zealand:

On October 28 (Wednesday), Reserve Bank of New Zealand (RBNZ) left rates unchanged at 2.75% after three consecutive rate-cuts since June. The central bank’s Governor Graeme Wheeler said that at present “it is appropriate to watch and wait.” “The prospects for slower growth in China and East Asia” remains a concern.

Housing market continues to pose financial stability risk. House price inflation is way higher. Median house prices are about nine times the average income. Short supply caused the house prices to increase significantly. “While residential building is accelerating, it will take some time to correct the supply shortfall.” RBNZ said in a statement. Auckland median home prices rose about 25.4% from September 2014 to September 2015, “House price inflation in Auckland remains strong, posing a financial stability risk.”

Further reduction in the Official Cash Rate (OCR) “seems likely” to ensure future CPI inflation settles near the middle of the target range (1 to 3%).

Although RBNZ left rates unchanged, Kiwi (NZD) fell because the central bank sent a dovish tone, “However, the exchange rate has been moving higher since September, which could, if sustained, dampen tradables sector activity and medium-term inflation. This would require a lower interest rate path than would otherwise be the case.” It’s a strong signal that RBNZ will cut rates to 2.5% if Kiwi continues to strengthening. I will be shorting Kiwi every time it strengthens.

“The sharp fall in dairy prices since early 2014 continues to weigh on domestic farm incomes…However, it is too early to say whether these recent improvements will be sustained.” RBNZ said in the statement. Low dairy prices caused RBNZ to cut rates. New Zealand exports of whole milk powder fell 58% in the first nine months of this year, compared with the same period in 2014. But, there’s a good news.

Recent Chinese announcement that it would abolish its one-child policy might just help increase dairy prices, as demand will increase. How? New Zealand is a major dairy exporter to China. Its milk powder and formula industry is likely to benefit from a baby boomlet in China.

BoJ expects to hit its 2% inflation target in late 2016 or early 2017 vs. previous projection of mid-2016. Again and Again. This is the second time BoJ changed its target data. The last revision before this week was in April. It also lowered its growth projections for the current year by 0.5% to 1.2%.

They also lowered projections for Core-CPI, which excludes fresh food but includes energy. They lowered their forecasts for this fiscal year to 0.1%, down from a previous estimate of 0.7%. For the next fiscal year, they expect 1.4%, down from a previous estimate of 1.9%. Just like other central banks, BoJ acknowledged that falling energy prices were hitting them hard.

Low inflation, no economic growth, revisions, revisions, and revisions. Nothing is recovering in Japan.

Haruhiko Kuroda, the governor of BoJ, embarked on aggressive monetary easing in early 2013. So far he hasn’t had much success.

In the second quarter (April-June), Japan’s economy shrank at an annualized 1.2%. Housing spending declined 0.4% in September from 2.8% in August. Core-CPI declined for two straight months, falling 0.1% year-over-year both in September and August. Annual exports only rose 0.6% in September, slowest growth since August 2014, following 3.1% gain in August.

Exports are part of the calculation for Gross Domestic Product (GDP). Another decline in GDP would put Japan into recession, which could force BoJ to ease its monetary policy again. Another recession would be its fourth since the 2008 financial crisis and the second since Shinzo Abe (Abenomics), the Prime Minister of Japan, came to power in December 2012.

Its exports to China, Japan’s second-biggest market after the U.S., fell 3.5% in September. The third-quarter (July-September) GDP report will be released on November 16.

April 2014 sales tax (sales tax increased from 5% to 8%) increase only made things worse in Japan. It failed to boost inflation and weakened consumer sentiment.

In April 2013, BoJ expanded its QQE (or QE), buying financial assets worth 60-70 trillion yen a year, including Exchange Traded Funds (ETF).

QQE stands for Quantitative and Qualitative Easing. Qualitative easing targets certain assets to drive up their prices and drive down their yield, such as ETF. Quantitative Easing targets to drive down interest rates. Possibility of negative interest rates has been shot down by BoJ. But, why trust BoJ for their word? Actions speak louder than words.

In October 2014, BoJ increased the QQE to an annual purchases of 80 trillion yen. When is the next expansion? December?

Did you know that the BoJ owns 52% of Japan’s ETF market?

For over a decade, BoJ’s aggressive monetary easing through asset purchases did not help Japan’s economy. Since 2001, the central bank operated 9 QEs and is currently operating its current 10th QE (or QQE). The extensions of its QE are beginning to become routine or the “new normal.”

Growth and prices are slowing in China, with no inflation in United Kingdom, Euro-zone, and the U.S. The chances that Japan will crawl out of deflation are very slim.

USD/JPY Reaction:

USD/JPY – Hourly Chart

US Market Reactions (ECB and FOMC):

S&P 500 (“SPX”) – Hourly Chart

Next week, both Reserve Bank of Australia (RBA) and Bank of England (BoE) will meet. Will be very interesting to watch.