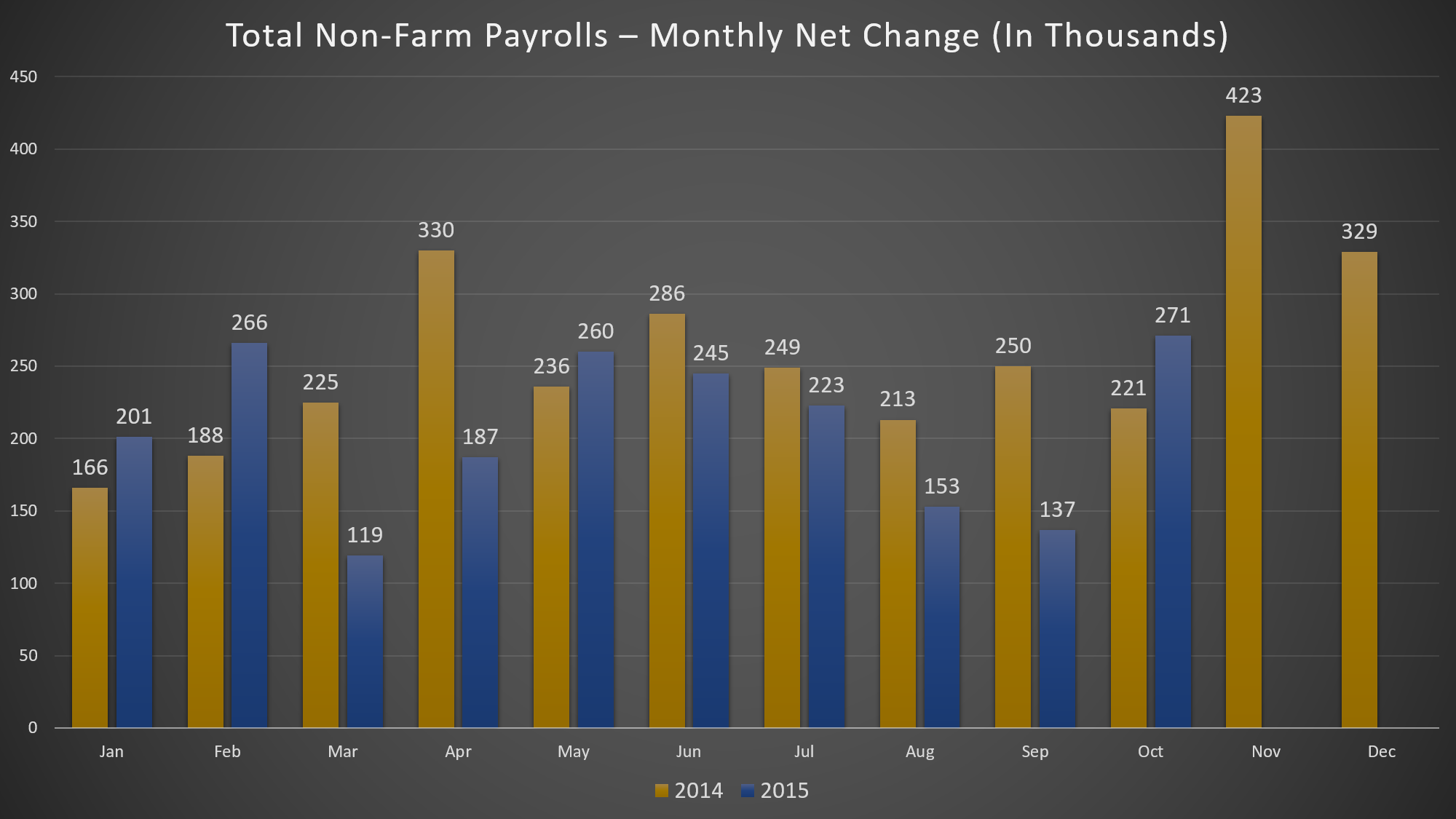

On November 6 (Friday), jobs report for October had the winds of 120 miles per hour and blew everyone away. Non-farm payrolls showed 271,000 jobs were added in October, the most gain since December and a huge beatdown on expectations of about 185,000. It’s the best month for job growth so far this year. The report follows two consecutive months (August and September) of weak jobs growth below 160,000.

The total job gains for August and September were revised 12,000 higher. August was revised 17K higher to 153K from 136k, and September was revised -5K lower to 137K from 142K. Over the last 12 months, employment growth had averaged 230K per month, vs. 222K in the same-period of 2014. In 2014, average monthly payrolls was 260K. This year, it is 206K. Not only jobs gains for October were strong, but also unemployment and wages.

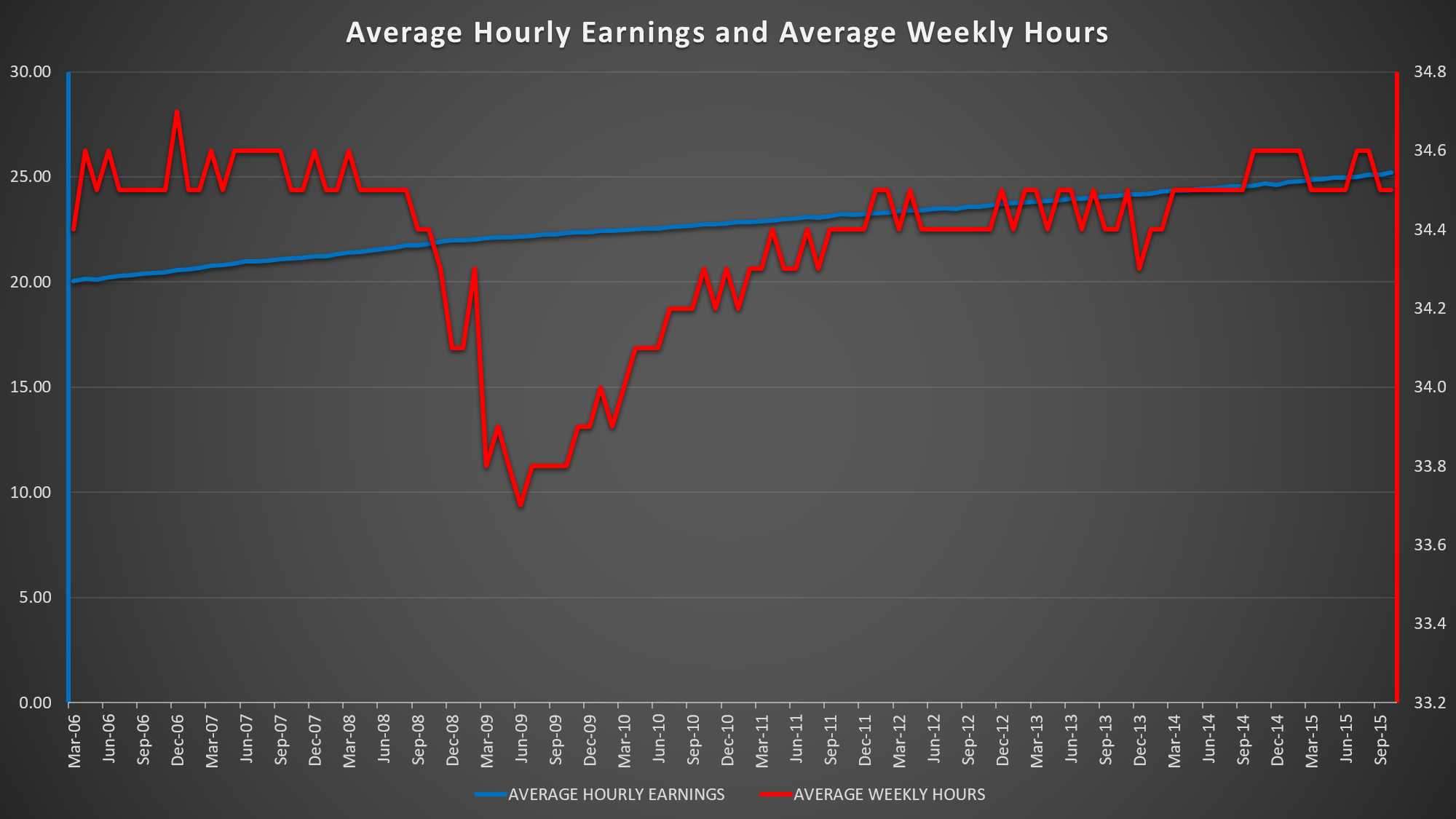

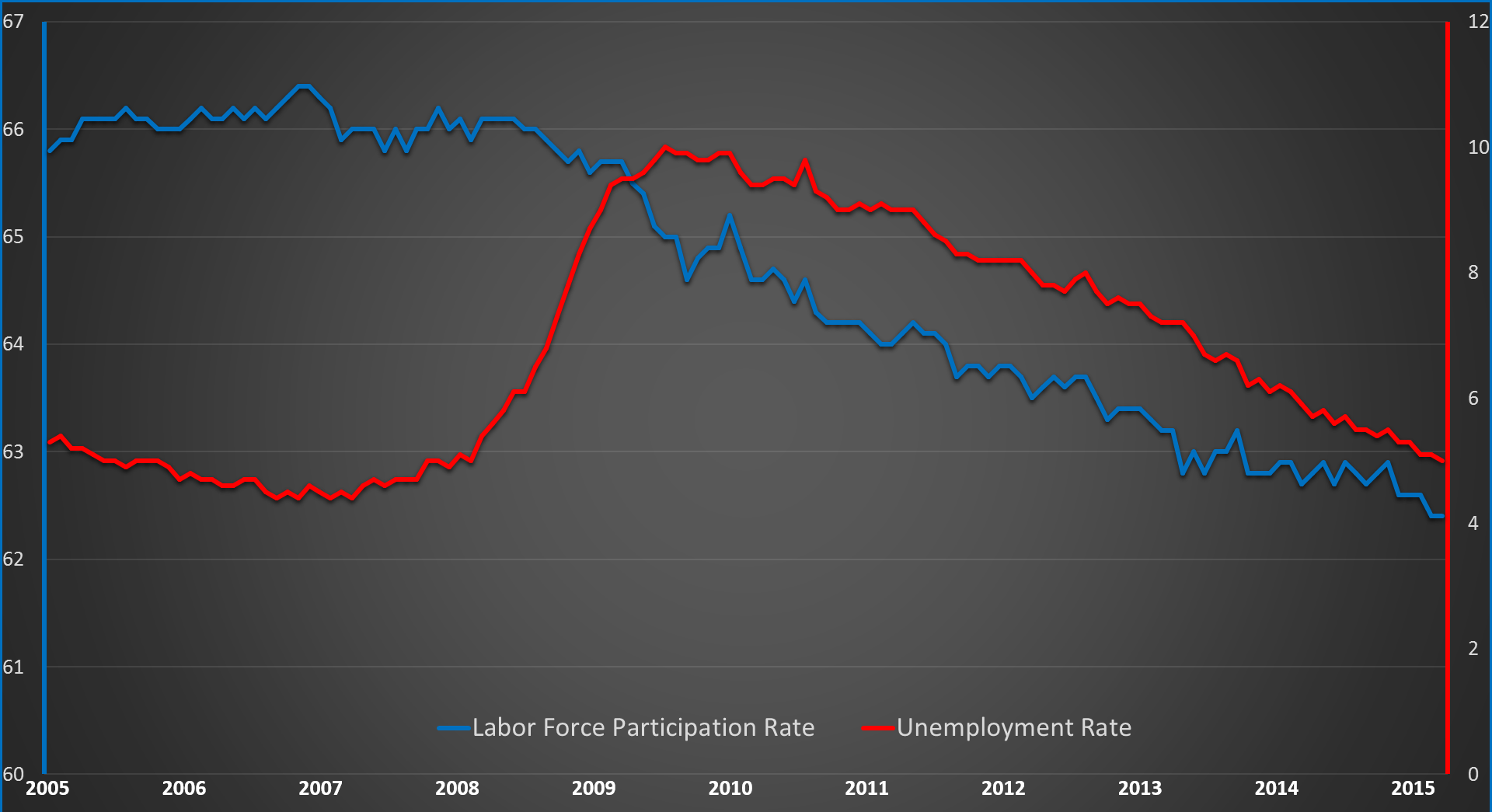

The unemployment rate dipped 0.1% to 5%, its lowest level since April 2008. Average hourly earnings rose by 9 cents an hour to $25.20. It rose 2.5% year-over-year (Y/Y), the best level since July 2009. For most of the “recovery”, wages has been flat. The increase in earnings is significant for two reasons. More money for employees means more spending (don’t forget debts), which accounts two-thirds of the economy. Second, wage growth might suggest that employers are having trouble finding new workers (should I say “skilled” workers) and they have to pay more to keep its workers and/or to get new skilled workers. This could draw more people back into the labor market, increasing the participation rate. Without the right skills, good luck.

The labor force participation rate remained unchanged at a 38-year (1977) low of 62.4%. The long-term decline in the participation rate is due to the aging of the baby-boom generation and loss of confidence in the jobs market. There hasn’t even been a rebound in participation rate of prime-age Americans (between the ages of 25 and 54).

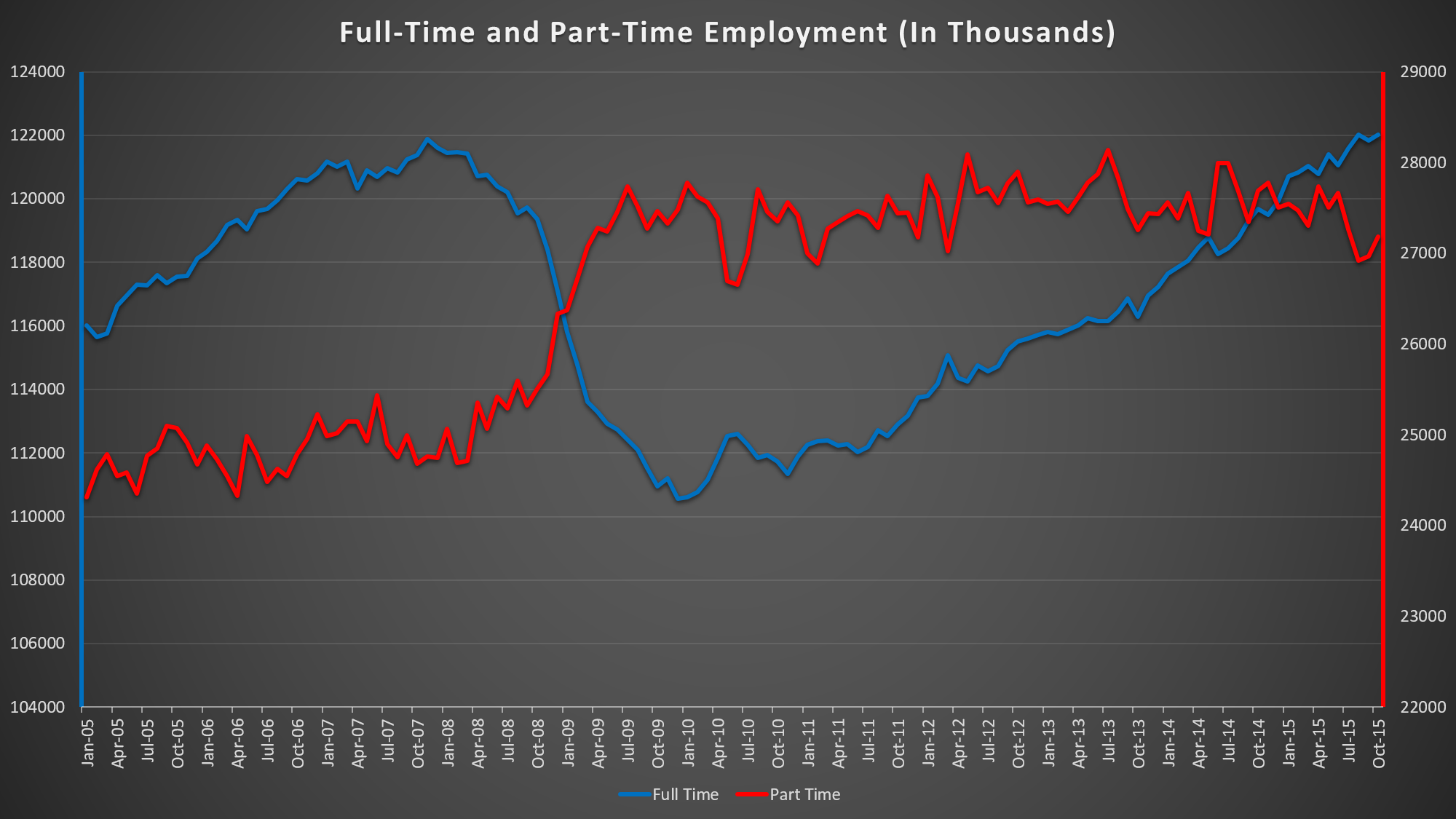

More than 122 million Americans had full-time jobs at the end of October, the highest since December 2007 (121.6 million).

Immediately after the jobs report, the probability of a rate-hike in December lifted. Fed funds futures currently anticipates about 65% chance of a rate hike next month vs. about 72% immediately after the report and about 55% before the report.

Federal Reserve Chairwoman, Janet Yellen, lately has been saying that December’s Federal Open Market Committee (FOMC) meeting was “live” for a potential rate-hike. While this jobs report is positive, I believe it is too early to jump in on conclusions.

The policymakers should not be too quick to act on one report. In September, the Fed left rates unchanged mainly due to a low inflation. Inflation is still low and we will get a fresh look on Tuesday (November 17) when Consumer Price Index (CPI) is released.

In March, the Fed expressed worries about the strength of the U.S. Dollar, just after the greenback hit above $100 mark. The greenback then tumbled and has never recovered back to $100….yet.

Right after the jobs report, the dollar skyrocketed and was 40 cents away from hitting $100 mark. It’s currently at $98.88 and there is a very high chance it will go above $100 until December 15, the first day of FOMC meeting.

If the November job numbers does not surprise to the upside (released in December 4), inflation stays low, and the dollar keeps strengthening, I do not believe the Fed will hit the “launch” button for a rate-hike liftoff.

Market Reactions:

One thought on “October Jobs Report Strong: It Is Just One Report”

Comments are closed.