In the next 8 days, I won’t be posting any articles as I get ready for my finals at Baruch College. I understand last week’s events (jobs reports, ECB, etc) are important and I plan to write about them. I also understand the Fed will be meeting next week. I will be writing about all of them after I’m done with the finals.

I just wanted to give a quick summary of what I think. I believe there’s a lot of risks for a rate-hike. Suchs risks include, lack of liquidity due to regulations, widening divergence between the Fed and many other central banks (ECB, BoJ, etc), junk bonds, and more. I will post an article about the risks.

I believe the Fed will raise rates by 0.10%, instead of 0.25%. Current probability of 25 basis points rate-hike stands above 80%. Thus, the Fed has to raise rates or they will lose their credibility. I believe 0.25% is too risky and 0.25% increase will backfire on them as I believe there are too much of risks.

I’m always on Twitter. You can tweet me your questions, comments, etc and I will respond within 24 hours. If you would like to discuss the financial news with me, feel free to contact me privately. Thank you.

On October 22, Eli Lilly (LLY) reported an increase in the third-quarter profit, as sales in its animal health segment and new drug launches offset the effect of unfavorable foreign exchange rates and patent expirations. Indianapolis-based drug maker posted a net income increase of 60% to $799.7 million, or to $0.75 per share, as its revenue increased 33% in animal health segment. In January 2015, Eli Lilly acquired Norvartis’s animal health unit for $5.29 billion in an all-cash transaction. The increase in the animal-health revenue helped offset sharp revenue decreases in osteoporosis treatment Evista and antidepressant Cymbalta, whose revenue fell 35% and 34% year-over-year, respectively. Eli Lilly lost U.S. patent protection for both drugs last year, causing patent cliffs. Lower price for the Evista reduced sales by about 2%.

Total revenue increased 2% to $4.96 billion even as currency headwinds, including strong U.S. dollar, shaved 8% off of the top line in revenue. Recently launched diabetes drug Trulicity and bladder-cancer treatment Cyramza helped increase profits, bringing a total of $270.6 billion in the third-quarter. Eli Lilly lifted its guidance for full-year 2015. They expect earnings per share in the range of $2.40 and $2.45, from prior guidance of $2.20 to $2.30.

Despite the stronger third-quarter financial results, I believe Eli Lilly is overvalued. Eli Lilly discovers, develops, manufactures, and sells pharmaceutical products for humans and animals worldwide. The drug maker recently stopped development of the cholesterol treatment evacetrapib because the drug wasn’t effective. Eli Lilly deployed a substantial amount of capital to fund Evacetrapib, which was in Phase 3 research, until they decided to pull the plug on it. The suspension to the development of Evacetrapib is expected to result in a fourth-quarter charge to research and development expense of up to $90 million pre-tax, or about $0.05 per share after-tax. Eli Lilly’s third-quarter operating expense declined 7% year-over-year, mainly due to spending on experimental drugs that failed in late-stage testing trials.

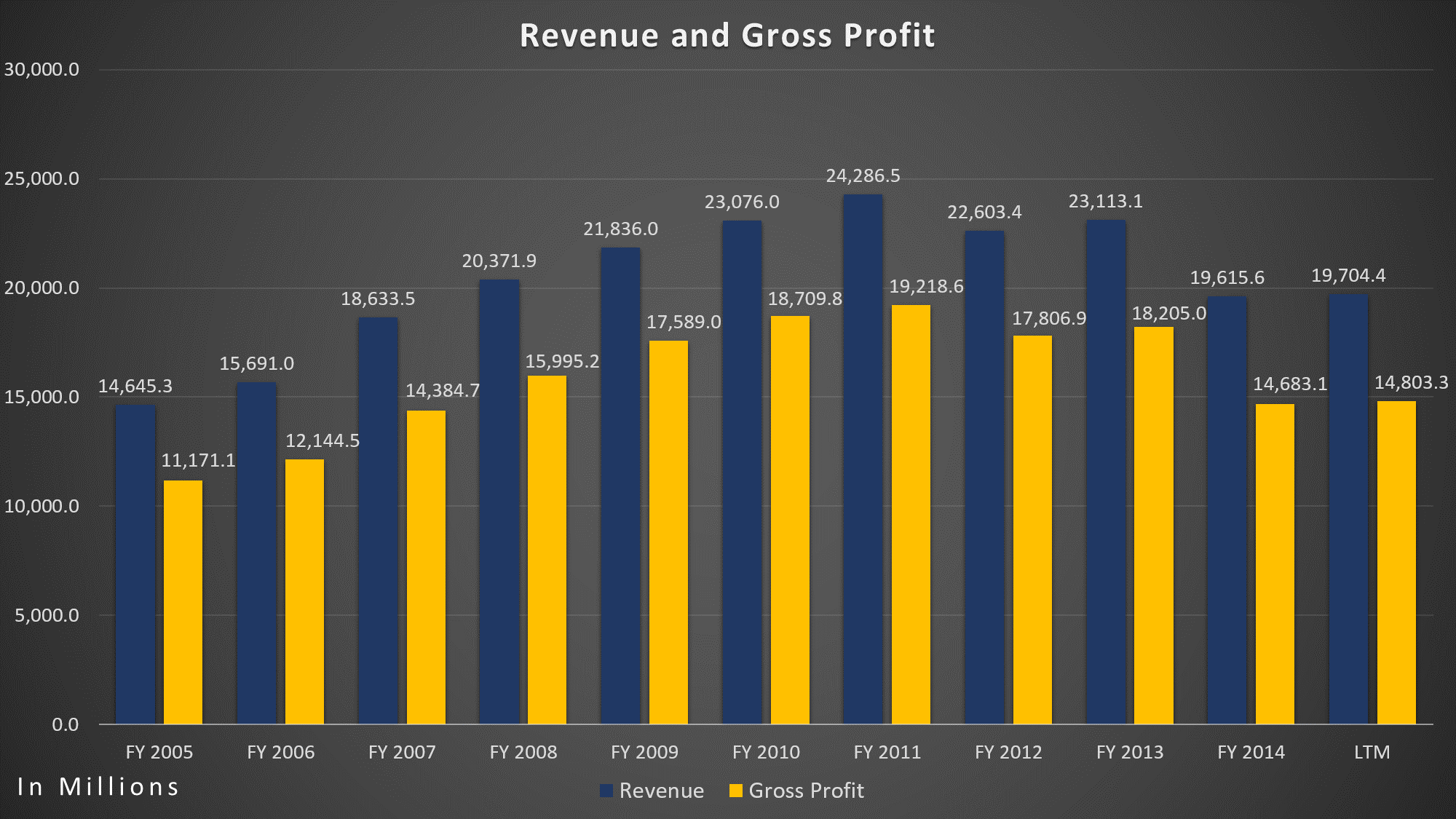

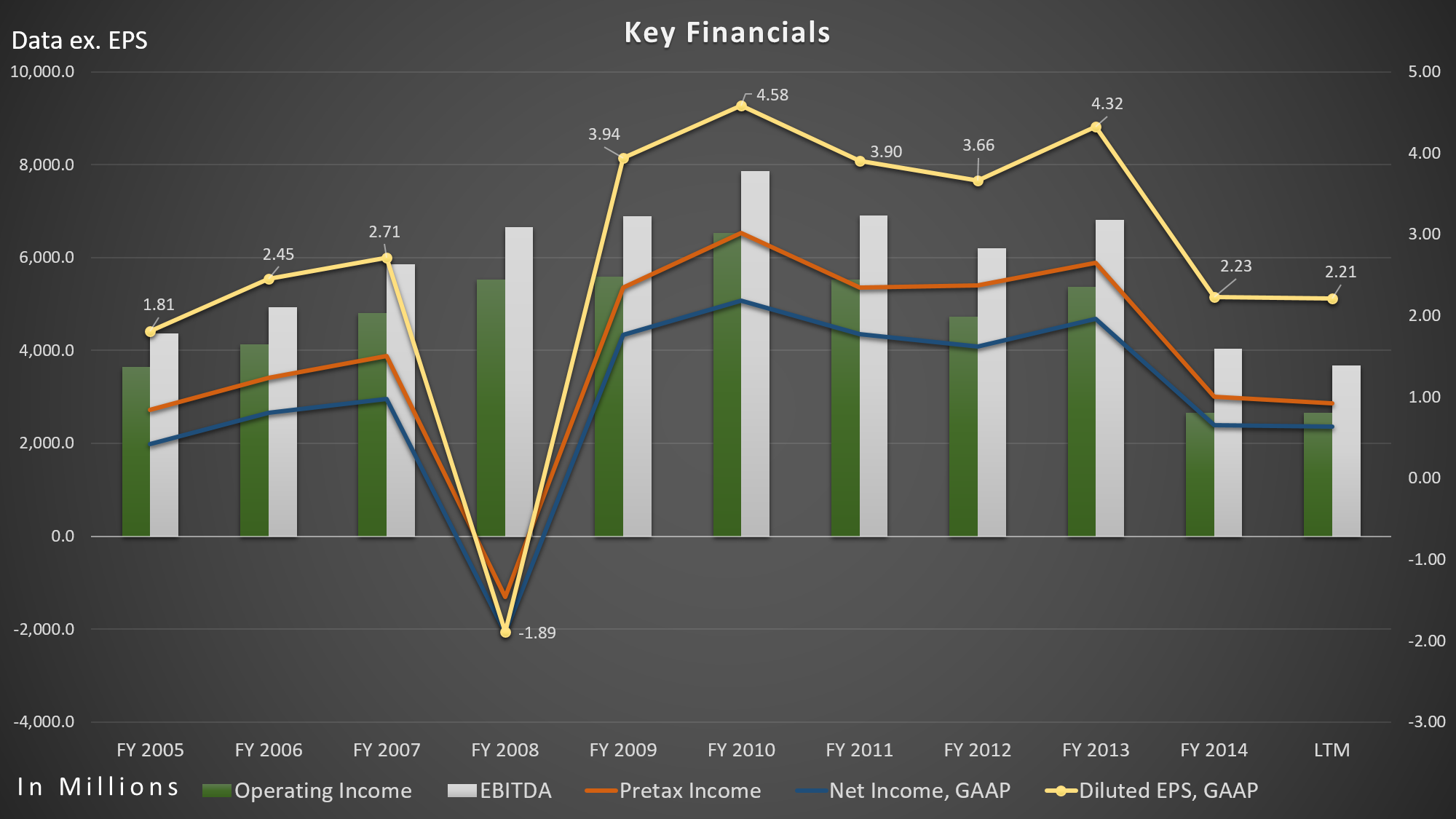

Eli Lilly’s market capitalization skyrocketed over the past five years by 122.76% to $90 billion, but their revenue, gross profit, net-income, operating income, as well as EBITDA, declined significantly. Over the past five years, its revenue decreased 14.61% from $23.08 billion to $19.70 billion (LTM), largely due to patent expirations. Gross profit and net-income declined 26.06% and 53.48%, respectively. Its operating income fell 59.18% over the past five years.

Eli Lilly – Revenue/Gross Profit

Eli Lilly – Key Financials

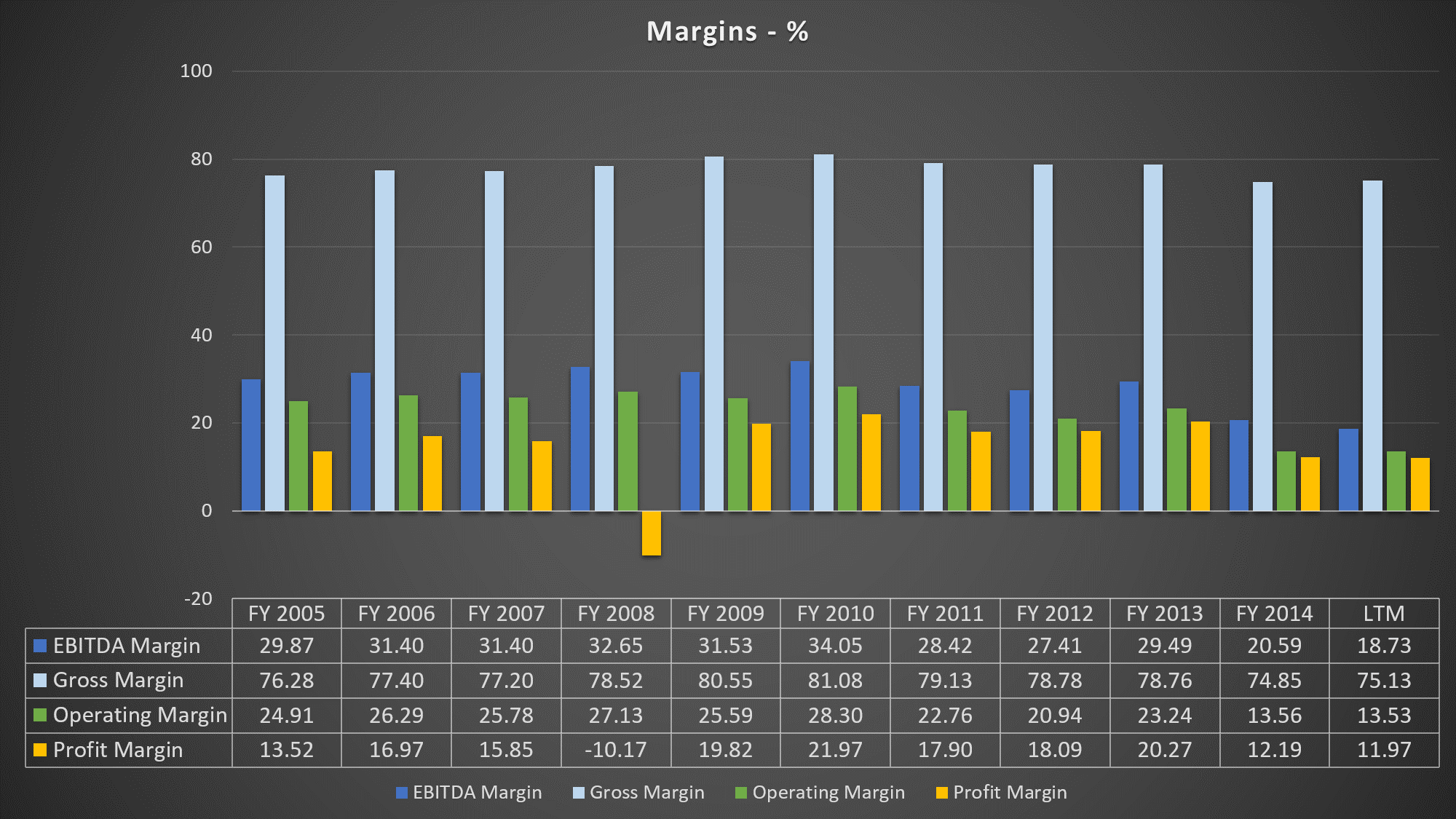

Its operating margin fell a halfway over the past five years from 28.30% to 13.53% (LTM). EBITDA margin, on the other hand, fell all the way to 18.73% (LTM) from 34.05%.

Eli Lilly – Key Margins

Meanwhile, shares of Eli Lilly gained 144.49% over the past five years. Its price-to-sales ratio too high compared to its history and to S&P 500. Its Price/Sales ratio currently stands at 4.6, vs. at 1.7 in 2010, while S&P 500 currently stays at 1.8 and industry average at 3.9. In addition to the falling revenue, gross profit, net-income, and EBITDA, its free cash flow fell significantly over the past five years by 72.24%, or fell 22.61% on a compounded annual basis.

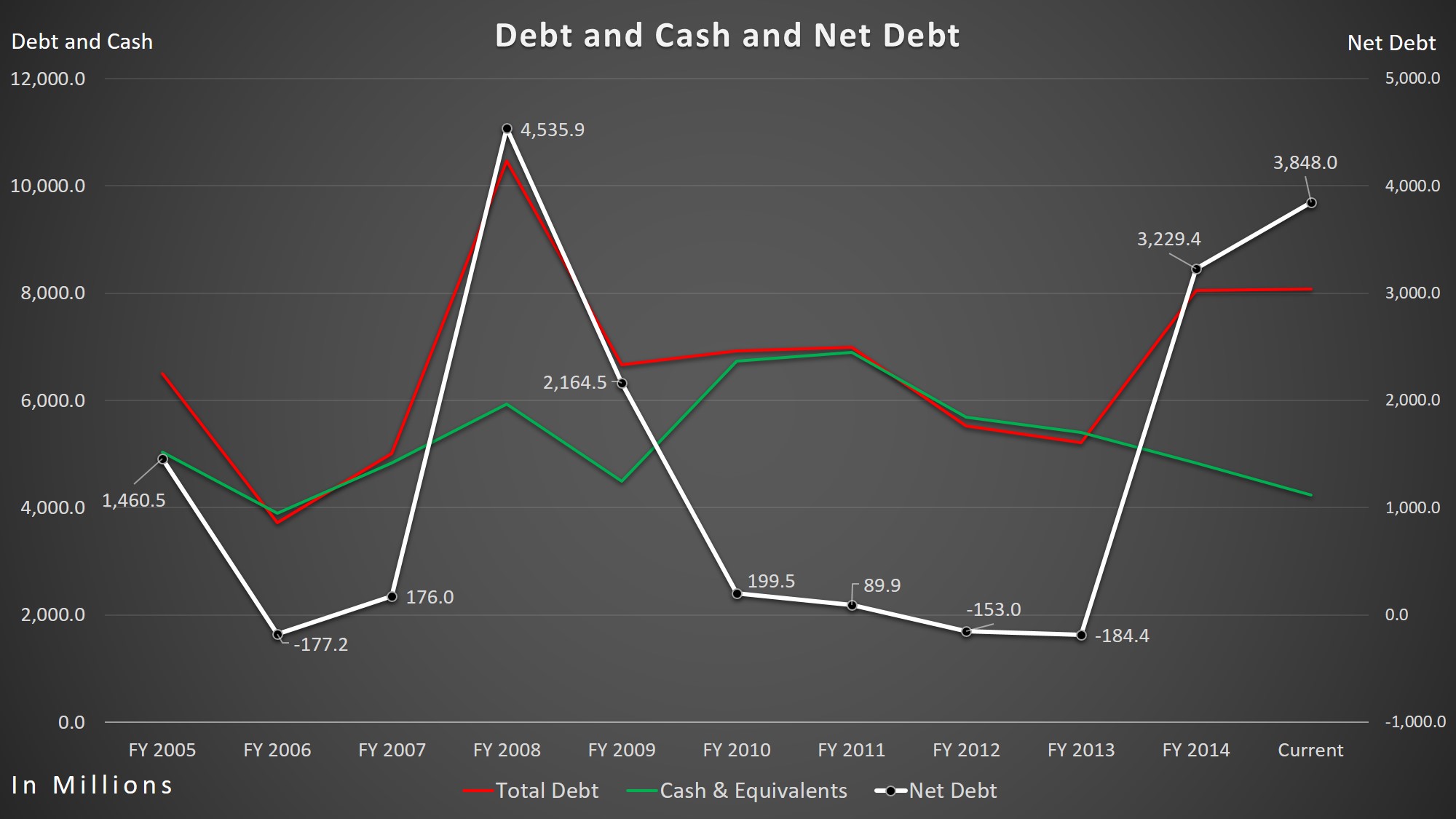

Not only did their cash flow fall, but their net-debt increased significantly. Its net-debt increased by a whopping 1789.87% over the past five years from $199.5 million to $3.85 billion. They now have almost twice as much of total debt than they do in cash and equivalents. I believe Eli Lilly is at a risk for poor future ratings by rating agencies, which will increase their borrowing costs.

Eli Lilly – Total Cash/Total Cash/Net-Debt

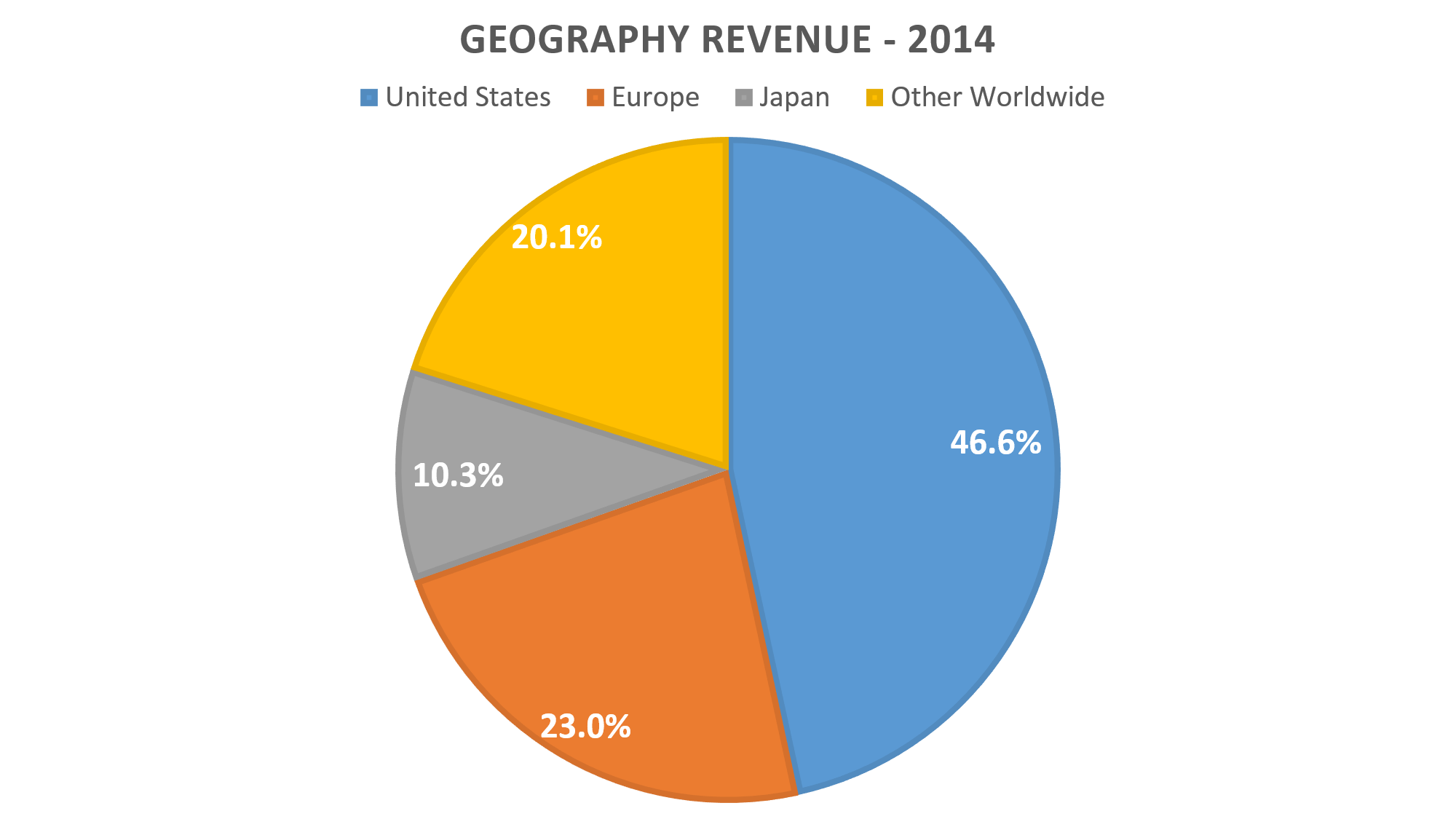

Strong U.S. dollar is an issue for Eli Lilly. Over the past five years, the dollar index increased 26.75%. Last quarter, its 49.2% of revenue came from foreign countries. Its revenue in the U.S. increased 14% to $2.54 billion, while revenue outside the U.S. decreased 9% to $2.42.

Eli Lilly – 2014 Geography Revenue

Eli Lilly’s dividend yield of 2.55% or 0.50 cents per share quarterly can be attractive, but it is undesirable. From 1995 through 2009 (expectation of 2003-2004), Eli Lilly raised its dividend. Payouts of $0.26 quarterly in 2000 almost doubled to $0.49 in 2009. Then, the company kept its dividend payment unchanged in 2010, the same year when its net-income, EBITDA and earnings per share (EPS) reached an all-time high. About four years later (December 2014), Eli Lilly increased the dividend to $0.50 quarterly. I still don’t see a reason to buy shares of Eli Lilly. The frozen divided before the recent increase was a signal that the management did not see earnings growing. With expected patent expiration of Cymbalta, their top selling drug in 2010, it is no wonder Eli Lilly’s key financials declined and dividends stayed the same. Cymbalta sales were $5.1 billion in 2013, the year its patent expired. In 2014, its sales shrank all the way down to $1.6 billion. Loss of exclusivity for Evista in March 2014 immensely reduced Eli Lilly’s revenue rapidly. Sales decreased to $420 million in 2014, followed by $1.1 billion in 2013. Pharmaceuticals industry continues to lose exclusivities, including Eli Lilly.

In December 2015, Eli Lilly will lose a patent exclusivity for antipsychotic drug Zyprexa in Japan and for lung cancer drug Alimta in European countries and Japan. Both of the drugs combined accounted for revenue of $866.4 million in the third-quarter, or 17.5% of the total revenue. They will also lose a patent protection for the erectile dysfunction drug Cialis in 2017, which accounted for $2.29 billion of sales in 2014, or 11.68% of the total revenue.

Besides the pressure from patent expirations, there is also regulatory pressures on drug pricing. According to second-quarter 10Q filing, Eli Lilly believes “State and federal health care proposals, including price controls, continue to be debated, and if implemented could negatively affect future consolidated results of operations.” During the third-quarter earnings call, CEO of Eli Lilly, John C. Lechleiter, said that price increases reflects many of medicines going generic and “deep discounts” government mandates for large purchasers.

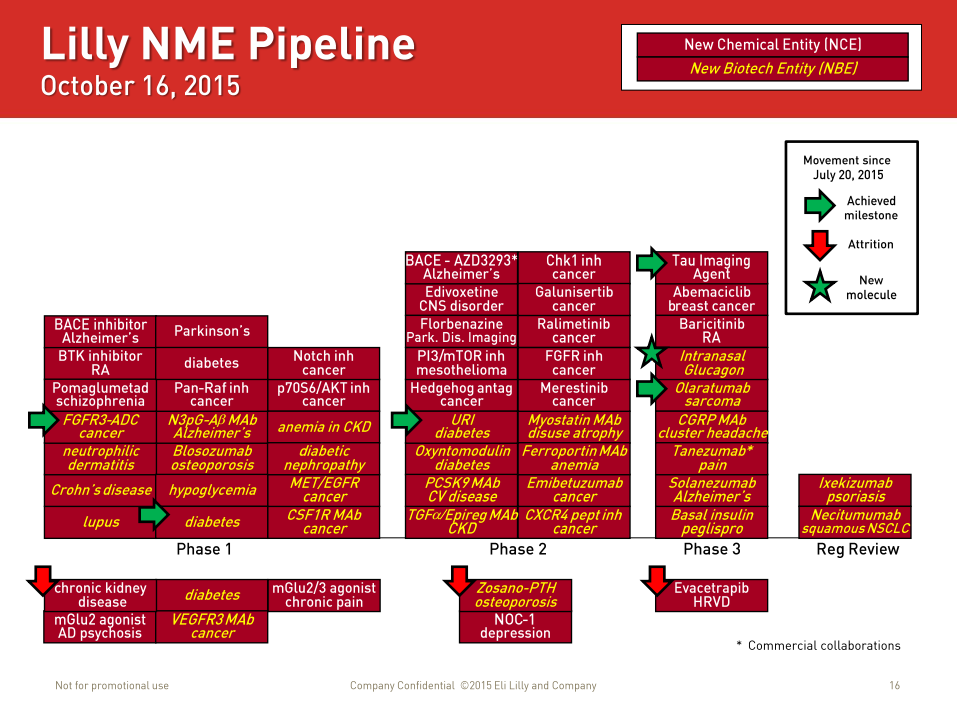

As of October 16, Eli Lilly had two drugs under regulatory review, nine drugs in Phase 3 testing, and 18 drugs in Phase 2 testing. Since the end of July, the drug maker terminated the development of few drugs, including evacetrapib in Phase 3, two drugs in Phase 2, and five in Phase 1. Out of total eight drug termination, only five drugs moved to the next stage of testing. I view the recent termination of evacetrapib as a major setback.

Compared to its peers, LLY’s Price-to-Earnings ratio is too high. Its P/E ratio (on GAAP basis) stands at 38.22 while industry average stands at 17.7. Four of its main peers, Pfizer (PFE), Johnson & Johnson (JNJ), Merck (MRK), and Sanofi (SNY) P/E ratio stands at 24.08, 19.63, 14.41, and 22.38, respectively.

Negative trends, tighter regulations, increasing competition and slowing growth makes Eli Lilly’s current valuation unjustified. I believe it will reach an average P/E ratio of its four main competitors, at 20.12, in the next three years. I expect EPS (GAAP) to contract. With current EPS of $2.21 (LTM, GAAP) and P/E ratio of 20.12, share price would be worth $44.46, down 47.37% from current share-price of $84.47. As EPS contracts, the share price of Eli Lilly will be much further down from $44.46 in the next three years.

Disclosure: I’m not currently short on the stock, LLY, at this time (October 21, 2015).

Note: All information I used here such as revenue, margins, EBITDA, etc are found from Eli Lilly and Company’s official investor relations site, Bloomberg terminal and morningstar. The pictures you see here are my own, except “Eli Lilly Pipeline – Third Quarter Earnings Presentation – Page 16”

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.

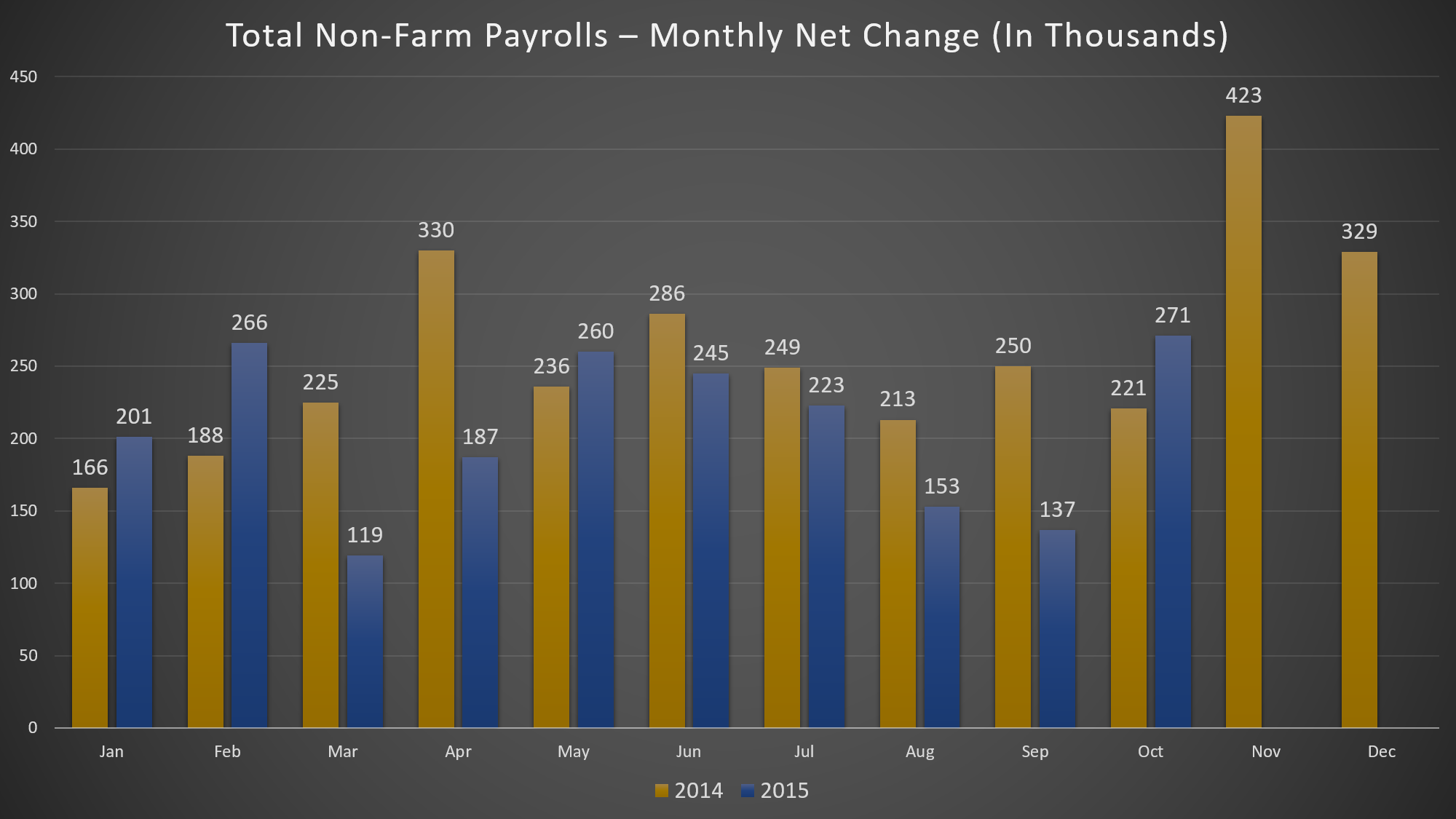

On November 6 (Friday), jobs report for October had the winds of 120 miles per hour and blew everyone away. Non-farm payrolls showed 271,000 jobs were added in October, the most gain since December and a huge beatdown on expectations of about 185,000. It’s the best month for job growth so far this year. The report follows two consecutive months (August and September) of weak jobs growth below 160,000.

The total job gains for August and September were revised 12,000 higher. August was revised 17K higher to 153K from 136k, and September was revised -5K lower to 137K from 142K. Over the last 12 months, employment growth had averaged 230K per month, vs. 222K in the same-period of 2014. In 2014, average monthly payrolls was 260K. This year, it is 206K. Not only jobs gains for October were strong, but also unemployment and wages.

Total Non-Farm Payrolls – Monthly Net Change

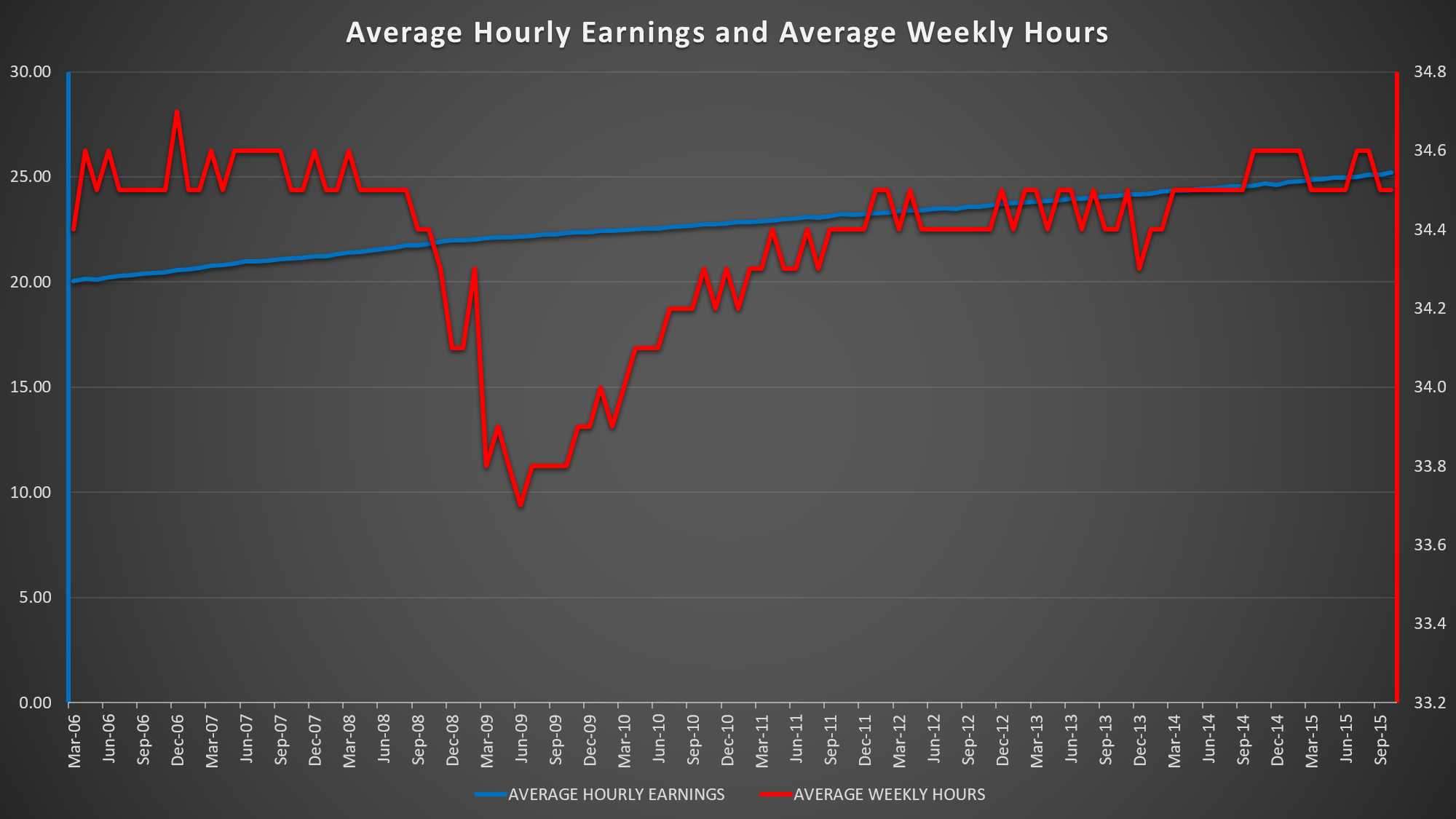

The unemployment rate dipped 0.1% to 5%, its lowest level since April 2008. Average hourly earnings rose by 9 cents an hour to $25.20. It rose 2.5% year-over-year (Y/Y), the best level since July 2009. For most of the “recovery”, wages has been flat. The increase in earnings is significant for two reasons. More money for employees means more spending (don’t forget debts), which accounts two-thirds of the economy. Second, wage growth might suggest that employers are having trouble finding new workers (should I say “skilled” workers) and they have to pay more to keep its workers and/or to get new skilled workers. This could draw more people back into the labor market, increasing the participation rate. Without the right skills, good luck.

Average Hourly Earnings and Average Weekly Hours

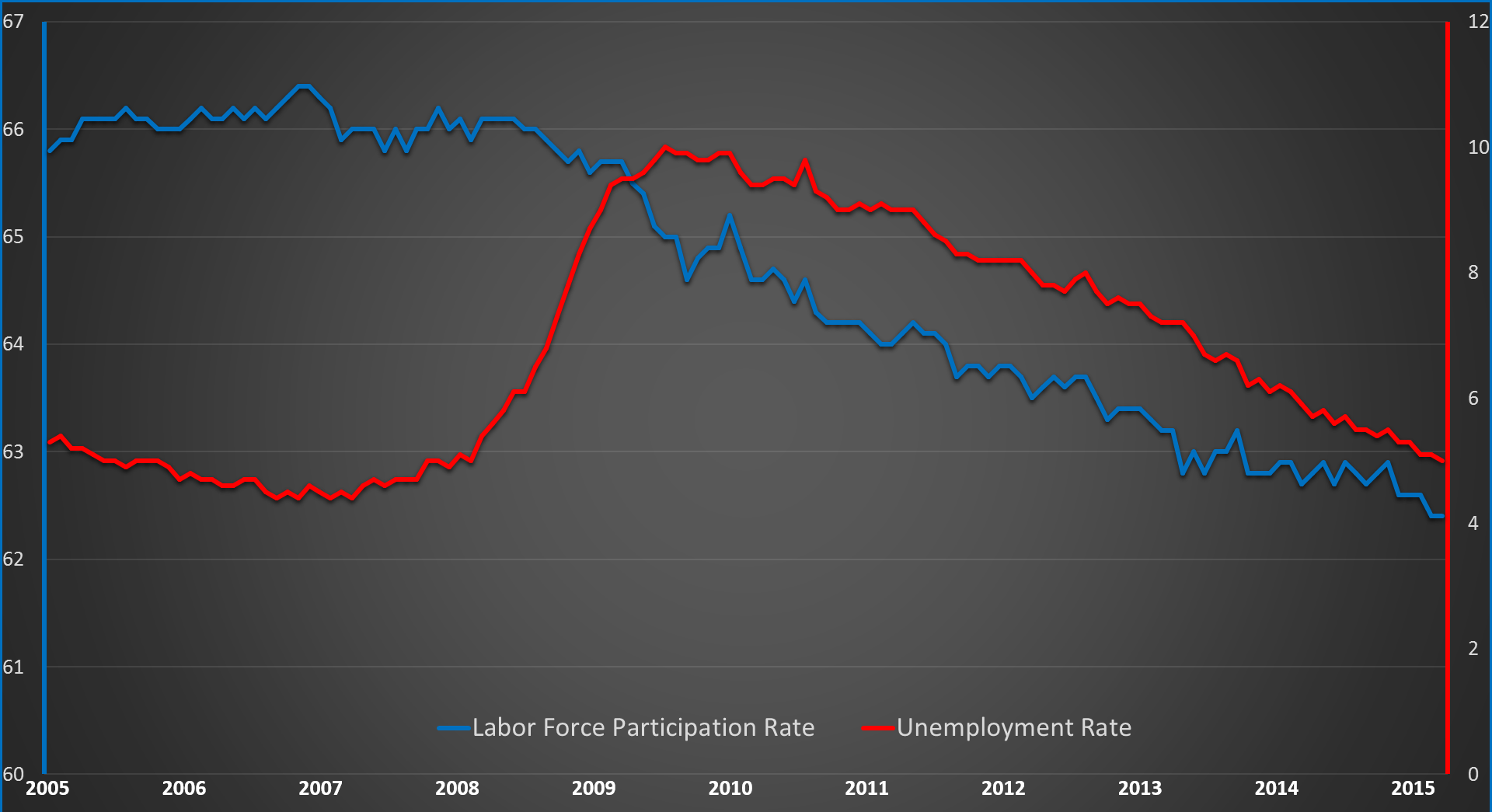

The labor force participation rate remained unchanged at a 38-year (1977) low of 62.4%. The long-term decline in the participation rate is due to the aging of the baby-boom generation and loss of confidence in the jobs market. There hasn’t even been a rebound in participation rate of prime-age Americans (between the ages of 25 and 54).

Unemployment Rate + Labor Force Participation Rate

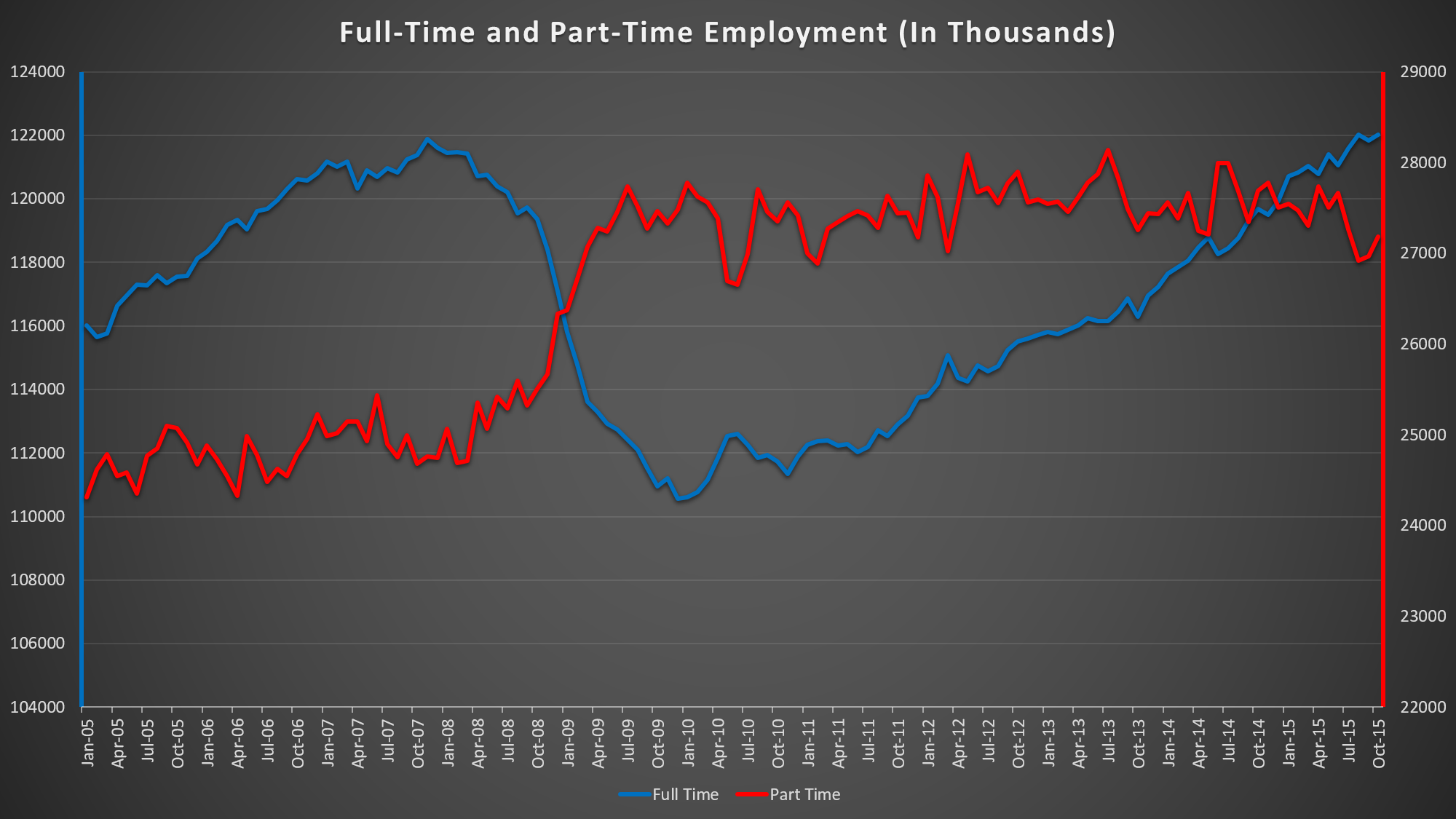

More than 122 million Americans had full-time jobs at the end of October, the highest since December 2007 (121.6 million).

Full-Time and Part-Time Employment

Immediately after the jobs report, the probability of a rate-hike in December lifted. Fed funds futures currently anticipates about 65% chance of a rate hike next month vs. about 72% immediately after the report and about 55% before the report.

Federal Reserve Chairwoman, Janet Yellen, lately has been saying that December’s Federal Open Market Committee (FOMC) meeting was “live” for a potential rate-hike. While this jobs report is positive, I believe it is too early to jump in on conclusions.

The policymakers should not be too quick to act on one report. In September, the Fed left rates unchanged mainly due to a low inflation. Inflation is still low and we will get a fresh look on Tuesday (November 17) when Consumer Price Index (CPI) is released.

Right after the jobs report, the dollar skyrocketed and was 40 cents away from hitting $100 mark. It’s currently at $98.88 and there is a very high chance it will go above $100 until December 15, the first day of FOMC meeting.

If the November job numbers does not surprise to the upside (released in December 4), inflation stays low, and the dollar keeps strengthening, I do not believe the Fed will hit the “launch” button for a rate-hike liftoff.

Market Reactions:

US Dollar (“/DX” on thinkorswim platform) – HourlyS&P 500 Index (“SPX” on thinkorswim platform) – Hourly

On October 22 (Thursday), European Central Bank (ECB) left rates unchanged, with interests on the main refinancing operations, marginal lending, and deposit rate at 0.05%, 0.30% and -0.20, respectively. But the press conference gave an interesting hint. Mario Draghi, the President of ECB, was most dovish as he could be, “work and assess” (unlike “wait and see” before).

The central bank is preparing to adjust “size, composition and duration” of its Quantitative Easing (QE) program at its December meeting, “the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting”, Draghi said during the press conference. They are already delivering a massive stimulus to the euro area, following decisions taken between June 2014 and March 2015, to cut rates and introduce QE program. In September 2014, ECB cut its interest rate, or deposit rate to -0.20%, a record low. Its 1.1 trillion euros QE program got under way in March with purchases of 60 billion euros a month until at least September 2016.

When ECB cut deposit rate to record low in September 2014, Mr. Draghi blocked the entry to additional cuts, “we are at the lower bound, where technical adjustment are not going to be possible any longer.” (September 2014 press conference). Since then, growth hasn’t improved much and other central banks, such as Sweden and Switzerland, cut their interest rates into much lower territory. Now, another deposit rate-cut is back, “Further lowering of the deposit facility rate was indeed discussed.” Mr. Draghi said during the press conference.

The outlook for growth and inflation remains weak. Mr. Draghi – famous for his “whatever it takes” line – expressed “downside risks” to both economic growth and inflation, mainly from China and emerging markets.

Given the extent to which the central bank provided substantial amount of stimulus, the growth in the euro area has been disappointing. The euro area fell into deflation territory in September after a few months of low inflation. In September, annual inflation fell to 0.1% from 0.1% and 0.2% in August and July, respectively. Its biggest threat to the inflation is energy, which fell 8.9% in September, down from 7.2% and 5.6% in August and July, respectively.

As the ECB left the door open for more QE, Euro took a dive. Euro took a deeper dive when Mr. Draghi mentioned that deposit rate-cut was discussed. Deposit rate cut will also weaken the euro if implemented. After the press conference, the exchange rate is already pricing in a rate-cut. Mentions of deposit rate-cut and extra QE sent European markets higher and government bond yields fell across the board. The Euro Stoxx 50 index climbed 2.6%, as probability of more easy money increased. Swiss 10-year yield fell to fresh record low of -0.3% after the ECB press conference. 2-year Italian and Spanish yields went negative for the first time. 2-year German yield hit a record low of -0.32.

Regarding the exchange rate (EUR/USD), I expect it to hit a parity level by mid-February 2016.

As I stated in the previous posts, I expect more quantitative easing by ECB (and Bank of Japan also). I’m expecting ECB to increase its QE program to 85 billion euros a month and extend it until March 2017. When ECB decides to increase and extend the scope of its QE, I also expect deposit rate-cut of 10 basis points.

ECB will be meeting on December 3 when its quarterly forecasts for inflation and economic growth will be released. The only conflict with this meeting is that U.S. Federal Reserve policy makers meets two weeks later. ECB might hold off until the decision of the Fed, but the possibility of that is low.

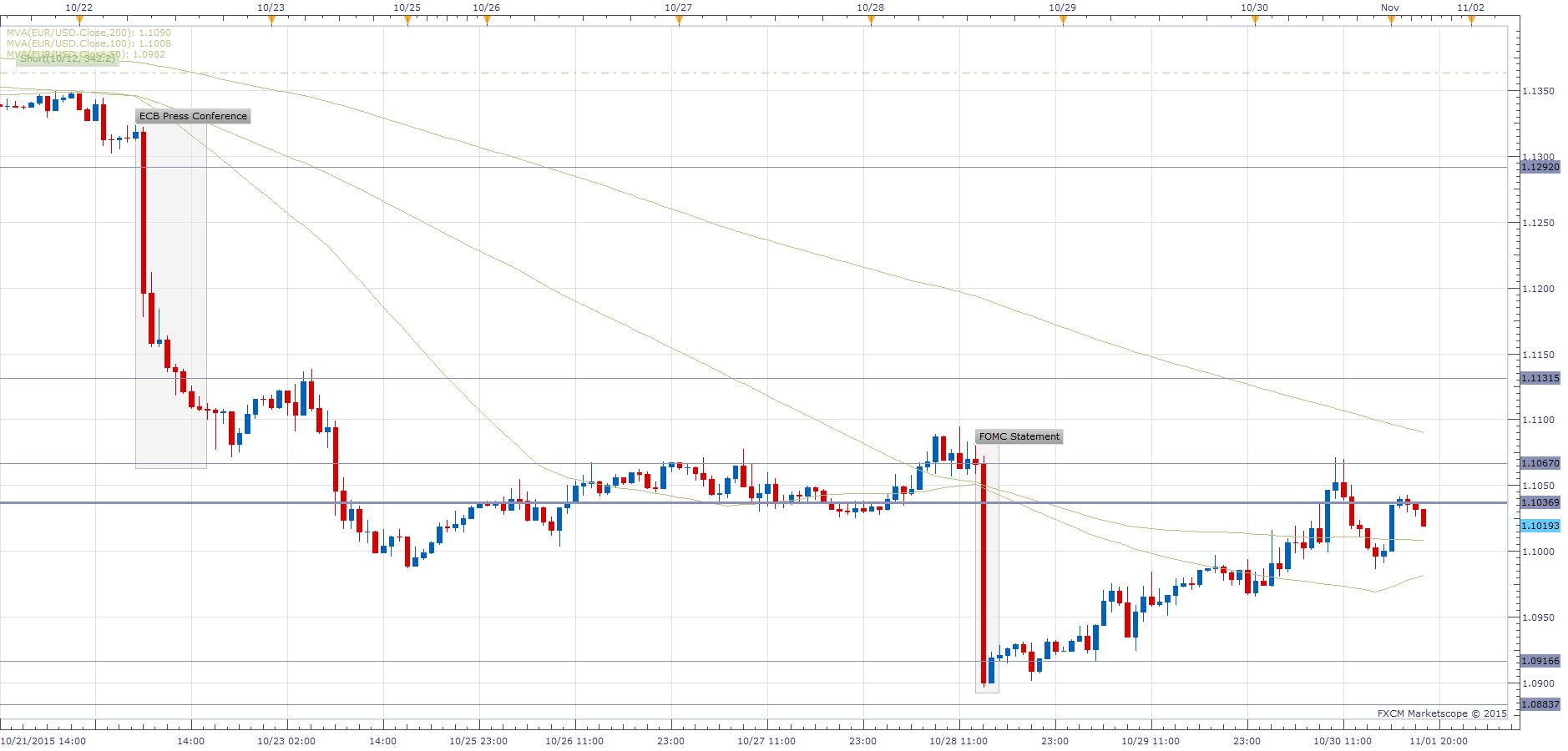

EUR/USD Reaction:

EUR/USD – Hourly Chart

U.S. Federal Reserve:

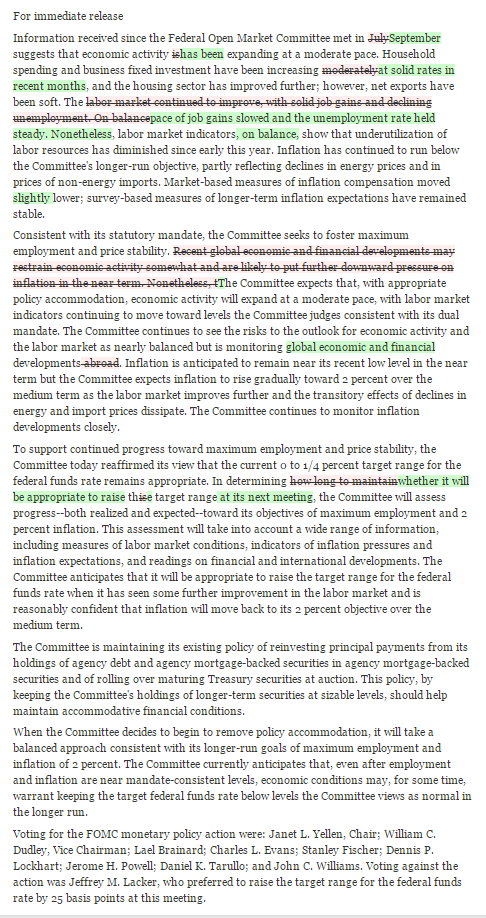

On October 28 (Wednesday), the Federal Reserve left rates unchanged. The bank was hawkish overall. It signaled that rate-hike is still on the table at its December meeting and dropped previous warnings about the events abroad that poses risks to the U.S. economy.

It does not make sense to drop “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” (September statement) I’m sure the events abroad has its risks (spillover effect) to the U.S. economy and the Fed will keep an eye on them.

In its statement, it said the U.S. economy was expanding at a “moderate pace” as business capital investments and consumer spending rose at “solid rates”, but removed the following “…labor market continued to improve…” (September statement). The pace of job growth slowed, following weak jobs report in the past several months.

Let’s take a look at the comparison of the Fed statement from September to October, shall we?

The Fed badly wants to raise rates this year, but conditions here and abroad does not support its mission. Next Federal Open Market Committee (FOMC) meeting takes place on December 15-16. By then, we will get important economic indicators including jobs report, Gross Domestic Product (GDP), retail spending and Consumer Price Index (CPI). If we don’t see any strong rebound, rate-hike is definitely off the table, including my prediction of 0.10% rate-hike for next month.

The report caused investors to increase the possibility of a rate increase in December. December rate-hike odds rose to almost 50% after the FOMC statement.

Greenback (US Dollar) Reaction:

U.S. Dollar ( “/DX” on thinkorswim platform) – Hourly Chart

Reserve Bank of New Zealand:

On October 28 (Wednesday), Reserve Bank of New Zealand (RBNZ) left rates unchanged at 2.75% after three consecutive rate-cuts since June. The central bank’s Governor Graeme Wheeler said that at present “it is appropriate to watch and wait.” “The prospects for slower growth in China and East Asia” remains a concern.

Housing market continues to pose financial stability risk. House price inflation is way higher. Median house prices are about nine times the average income. Short supply caused the house prices to increase significantly. “While residential building is accelerating, it will take some time to correct the supply shortfall.” RBNZ said in a statement. Auckland median home prices rose about 25.4% from September 2014 to September 2015, “House price inflation in Auckland remains strong, posing a financial stability risk.”

Further reduction in the Official Cash Rate (OCR) “seems likely” to ensure future CPI inflation settles near the middle of the target range (1 to 3%).

Although RBNZ left rates unchanged, Kiwi (NZD) fell because the central bank sent a dovish tone, “However, the exchange rate has been moving higher since September, which could, if sustained, dampen tradables sector activity and medium-term inflation. This would require a lower interest rate path than would otherwise be the case.” It’s a strong signal that RBNZ will cut rates to 2.5% if Kiwi continues to strengthening. I will be shorting Kiwi every time it strengthens.

“The sharp fall in dairy prices since early 2014 continues to weigh on domestic farm incomes…However, it is too early to say whether these recent improvements will be sustained.” RBNZ said in the statement. Low dairy prices caused RBNZ to cut rates. New Zealand exports of whole milk powder fell 58% in the first nine months of this year, compared with the same period in 2014. But, there’s a good news.

Recent Chinese announcement that it would abolish its one-child policy might just help increase dairy prices, as demand will increase. How? New Zealand is a major dairy exporter to China. Its milk powder and formula industry is likely to benefit from a baby boomlet in China.

BoJ expects to hit its 2% inflation target in late 2016 or early 2017 vs. previous projection of mid-2016. Again and Again. This is the second time BoJ changed its target data. The last revision before this week was in April. It also lowered its growth projections for the current year by 0.5% to 1.2%.

They also lowered projections for Core-CPI, which excludes fresh food but includes energy. They lowered their forecasts for this fiscal year to 0.1%, down from a previous estimate of 0.7%. For the next fiscal year, they expect 1.4%, down from a previous estimate of 1.9%. Just like other central banks, BoJ acknowledged that falling energy prices were hitting them hard.

Low inflation, no economic growth, revisions, revisions, and revisions. Nothing is recovering in Japan.

Haruhiko Kuroda, the governor of BoJ, embarked on aggressive monetary easing in early 2013. So far he hasn’t had much success.

In the second quarter (April-June), Japan’s economy shrank at an annualized 1.2%. Housing spending declined 0.4% in September from 2.8% in August. Core-CPI declined for two straight months, falling 0.1% year-over-year both in September and August. Annual exports only rose 0.6% in September, slowest growth since August 2014, following 3.1% gain in August.

Exports are part of the calculation for Gross Domestic Product (GDP). Another decline in GDP would put Japan into recession, which could force BoJ to ease its monetary policy again. Another recession would be its fourth since the 2008 financial crisis and the second since Shinzo Abe (Abenomics), the Prime Minister of Japan, came to power in December 2012.

Its exports to China, Japan’s second-biggest market after the U.S., fell 3.5% in September. The third-quarter (July-September) GDP report will be released on November 16.

April 2014 sales tax (sales tax increased from 5% to 8%) increase only made things worse in Japan. It failed to boost inflation and weakened consumer sentiment.

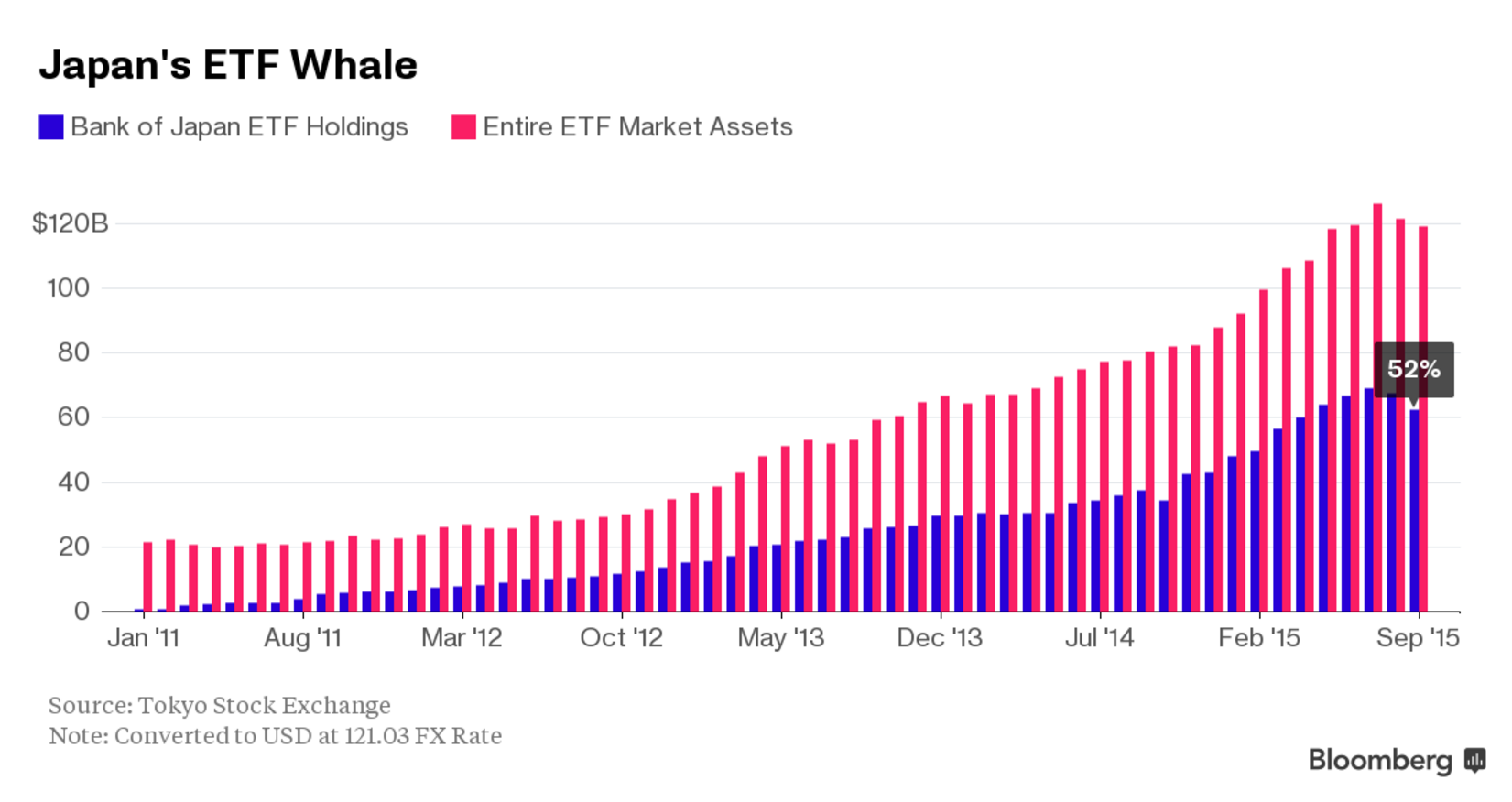

In April 2013, BoJ expanded its QQE (or QE), buying financial assets worth 60-70 trillion yen a year, including Exchange Traded Funds (ETF).

QQE stands for Quantitative and Qualitative Easing. Qualitative easing targets certain assets to drive up their prices and drive down their yield, such as ETF. Quantitative Easing targets to drive down interest rates. Possibility of negative interest rates has been shot down by BoJ. But, why trust BoJ for their word? Actions speak louder than words.

In October 2014, BoJ increased the QQE to an annual purchases of 80 trillion yen. When is the next expansion? December?

Did you know that the BoJ owns 52% of Japan’s ETF market?

For over a decade, BoJ’s aggressive monetary easing through asset purchases did not help Japan’s economy. Since 2001, the central bank operated 9 QEs and is currently operating its current 10th QE (or QQE). The extensions of its QE are beginning to become routine or the “new normal.”

Growth and prices are slowing in China, with no inflation in United Kingdom, Euro-zone, and the U.S. The chances that Japan will crawl out of deflation are very slim.

USD/JPY Reaction:

USD/JPY – Hourly Chart

US Market Reactions (ECB and FOMC):

S&P 500 (“SPX”) – Hourly Chart

Next week, both Reserve Bank of Australia (RBA) and Bank of England (BoE) will meet. Will be very interesting to watch.

Last Wednesday (October 7, 2015), I had a chance to meet Ben Bernanke, former chairman of the Federal Reserve and the most powerful man in the world (well, was).

Not that I got a handshake, but got to ask a question.

So how did I get to meet him? It was part of WSJ Pro Central Banking events.

Recently, Wall Street Journal introduced a subscription service, “WSJ Pro”. It debuted with WSJ Pro Central Banking. Its parent company, Dow Jones, describes it as a “premium suite of industry and subject-specific content services, combining news, data, and events in a single membership platform.” The key word is “events”. “Events” is what I love about the subscription. “Events” in other words mean, meeting high-profile people and networking with people in the financial industry.

I had a free access for a while, but now that’s gone. During my trial, I registered for two events, “Breakfast Interview Series: William Dudley” and “Breakfast Interview Series: Ben Bernanke”. I was lucky enough to be chosen to go to both of them.

The event with William Dudley, President of the Federal Reserve Bank of New York, took place on September 28. Did not get a chance to ask a question. Nevertheless, great event. Full video of the interview can be found here.

The event with Ben Bernanke took place on October 7. I was so excited for this particular event. Well, who doesn’t want to meet Ben Bernanke? I woke up on 4:30 in the morning and left my house at 6:45 AM. I got to the location of the event by about 7:50. When I checked in, I got an autographed copy of Mr. Bernanke’s new book, “The Courage to Act.” Signed, Sealed, Delivered.

It wasn’t until 8:30 AM when Mr. Bernanke entered the room, getting me and others excited. Along with him, there was WSJ’s Chief Economics Correspondent, Jon Hilsenrath, who also interviewed William Dudley the week before.

During the Q&A session, I got a chance to ask a question. I was so excited and confident. I strongly believed that I was not nervous at all. But, that wasn’t the case.

When I got handed the microphone, I instantly went blind. I forgot most of what I was going to say. It was like Warren Buffett, my idol, interviewing me for a job.

The first word out of my mouth was “student”, when I actually should have stated my name. Asking a question to a person like Ben Bernanke got me so nervous, I mumbled and rambled during my question. My question basically was, “If you were the president, what would you do about the taxes, corporate taxes, which is too high?”

Full video of the interview can be found here. I can be heard asking the question at 42:30.

I asked it because I strongly believe U.S. corporate taxes are too high, causing inversions. Although I got a reasonable answer, I believe I would have gotten better answer if I asked the question in a different way.

My first encounter with a high-profile person made me so nervous, yet taught me a big lesson. It significantly improved my confidence and ability to ask a question (to a high-profile person) without being so nervous. Who’s the next high-profile person I will meet? Janet Yellen?

A short video of Mr. Bernanke leaving the “stage”

A picture of Mr. Bernanke leaving the “stage”

I will forever remember this day, October 7, 2015.

Thank you, Wall Street Journal.

UPDATE: At the event when I was asking the question,