Failure of trial III Alzheimer drug, Solanezumab, is a major setback for Eli Lilly.

Lilly’s spending relative to the industry is following the same pattern as in 2005 and 2007, before its stock price got cut in half in over a year.

While Lilly is strengthening its pipeline in the diabetes space, it will not be enough to stop the stock from continuing to fall as they face stiff competition.

Four drugs accounting for 29.6%, or almost $1.5 billion of its third-quarter sales, are due to lose their compound protection this month and next year.

About two weeks ago, my second article was approved on Seeking Alpha. The article is about FireEye (NASDAQ: FEYE). The first article was about Eli Lilly and Company (NYSE: LLY)

If you have any questions/suggestions, feel free to contact me anytime. Thank you.

Summary

FireEye acquired four companies in the last three years.

Issued nearly $900 million in debt and continues to lose money.

Possible secondary offering, diluting shareholders’ equity further.

Founded in 2004, FireEye (NASDAQ:FEYE) has grown exponentially. The importance of security is extremely vital, and the demand for security continues to increase as cyber attacks increase and the world becomes more connected.

In 1988, after four years from the Macintosh introduction, the Internet’s first ever worm virus hit the computers. The Morris worm – one of the finest recognized worms to affect the world’s nascent cyber infrastructure – changed everything. Bugs in the code caused hundreds of systems to slow down and crash. Computer security was then no longer a science fiction.

Today, it is not just a computer security, but also smartphone security, cloud security, and so on. In short, the Internet is everywhere. As FireEye says:

“Attackers are clever, technology is complex, and experts are in short supply.”

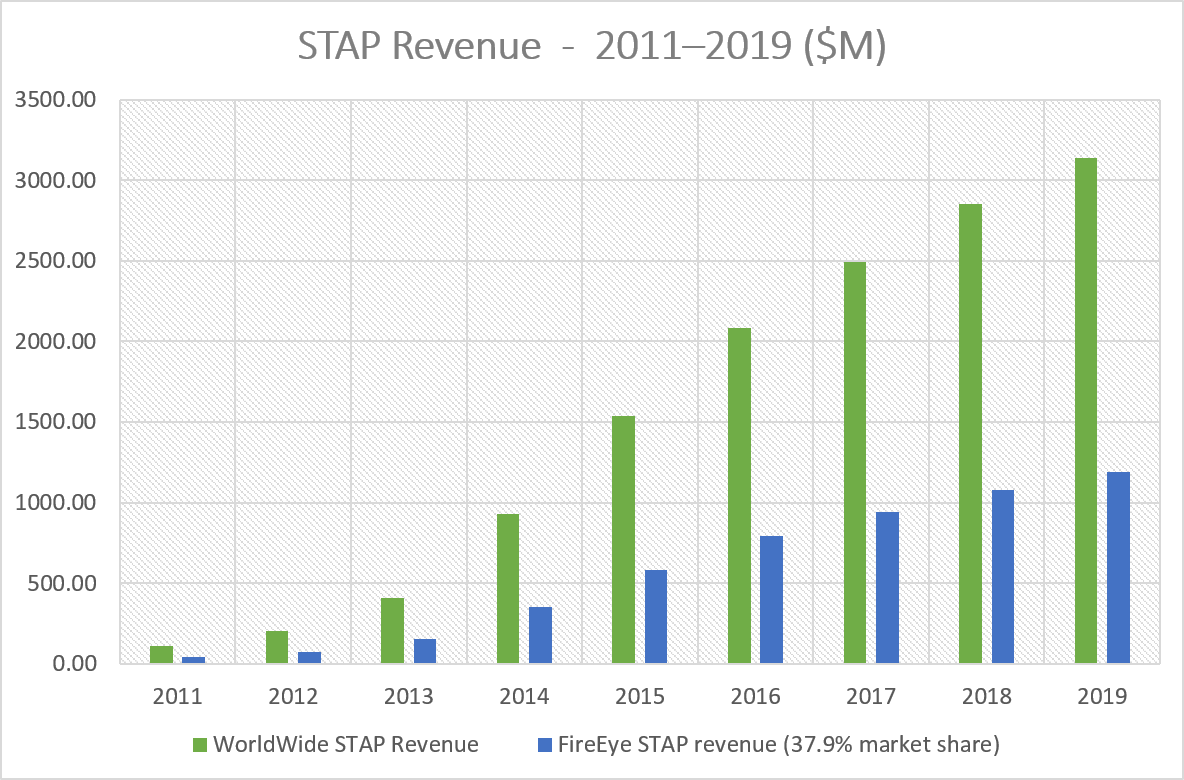

FireEye stands out in the global Specialized Threat Analysis and Protection (STAP) market. According to research firm IDC, FireEye had 37.9% of the nearly $1 billion STAP market in 2014, seven times greater than its closest competitor. The $930 million STAP market grew 126.3% from 2013. By the end of 2019, it’s expected to reach $3.14 billion, compounded annual growth rate (CAGR) of 27.6% from 2014 to 2019.

From the STAP market alone, FireEye generated $353 million in revenue, a 119.2% growth year over year (Y/Y). The STAP market revenue accounted for a whopping 82.86% of FireEye’s total $426 million revenue in 2014. If the company can maintain its 38% of share by 2019, it could be generating about $1.2 billion in revenue from that market alone.

STAP Revenue – 2011-2019 ($M)

While these are great news, there’s a disappointment. FireEye’s 37.9% share of the market in 2014 declined from 43.1% in 2013 due to a growing competition, notably from Palo Alto Networks (NYSE:PANW).

In April 2014, Palo Alto Networks acquired Israeli cyber security start-up Cyvera for nearly $180 million. In September 2014, it introduced Traps, an endpoint STAP product that was built on the technology from Cyvera.

FireEye itself admits the intense competition it operates in. In its 2015 annual filing, it recognized that “several vendors have either introduced new products or incorporated new features into existing products that compete with our solutions…independent security vendors such as Palo Alto Networks…offer products that claim to perform similar functions to our platform.”

In December 2013, FireEye acquired Mandiant, a leading provider of advanced endpoint security products and security incident response management solutions, for approximately $1.02 billion in cash and stock. Mandiant is well known for a report it published in February 2013, detailing a secretive Chinese military unit believed to be behind a long list of cyber attacks on U.S. companies.

The combination of former FireEye, attack detector, and Mandiant, attack responder, came after the Snowden leaks in June 2013. The marriage between them created a major force in the cyber security industry.

“We’ve gone from selling discrete web and email security appliances to enterprise customers to delivering a global threat management platform integrated across the network, endpoint and cloud to customers large and small.”

According to a report by Cybersecurity Ventures, the global cyber security market is expected to grow from $106.32 billion in 2015 to $170.21 billion by 2020 at a compound annual growth rate of 9.8%. In its cyber security 500 list of the world’s hottest and most innovative cyber security companies, FireEye came in first.

While FireEye may be the hottest, its stock is the ugliest. The share price of FireEye was down 35% last year while the NASDAQ 100 Technology sector has declined 2.8%. Since hitting an all-time high at $97.35 on March 2014, the stock is down 82%. The stock hit all-time lows on February 12th – the day after the fourth-quarter earnings report – at $11.35. Since then, the share price is up 55% at a current price of $17.60.

FEYE data by YCharts

In May 2014, FireEye acquired nPulse Technologies, a privately-held network forensics firm, for $56.6 million. nPulse specialized in the analytics of a cyber attack and how the attacks may have affected the networks. nPulse was a partner of FireEye prior to the acquisition. It seems FireEye benefited from the partnership with nPulse. The combination of Mandiant and nPulse gives FireEye an all-encompassing security framework.

In January 2016, FireEye acquired iSIGHT Security, a cyber threat intelligence solutions provider, for $200 million. iSIGHT is memorable for its discovery of a zero-day vulnerability – a hole in a software that is unknown to the vendor – affecting Microsoft (NASDAQ:MSFT) devices. It was used by Russian hackers to hijack and snoop on computers and servers used by NATO, the European Union, telecommunications and energy sectors.

In February 2016, FireEye acquired Invotas, a small company based in Virginia focusing on security automation and orchestration. The terms of the deal were not disclosed. FEYE said it plans to integrate the security orchestration capabilities from Invotas into the FireEye global threat management platform, “giving enterprises the ability to respond more quickly to attacks through automation,” and help customers deal with the “severe shortage of resources by automating the security process and building intelligence into their operations.”

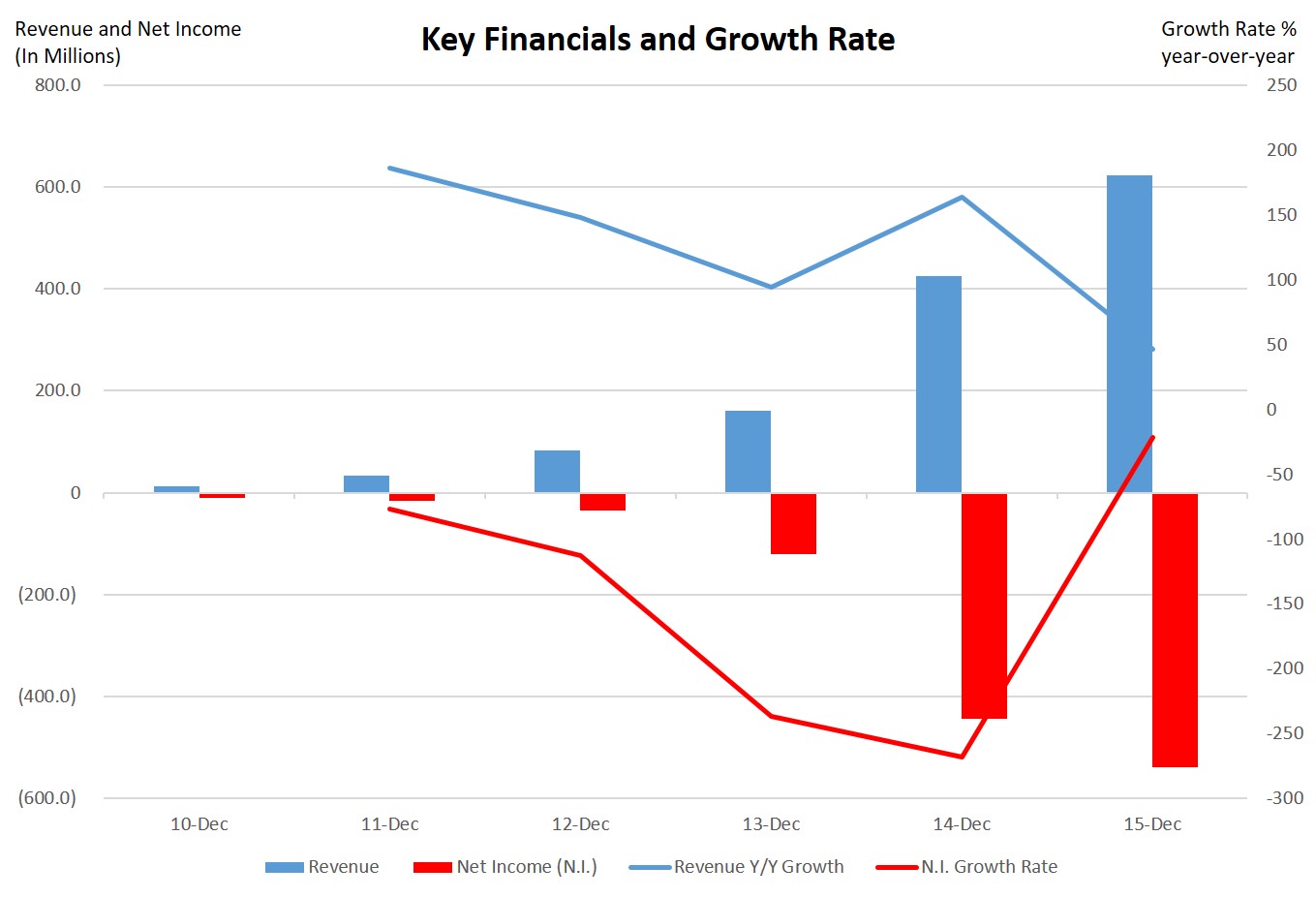

FireEye expects iSIGHT and Invotas to add approximately $60 million to $65 million to 2016 billings and approximately $55 million to $60 million to 2016 revenue. That alone would bring 7.52% to 8.15% growth to the billings Y/Y. Revenue would grow 8.83% to 8.63% Y/Y.

For the year ending December 31, FireEye expects revenue from $815 million to $845 million and billings from $975 million to $1.1 billion. If the revenue grows as expected, it represents a growth of 31% to 36% Y/Y, and the billings would grow 22% to 32% Y/Y. After subtracting the revenue growth from iSIGHT and Invotas, organic growth would range from 22.85% to 28.48%. Of course, that does not include other acquisitions. The question is what is FireEye’s real organic growth?

FireEye’s Key Financials and Growth Rate

DeWalt believes bringing FireEye, “Mandiant, iSIGHT and Invotas together, we’ve created a cyber security like no other, one with a suite of leading technologies, world-class cyber security expertise, and nation-grade threat intelligence, all brought together to form a comprehensive threat management platform.”

At the end of 2015, the company had $402.1 million in cash and cash equivalents, up from $146.4 million in the end of 2014. With short-term investment – which can be liquidated in less than a year – of $767.8 million, total cash and ST investment adds up to $1.17 billion, an increase of 190.86% from $402.2 million in 2014. Most of the increase in total cash can be attributed to the issuance of debt last year. In 2015, FireEye issued a total debt of $896.5 million. It currently has $706.2 million in debt, which I expect to increase as the company continues to lose money.

FireEye believes the existing “cash and cash equivalents and short-term investments and any cash inflow from operations will be sufficient to meet our anticipated cash needs, including cash we will consume for operations, for at least the next 12 months.” But, I do not take its word for it, considering the company loses about $135 million every quarter, or $500 million in a year. In addition to the issuance of debt, total stockholders’ equity decreased to $1.04 billion in 2015 from $1.25 billion in 2014, as the amount of common shares increased 8.8 million to 162 million. As FireEye continues to lose money, it is possible it might do a secondary offering, which will dilute shareholders’ equity further.

One sign that FireEye is investing into the future is its workforce. At the end of 2015, FireEye had approximately 3,100 employees, up from 2,500 in 2014 and 1,678 in 2013. Growing workforce shows the company is optimistic in the future. Make no mistake, FEYE is clearly positioning itself to take a bigger share of a growing industry.

I believe FireEye is a great company that has the potential to succeed in the growing security market. But, it is too early for me to be optimistic in its future stock performance, as it continues to lose money and possible secondary offering this year.

FireEye is due to report its first-quarter earnings on Thursday, May 5th.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: All information I used here such as revenue, etc are found from FireEye’s official investor relations site, SEC filings, and Bloomberg terminal. The pictures you see here including “FireEye’s Key Financials and Growth Rate” and “STAP Revenue – 2011-2019 ($M)” are my own.

On October 22, Eli Lilly (LLY) reported an increase in the third-quarter profit, as sales in its animal health segment and new drug launches offset the effect of unfavorable foreign exchange rates and patent expirations. Indianapolis-based drug maker posted a net income increase of 60% to $799.7 million, or to $0.75 per share, as its revenue increased 33% in animal health segment. In January 2015, Eli Lilly acquired Norvartis’s animal health unit for $5.29 billion in an all-cash transaction. The increase in the animal-health revenue helped offset sharp revenue decreases in osteoporosis treatment Evista and antidepressant Cymbalta, whose revenue fell 35% and 34% year-over-year, respectively. Eli Lilly lost U.S. patent protection for both drugs last year, causing patent cliffs. Lower price for the Evista reduced sales by about 2%.

Total revenue increased 2% to $4.96 billion even as currency headwinds, including strong U.S. dollar, shaved 8% off of the top line in revenue. Recently launched diabetes drug Trulicity and bladder-cancer treatment Cyramza helped increase profits, bringing a total of $270.6 billion in the third-quarter. Eli Lilly lifted its guidance for full-year 2015. They expect earnings per share in the range of $2.40 and $2.45, from prior guidance of $2.20 to $2.30.

Despite the stronger third-quarter financial results, I believe Eli Lilly is overvalued. Eli Lilly discovers, develops, manufactures, and sells pharmaceutical products for humans and animals worldwide. The drug maker recently stopped development of the cholesterol treatment evacetrapib because the drug wasn’t effective. Eli Lilly deployed a substantial amount of capital to fund Evacetrapib, which was in Phase 3 research, until they decided to pull the plug on it. The suspension to the development of Evacetrapib is expected to result in a fourth-quarter charge to research and development expense of up to $90 million pre-tax, or about $0.05 per share after-tax. Eli Lilly’s third-quarter operating expense declined 7% year-over-year, mainly due to spending on experimental drugs that failed in late-stage testing trials.

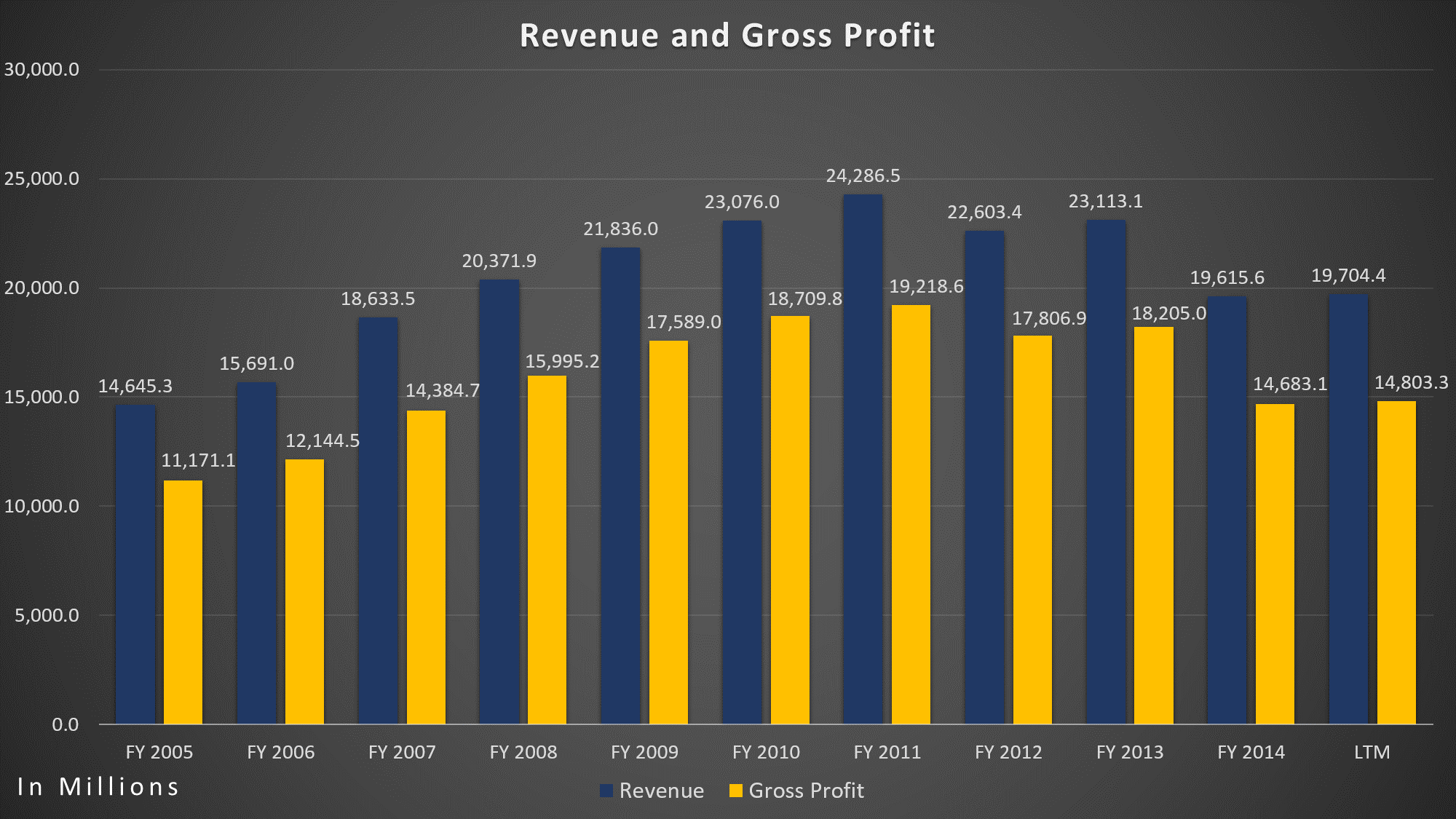

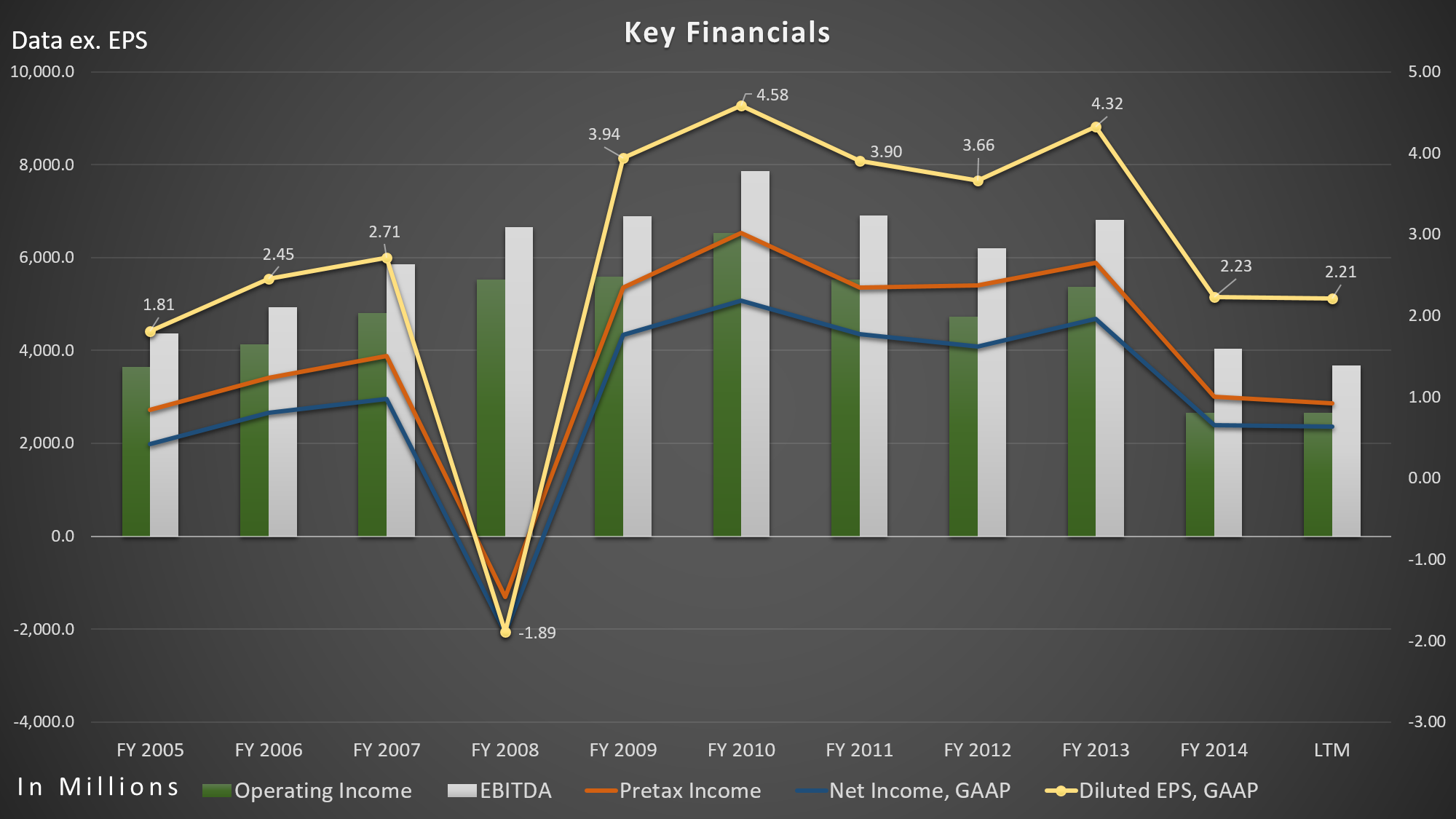

Eli Lilly’s market capitalization skyrocketed over the past five years by 122.76% to $90 billion, but their revenue, gross profit, net-income, operating income, as well as EBITDA, declined significantly. Over the past five years, its revenue decreased 14.61% from $23.08 billion to $19.70 billion (LTM), largely due to patent expirations. Gross profit and net-income declined 26.06% and 53.48%, respectively. Its operating income fell 59.18% over the past five years.

Eli Lilly – Revenue/Gross Profit

Eli Lilly – Key Financials

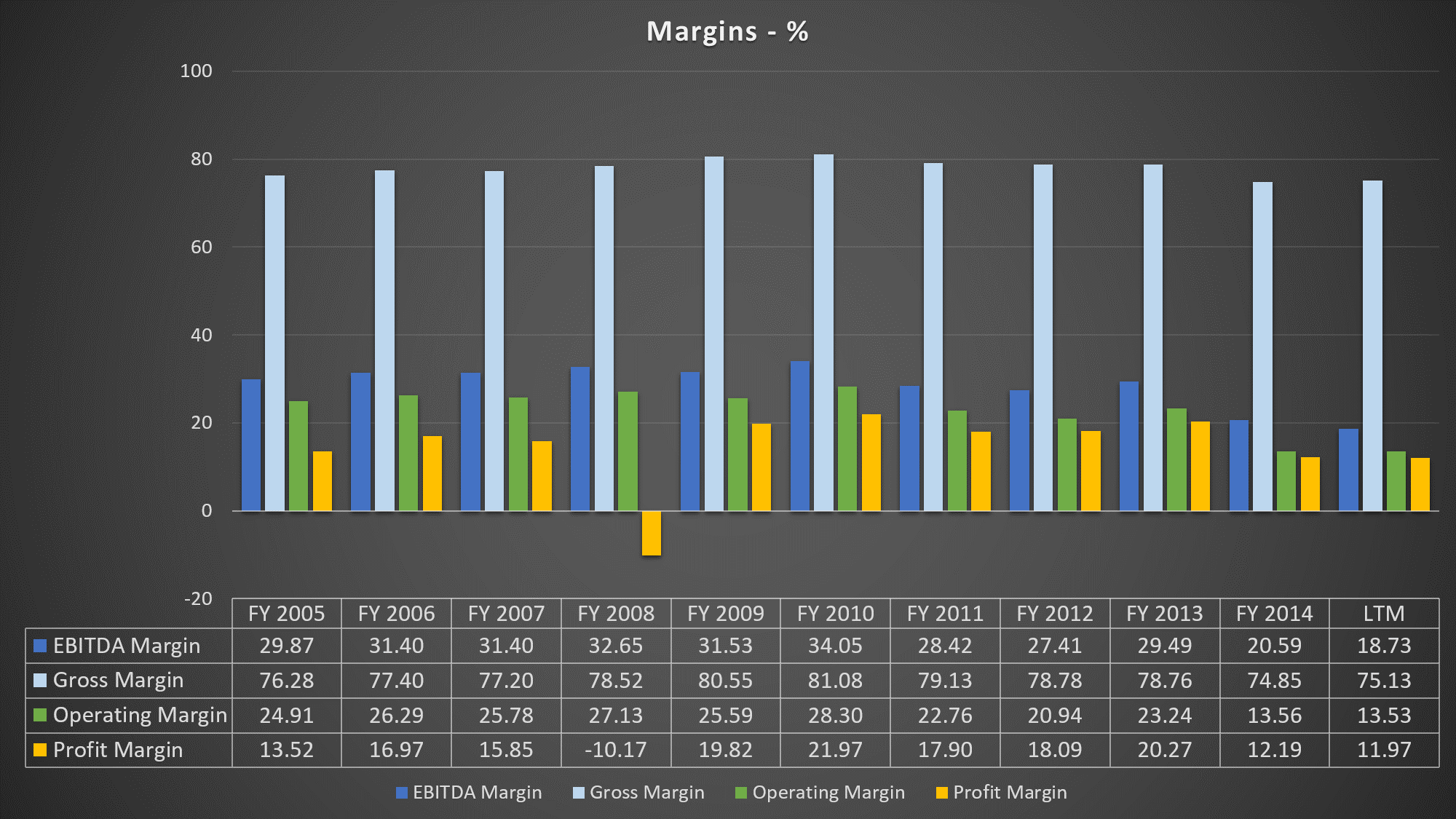

Its operating margin fell a halfway over the past five years from 28.30% to 13.53% (LTM). EBITDA margin, on the other hand, fell all the way to 18.73% (LTM) from 34.05%.

Eli Lilly – Key Margins

Meanwhile, shares of Eli Lilly gained 144.49% over the past five years. Its price-to-sales ratio too high compared to its history and to S&P 500. Its Price/Sales ratio currently stands at 4.6, vs. at 1.7 in 2010, while S&P 500 currently stays at 1.8 and industry average at 3.9. In addition to the falling revenue, gross profit, net-income, and EBITDA, its free cash flow fell significantly over the past five years by 72.24%, or fell 22.61% on a compounded annual basis.

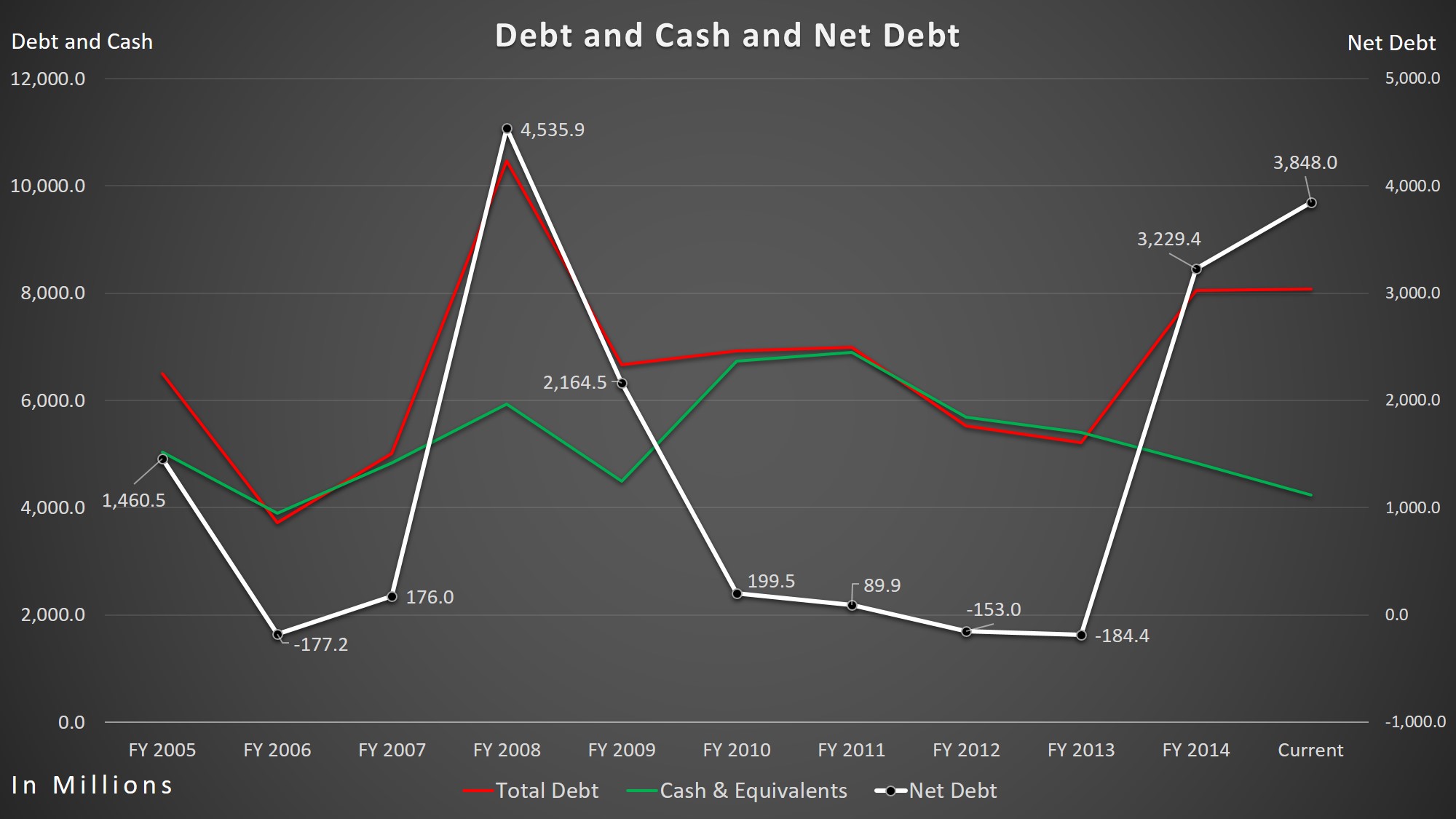

Not only did their cash flow fall, but their net-debt increased significantly. Its net-debt increased by a whopping 1789.87% over the past five years from $199.5 million to $3.85 billion. They now have almost twice as much of total debt than they do in cash and equivalents. I believe Eli Lilly is at a risk for poor future ratings by rating agencies, which will increase their borrowing costs.

Eli Lilly – Total Cash/Total Cash/Net-Debt

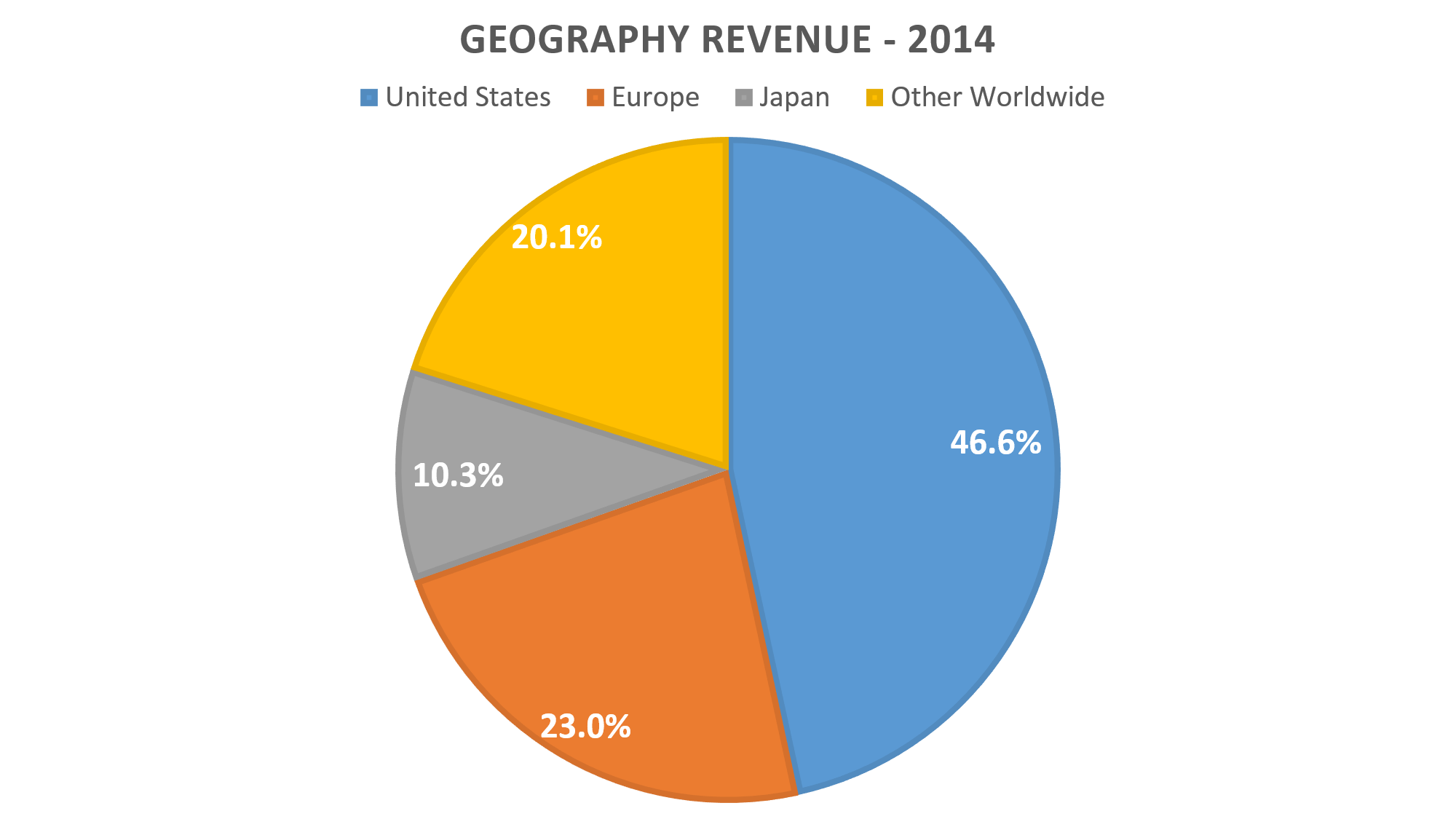

Strong U.S. dollar is an issue for Eli Lilly. Over the past five years, the dollar index increased 26.75%. Last quarter, its 49.2% of revenue came from foreign countries. Its revenue in the U.S. increased 14% to $2.54 billion, while revenue outside the U.S. decreased 9% to $2.42.

Eli Lilly – 2014 Geography Revenue

Eli Lilly’s dividend yield of 2.55% or 0.50 cents per share quarterly can be attractive, but it is undesirable. From 1995 through 2009 (expectation of 2003-2004), Eli Lilly raised its dividend. Payouts of $0.26 quarterly in 2000 almost doubled to $0.49 in 2009. Then, the company kept its dividend payment unchanged in 2010, the same year when its net-income, EBITDA and earnings per share (EPS) reached an all-time high. About four years later (December 2014), Eli Lilly increased the dividend to $0.50 quarterly. I still don’t see a reason to buy shares of Eli Lilly. The frozen divided before the recent increase was a signal that the management did not see earnings growing. With expected patent expiration of Cymbalta, their top selling drug in 2010, it is no wonder Eli Lilly’s key financials declined and dividends stayed the same. Cymbalta sales were $5.1 billion in 2013, the year its patent expired. In 2014, its sales shrank all the way down to $1.6 billion. Loss of exclusivity for Evista in March 2014 immensely reduced Eli Lilly’s revenue rapidly. Sales decreased to $420 million in 2014, followed by $1.1 billion in 2013. Pharmaceuticals industry continues to lose exclusivities, including Eli Lilly.

In December 2015, Eli Lilly will lose a patent exclusivity for antipsychotic drug Zyprexa in Japan and for lung cancer drug Alimta in European countries and Japan. Both of the drugs combined accounted for revenue of $866.4 million in the third-quarter, or 17.5% of the total revenue. They will also lose a patent protection for the erectile dysfunction drug Cialis in 2017, which accounted for $2.29 billion of sales in 2014, or 11.68% of the total revenue.

Besides the pressure from patent expirations, there is also regulatory pressures on drug pricing. According to second-quarter 10Q filing, Eli Lilly believes “State and federal health care proposals, including price controls, continue to be debated, and if implemented could negatively affect future consolidated results of operations.” During the third-quarter earnings call, CEO of Eli Lilly, John C. Lechleiter, said that price increases reflects many of medicines going generic and “deep discounts” government mandates for large purchasers.

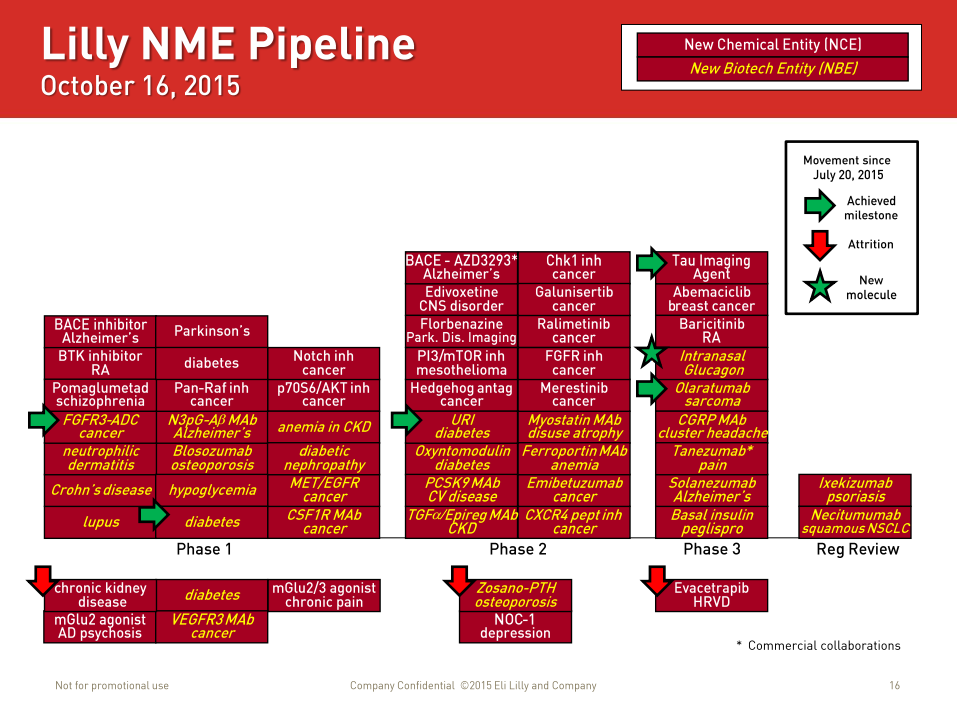

As of October 16, Eli Lilly had two drugs under regulatory review, nine drugs in Phase 3 testing, and 18 drugs in Phase 2 testing. Since the end of July, the drug maker terminated the development of few drugs, including evacetrapib in Phase 3, two drugs in Phase 2, and five in Phase 1. Out of total eight drug termination, only five drugs moved to the next stage of testing. I view the recent termination of evacetrapib as a major setback.

Compared to its peers, LLY’s Price-to-Earnings ratio is too high. Its P/E ratio (on GAAP basis) stands at 38.22 while industry average stands at 17.7. Four of its main peers, Pfizer (PFE), Johnson & Johnson (JNJ), Merck (MRK), and Sanofi (SNY) P/E ratio stands at 24.08, 19.63, 14.41, and 22.38, respectively.

Negative trends, tighter regulations, increasing competition and slowing growth makes Eli Lilly’s current valuation unjustified. I believe it will reach an average P/E ratio of its four main competitors, at 20.12, in the next three years. I expect EPS (GAAP) to contract. With current EPS of $2.21 (LTM, GAAP) and P/E ratio of 20.12, share price would be worth $44.46, down 47.37% from current share-price of $84.47. As EPS contracts, the share price of Eli Lilly will be much further down from $44.46 in the next three years.

Disclosure: I’m not currently short on the stock, LLY, at this time (October 21, 2015).

Note: All information I used here such as revenue, margins, EBITDA, etc are found from Eli Lilly and Company’s official investor relations site, Bloomberg terminal and morningstar. The pictures you see here are my own, except “Eli Lilly Pipeline – Third Quarter Earnings Presentation – Page 16”

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.