WHAT A YEAR! Market sell-off. Complete reverse afterwards. Full of surprises, from Brexit to Trump (not for me since I predicted them).

During the global markets crash in August of 2015, I completely lost all the money I made that year plus some more in forex. Witnessing markets free fall – faster than Luke skydiving 25,000 feet without parachute – for the first time ever crushed my account to death. (For the record, I wasn’t trading in 2008 and had absolutely no idea what was unfolding that time).

Thinking euro will go to the parity level by the end of 2015, most of my positions were crowded in shorting EUR (The Big Short). Just when I thought euro would follow the markets, it acted as a safe-haven.

Lessons learned the hard way:

Always keep enough cash for emergency and/or new opportunities (could not make new trades)

Do not keep most things in one place (EUR short)

Do not let the perceptions – media, traders, experts, you name it – fool you (“Euro is not a safe-haven asset”)

Taking all these lessons, I completely changed my strategy and will continue to tweak it to adapt to the current conditions. After taking a break from trading in September (2015), I opened a new forex account.

Started off strongly, with high standard deviations, but enough for me to sit through that. High-risk/High-reward. As I continued tweaking my strategy, I reduced the swings in the P/L.

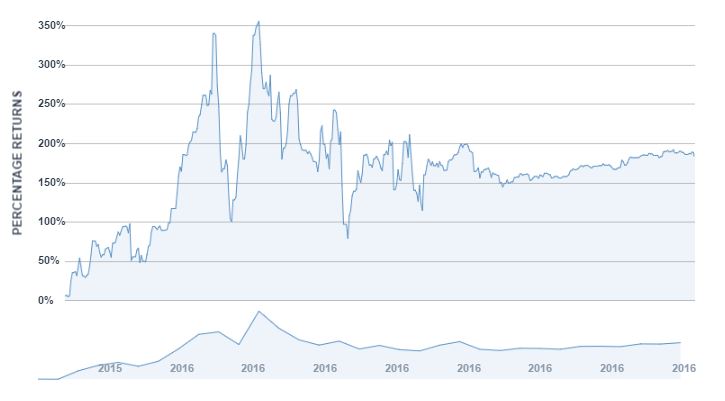

Figure 1: Forex Portfolio % Returns Since Inception (09/29/2015)

Starting in August 18 of this year (2016), my returns have been very stable, trending upwards (see Figure 1). It went from 144.49% return to 184.42% as of the last trading day in 2016. Last August, I made a significant chance to my strategy which led to stable returns trending upwards. I continue to tweak my strategy little by little until significant change is needed. Repeat.

Since inception (09/29/2015), I have returned 184.42%. In the second half of this year, I deposited more money into the account. In turn, the % returns you see in the pictures above and below, has a huge difference in nominal amounts.

Figure 2: Forex Portfolio Performance Since Inception

In 2015, I returned 117.48%. This year, I have returned 32.82%. Since the inception, percentage of profitable trades are 50.70%, with the average gain per trade 3.82 larger than the amount of average loss per trade.

Sharpe ratio is 1.13 (not good yet), with average monthly return of 11.01% and 33.79% standard deviation of monthly return. Compounded monthly rate of return is 7.22%.

I predicted Brexit and profited bigly off it. 30.77% of the profit came from pair GBP/USD. Thanks Brexit. How did I predict Brexit?

Predicting Brexit – 6 tweetsFigure 3: Top 3 FX pair P/L as a % of the total P/L

Largest loss was 5.21%, from pair AUD/USD. I don’t know what to blame except myself.

As to predicting Trump’s win, the profit was a fraction of Brexit profit, via other pairs than Mexican peso currency. The day after the election, the peso suffered its largest one-day drop since the Tequila Crisis of the 1990s. Too bad I did not have access to peso pair at the time. How did I predict Trump win? Tweet 1, 2.

If you invested $1,000 in me at the inception, that money would have been worth $2,844.23 today.

You can still invest in me. Minimum investment is $1,000. Contact me for more details.

12….11…10…9….IGNITION SEQUENCE START….6….5….4….3….2….1….0….ALL ENGINES RUNNING….LIFTOFF….WE HAVE A LIFTOFF!

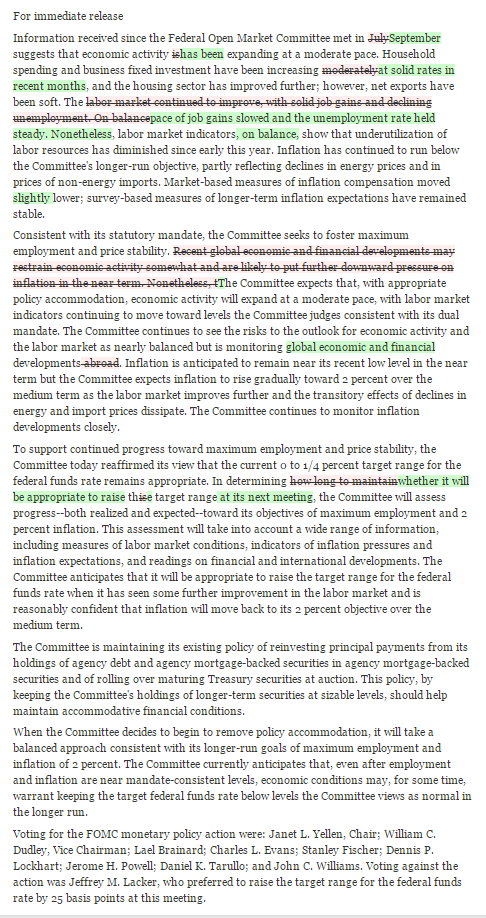

The Fed finally raised rates after nearly a decade. On December 16, the Fed decided to raise rates – for the first time since June 2006 – by 0.25%, or 25 basis points. It was widely expected by the markets and I only expected 10bps hike. Well, I was wrong on that.

The Federal Open Market Committee (FOMC) unanimously voted to set the new target range for the federal funds rate at 0.25% to 0.50%, up from 0% to 0.25%. In the statement, the policy makers judged the economy “has been expanding at a moderate pace.” Labor market had shown “further improvement.” Inflation, on the other hand, has continued to “run below Committee’s 2 percent longer-run objective” mainly due to low energy prices.

Remember when the Fed left rates unchanged in September? It was mainly due to low inflation. What’s the difference this time?

In September, the Fed clearly stated “…survey—based measures of longer-term inflation expectations have remained stable.”

Now, the Fed clearly states “…some survey-based measures of longer-term inflation expectations have edged down.”

So…umm…why did they raise rates this time?

Here is a statement comparison from October to December:

Fed Statement Comparison – Oct. to Dec. Source: WSJ

On the pace of rate hikes looking forward, the FOMC says:

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

They clearly stated one of the things they look for, which is inflation expectations. But, they also did state that “inflation expectations have edged down.”

It seems to me that the Fed did not decide to raise rates. The markets forced them. Fed Funds Futures predicted about 80% chance of a rate-hike this month. If the Fed did not raise rates, they would have lost their credibility.

I believe the Fed will have to “land” (lower back) rates this year, for the following reasons:

Growing Monetary Policy Divergence

On December 3, European Central Bank (ECB) stepped up its stimulus efforts. The central bank decided to lower deposit rates by 0.10% to -0.30%. The purpose of lower deposit rates is to charge banks more to store excess reserves, which stimulates lending. In other words, free money for the people so they can spend more and save less.

ECB also decided to extend Quantitative Easing (QE) program. They will continue to buy 60 billion euros ($65 billion) worth of government bonds and other assets, but until March 2017, six months longer than previously planned, taking the total size to 1.5 trillion euros ($1.6 trillion), from the previous $1.2 trillion euros package size. During the press conference, ECB President Mario Draghi said the asset eligibility would be broadened to include regional and local debt and signaled QE program could be extended further if necessary.

ECB might be running out of ammunition. ECB extending its purchases to regional and local debt raises doubts about its program.

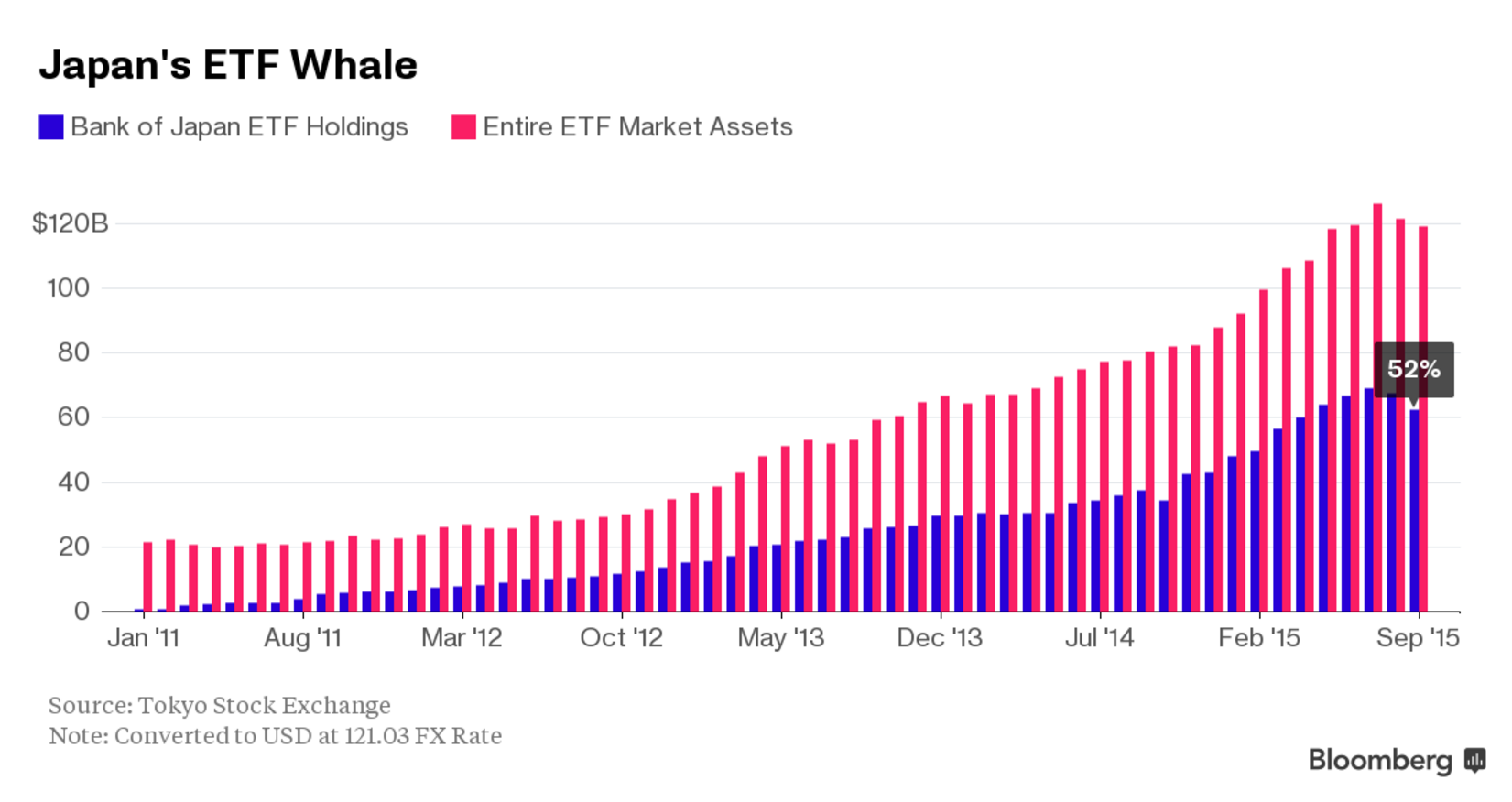

Not only ECB is going the opposite direction of the Fed. Three weeks ago, Bank of Japan (BoJ) announced a fresh round of new stimulus. The move was hardly significant, but it is still a new round of stimulus. The central bank decided to buy more exchange-traded fund (ETF), extend the maturity of bonds it owns to around 7-12 years from previously planned 7-10 years, and increase purchases of risky assets.

The move by BoJ exposes the weakness of its past actions. It suggests the bank is also out of ammunition. Already owning 52% or more of the Japan’s ETF market and having a GDP-to-Debt ratio around 245%, it is only a matter of time before Japan’s market crashes. Cracks are already beginning to be shown. I expect the market crash anytime before the end of 2019.

So, what are the side-effects of these growing divergence?

For example, the impact of a US dollar appreciation resulting from a tightening in US monetary policy and the impact of a depreciation in other currencies resulting from easing in its monetary policies. Together, these price changes will shift global demand – away from goods and services produced here in the U.S. and toward those produced abroad. In others words, US goods and services become more expensive abroad, leading to substitution by goods and services in other countries. Thus, it will hurt the sales and profits of U.S. multinationals. To sum up everything that is said in this paragraph, higher U.S. rates relative to rates around the global harms U.S. competitiveness.

Emerging Markets

Emerging markets were trouble last year. It is about to get worse.

International Monetary Fund (IMF) decided to include China’s currency, renminbi (RMB) or Yuan, to its Special Drawing Rights (SDR) basket, a basket of reserve currencies. Effective October 1, 2016, the Chinese currency is determined to be “freely usable” and will be included as a fifth currency, along with the U.S. dollar, euro, Japanese yen, and pound sterling, in the SDR basket.

“Freely useable” – not so well defined, is it?

Chinese government or should I say People’s Bank Of China (PBOC), cannot keep its hands off the currency (yuan). It does not want to let market forces take control. They think they can do whatever they want. As time goes on, it is highly unlikely. As market forces take more and more control of its exchange-rate, it will be pushed down, due to weak economic fundamentals and weak outlook.

China, no need to put a wall to keep market forces out. Let the market forces determine the value of your currency. It is only a matter of time before they break down the wall.

In August, China changed the way they value their currency. PBOC, China’s central bank, said it will decide the yuan midpoint rate based on the previous day’s close. In daily trading, the yuan is allowed to move 2% above or below the midpoint rate, which is called the daily fixing. In the past, the central bank used to ignore the daily moves and do whatever they want. Their decision to make the midpoint more market-oriented is a step forward, but they still have a long way to go.

China saw a significant outflows last year. According to Institute of International Finance (IFF), an authoritative tracker of emerging market capital flows, China will post record capital outflows in 2015 of more than $500 billion. The world’s second largest economy is likely to see $150 billion in capital outflow in the fourth quarter of 2015, following the third quarter’s record $225 billion.

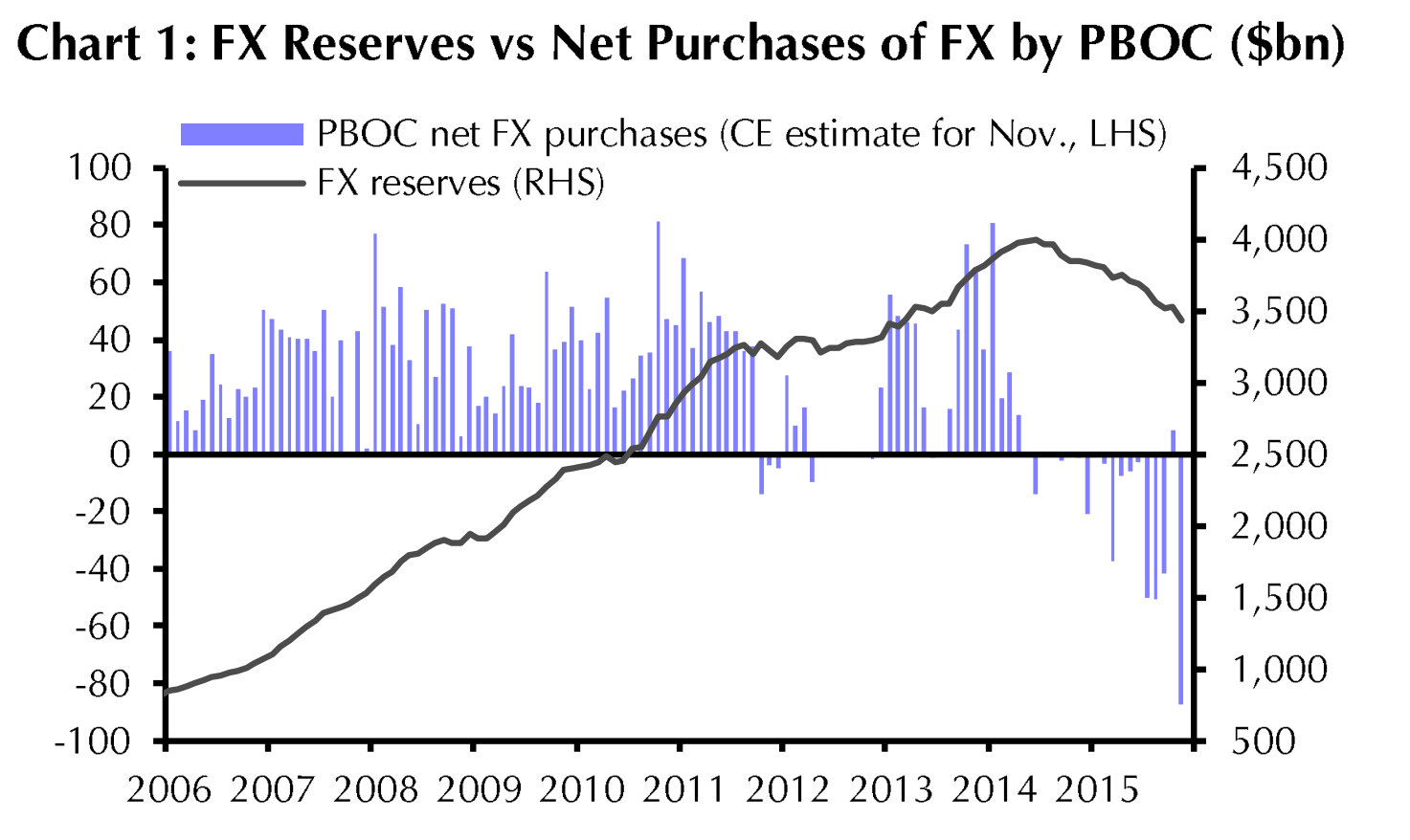

Ever since the devaluation in August, PBOC has intervened to prop yuan up. The cost of such intervention is getting expensive. The central bank must spend real money during the trading day to guide the yuan to the level the communists want. Where do they get the cash they need? FX reserves.

China’s foreign-exchange reserves, the world’s largest, declined from a peak of nearly $4 trillion in June 2014 to just below $3.5 trillion now, mainly due to PBOC’s selling of dollars to support yuan. In November, China’s FX (forex) reserves fell $87.2 billion to $3.44 trillion, the lowest since February 2013 and largest since a record monthly drop of $93.9 billion in August. It indicates a pick-up in capital outflows. This justifies increased expectations for yuan depreciation. Since the Fed raised rates last month, I would not be surprised if the capital flight flies higher, leading to a weaker yuan.

Depreciation of its currency translates into more problems for “outsiders,” including emerging markets (EM). EMs, particularly commodities-linked countries got hit hard last year as China slowed down and commodity prices slumped. EMs will continue to do so this year, 2016.

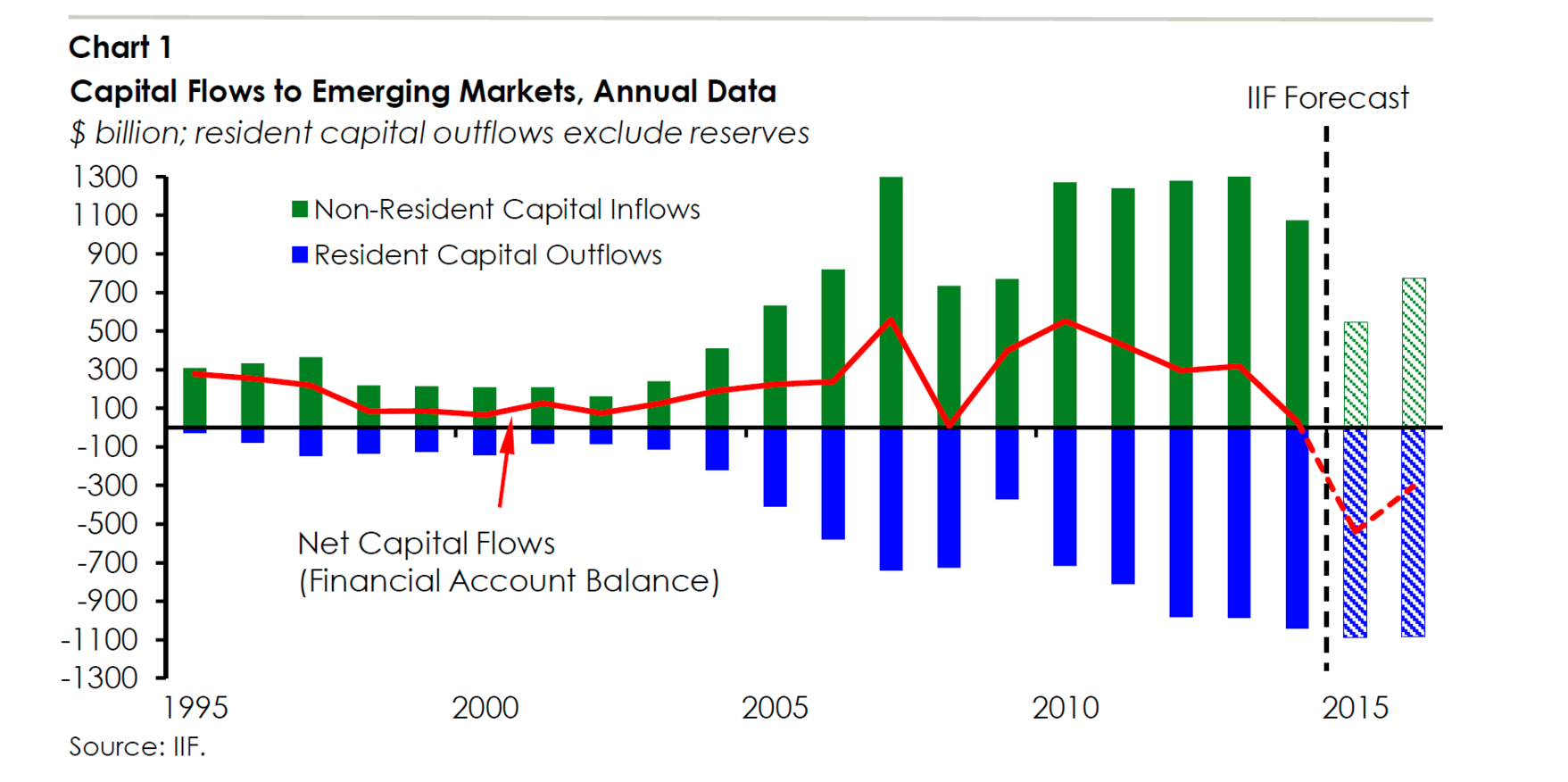

The anticipation of tightening in the U.S. and straightening dollar put a lot of pressure on EM. EM have seen a lot of significant capital outflows because they carry a lot of dollar denominated debt. According to the October report from IFF, net capital flows to EM was negative last year for the first time in 27 years (1988). Investors are estimated to pull $540 billion from developing markets in 2015. Foreign inflows will fall to $548 billion, about half of 2014 level and lower than levels recorded during the financial crisis in 2008. Foreign investor inflows probably fell to about 2% of GDP in emerging markets last year, down from a record of about 8% in 2007.

Capital Flows to Emerging Markets, Annual Data Source: IFF, taken from Bloomberg

Also contributing to EM outflows are portfolio flows, “the signs are that outflows are coming from institutional investors as well as retail,” said Charles Collyns, IIF chief economist. Investors in equities and bonds are estimated to have withdrawn $40 billion in the third quarter, the worst quarterly figure since the fourth quarter of 2008.

A weaker yuan will make it harder for its main trading partners, emerging markets and Japan, to be competitive. This will lead to central banks of EM to further weaken their currencies. Japan will have no choice but to keep extending their QE program. And to Europe. And to the U.S. DOMINO EFFECT

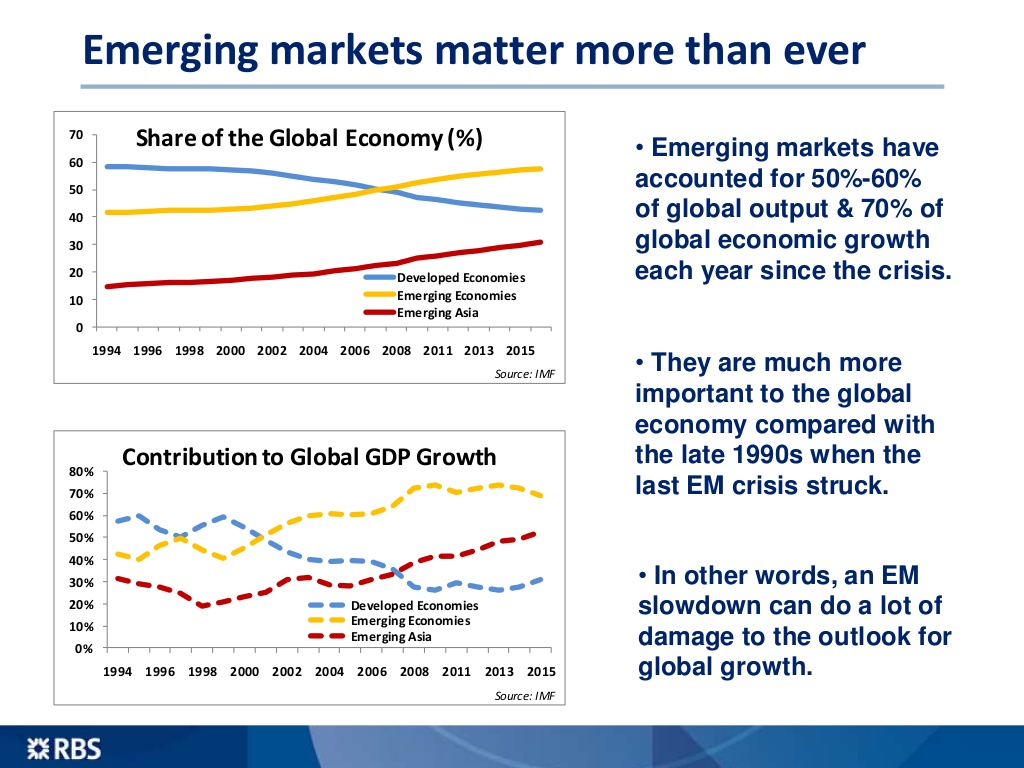

Why are EMs so important? According to RBS Economics, EMs have accounted for 50%-60 of global output and 70% of global economic growth each year since the 2008 crisis.

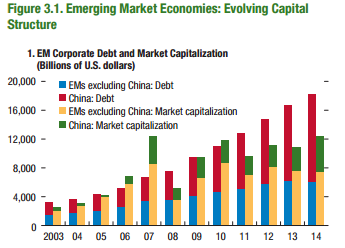

Some EM investors, if not all, will flee as U.S. rates rise, compounding the economic pain there. Corporate debt in EM economies increased significantly over the past decade. According to IMF’s Global Financial Stability report, the corporate debt of non-financial firms across major EM economies increased from about $4 trillion in 2004 to well over $18 trillion in 2014.

When you add China’s debt with EM, the total debt is higher than the market capitalization. The average EM corporate debt-to-GDP ratio has also grown by 26% the same period.

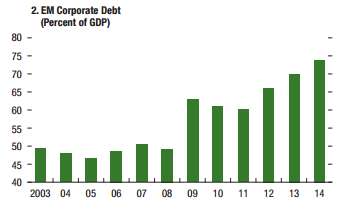

EM Corporate Debt (percent of GDP) – Page 84

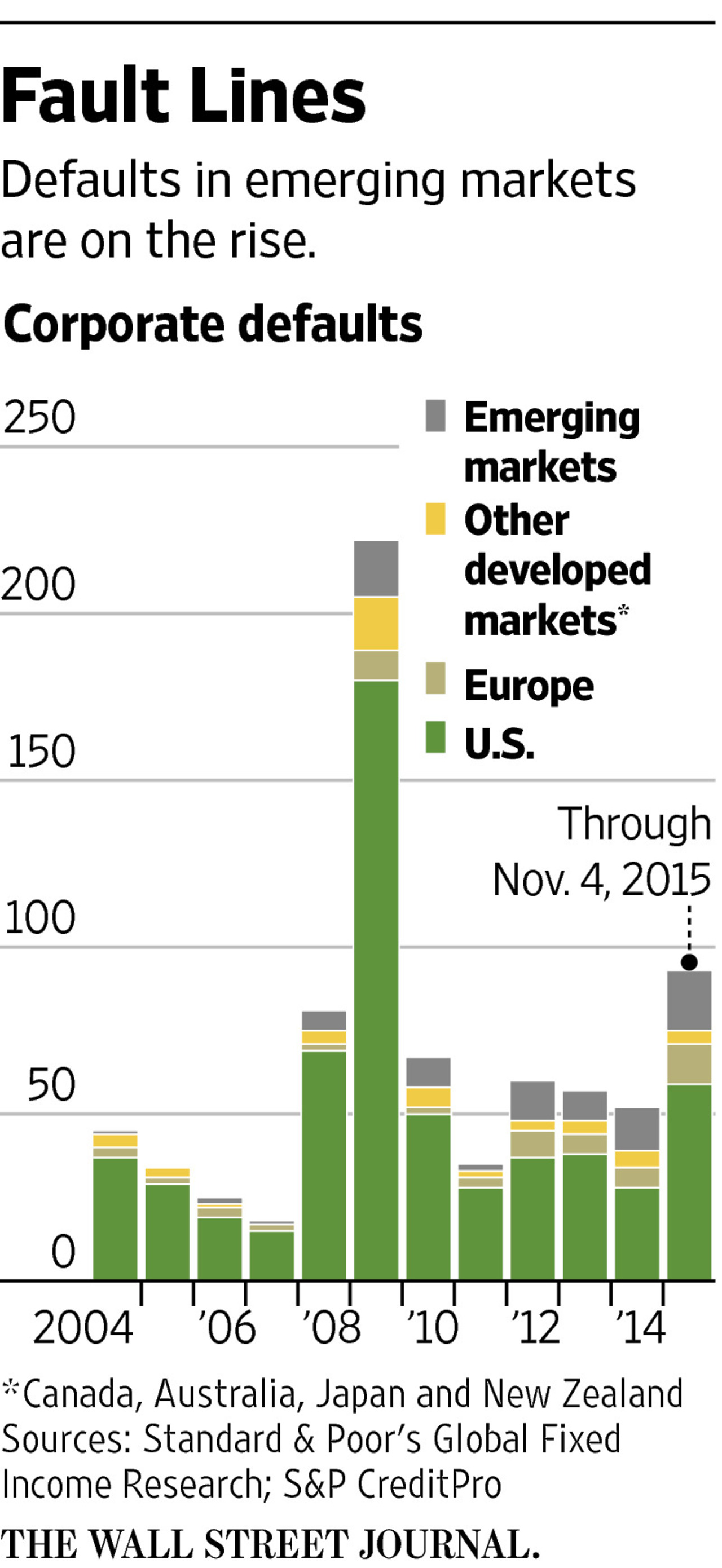

The speed in the build-up of debt is distressing. According to Standard & Poor’s, corporate defaults in EM last year have hit their highest level since 2009, and are up 40% year-over-year (Y/Y).

According to IFF (article by WSJ), “companies and countries in EMs are due to repay almost $600 billion of debt maturing this year….of which $85 is dollar-denominated. Almost $300 billion of nonfinancial corporate debt will need to be refinanced this year.”

I would not be surprised if EM corporate debt meltdown triggers sovereign defaults. As yuan weakens, Japan will be forced to devalue their currency by introducing me QE which leaves EMs with no choice. EMs will be forced to devalue their currency. Devaluations in EM currencies will make it much harder (it already is) for EM corporate borrowers to service their debt denominated in foreign currencies, due to decline in their income streams. Deterioration of income leads to a capital flight, pushing down the value of the currency even more, which leads to much more capital flight.

“Firms that have borrowed the most stand to endure the sharpest rise in their debt-service costs once interest rates begin to rise in some advanced economies. Furthermore, local currency depreciations associated with rising policy rates in the advanced economies would make it increasingly difficult for emerging market firms to service their foreign currency-denominated debts if they are not hedged adequately. At the same time, lower commodity prices reduce the natural hedge of firms involved in this business.”

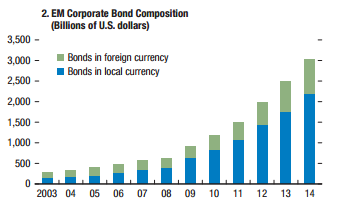

According to its Global Financial Stability report, EM companies have an estimated $3 trillion in “overborrowing” loans in the last decade, reflecting a quadrupling of private sector debt between 2004 and 2014.

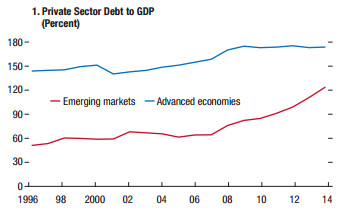

EM Corporate Bond Composition (Billions of U.S. dollars) – Page 86Private Sector Debt to GDP (Percent – Page 11

Rising US rates and a strengthening dollar will make things much worse for EMs. Jose Vinals, financial counsellor and director of the IMF’s Monetary and Capital Markets Department, said in his October article, “Higher leverage of the private sector and greater exposure to global financial conditions have left firms more susceptible to economic downturns, and emerging markets to capital outflows and deteriorating credit quality.”

I believe currency war will only hit “F5” this year and corporate defaults will increase, leading to the early stage of sovereigns’ defaults. I would not be surprised if some companies gets a loan denominated in euros just to pay off the debt denominated in U.S dollars. That’s likely to make things worse.

Those are some of the risks I see that will force the Fed to lower back the rates. I will address more risks, including lack of liquidity, junk bonds, inventory, etc, in my next article. Thank you.

EXTRA: Market reactions,

EUR/USD:

EUR/USD – Hourly Chart

USD/JPY:

USD/JPY – Hourly

10-Year Treasury Index:

10-Year Treasury Index ( “TNX” on thinkorswim platform) – Hourly

2-Year U.S. Treasury Note Futures:

2-Year U.S. Treasury Note Futures ( “/ZT” on thinkorswim platform) – Hourly

On October 22 (Thursday), European Central Bank (ECB) left rates unchanged, with interests on the main refinancing operations, marginal lending, and deposit rate at 0.05%, 0.30% and -0.20, respectively. But the press conference gave an interesting hint. Mario Draghi, the President of ECB, was most dovish as he could be, “work and assess” (unlike “wait and see” before).

The central bank is preparing to adjust “size, composition and duration” of its Quantitative Easing (QE) program at its December meeting, “the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting”, Draghi said during the press conference. They are already delivering a massive stimulus to the euro area, following decisions taken between June 2014 and March 2015, to cut rates and introduce QE program. In September 2014, ECB cut its interest rate, or deposit rate to -0.20%, a record low. Its 1.1 trillion euros QE program got under way in March with purchases of 60 billion euros a month until at least September 2016.

When ECB cut deposit rate to record low in September 2014, Mr. Draghi blocked the entry to additional cuts, “we are at the lower bound, where technical adjustment are not going to be possible any longer.” (September 2014 press conference). Since then, growth hasn’t improved much and other central banks, such as Sweden and Switzerland, cut their interest rates into much lower territory. Now, another deposit rate-cut is back, “Further lowering of the deposit facility rate was indeed discussed.” Mr. Draghi said during the press conference.

The outlook for growth and inflation remains weak. Mr. Draghi – famous for his “whatever it takes” line – expressed “downside risks” to both economic growth and inflation, mainly from China and emerging markets.

Given the extent to which the central bank provided substantial amount of stimulus, the growth in the euro area has been disappointing. The euro area fell into deflation territory in September after a few months of low inflation. In September, annual inflation fell to 0.1% from 0.1% and 0.2% in August and July, respectively. Its biggest threat to the inflation is energy, which fell 8.9% in September, down from 7.2% and 5.6% in August and July, respectively.

As the ECB left the door open for more QE, Euro took a dive. Euro took a deeper dive when Mr. Draghi mentioned that deposit rate-cut was discussed. Deposit rate cut will also weaken the euro if implemented. After the press conference, the exchange rate is already pricing in a rate-cut. Mentions of deposit rate-cut and extra QE sent European markets higher and government bond yields fell across the board. The Euro Stoxx 50 index climbed 2.6%, as probability of more easy money increased. Swiss 10-year yield fell to fresh record low of -0.3% after the ECB press conference. 2-year Italian and Spanish yields went negative for the first time. 2-year German yield hit a record low of -0.32.

Regarding the exchange rate (EUR/USD), I expect it to hit a parity level by mid-February 2016.

As I stated in the previous posts, I expect more quantitative easing by ECB (and Bank of Japan also). I’m expecting ECB to increase its QE program to 85 billion euros a month and extend it until March 2017. When ECB decides to increase and extend the scope of its QE, I also expect deposit rate-cut of 10 basis points.

ECB will be meeting on December 3 when its quarterly forecasts for inflation and economic growth will be released. The only conflict with this meeting is that U.S. Federal Reserve policy makers meets two weeks later. ECB might hold off until the decision of the Fed, but the possibility of that is low.

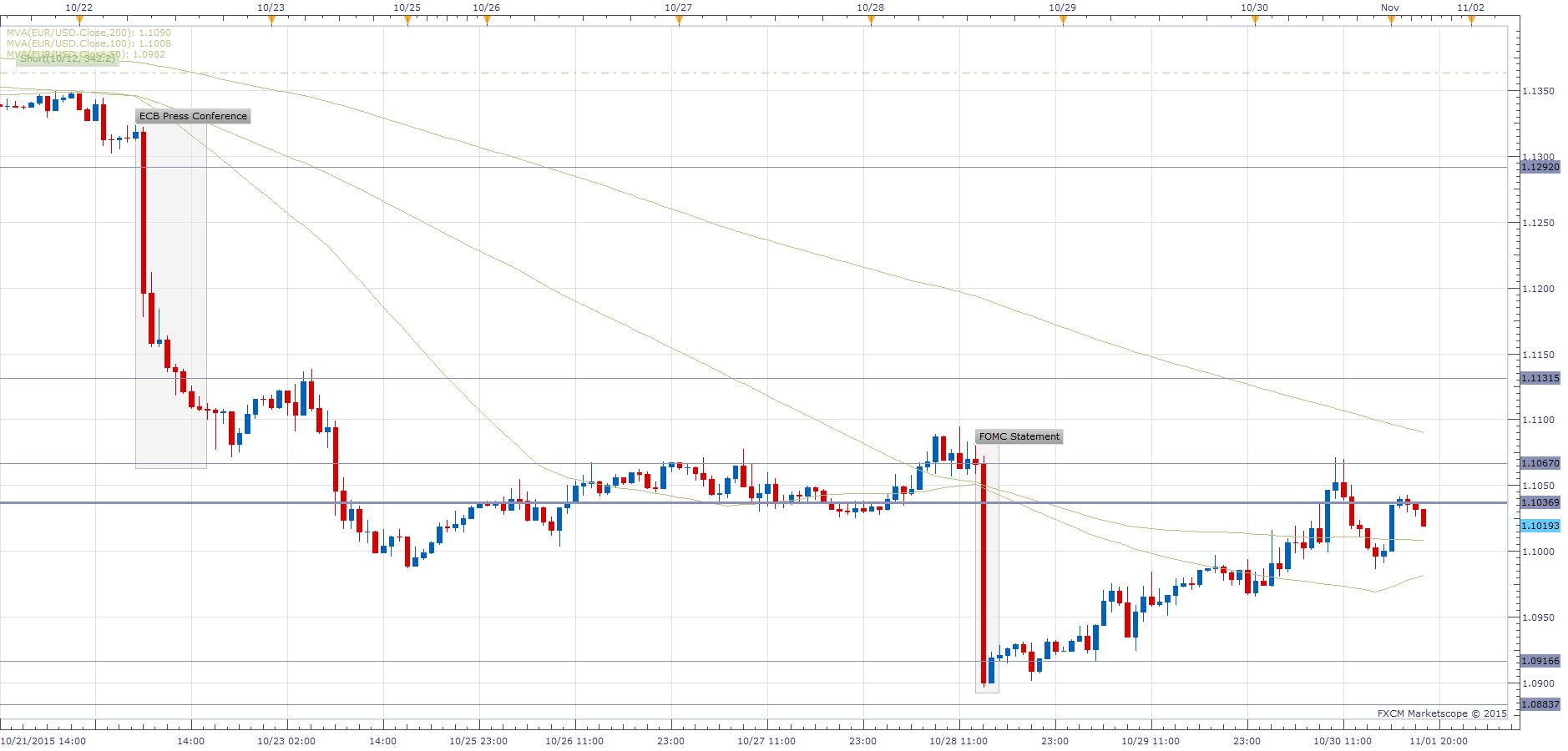

EUR/USD Reaction:

EUR/USD – Hourly Chart

U.S. Federal Reserve:

On October 28 (Wednesday), the Federal Reserve left rates unchanged. The bank was hawkish overall. It signaled that rate-hike is still on the table at its December meeting and dropped previous warnings about the events abroad that poses risks to the U.S. economy.

It does not make sense to drop “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” (September statement) I’m sure the events abroad has its risks (spillover effect) to the U.S. economy and the Fed will keep an eye on them.

In its statement, it said the U.S. economy was expanding at a “moderate pace” as business capital investments and consumer spending rose at “solid rates”, but removed the following “…labor market continued to improve…” (September statement). The pace of job growth slowed, following weak jobs report in the past several months.

Let’s take a look at the comparison of the Fed statement from September to October, shall we?

The Fed badly wants to raise rates this year, but conditions here and abroad does not support its mission. Next Federal Open Market Committee (FOMC) meeting takes place on December 15-16. By then, we will get important economic indicators including jobs report, Gross Domestic Product (GDP), retail spending and Consumer Price Index (CPI). If we don’t see any strong rebound, rate-hike is definitely off the table, including my prediction of 0.10% rate-hike for next month.

The report caused investors to increase the possibility of a rate increase in December. December rate-hike odds rose to almost 50% after the FOMC statement.

Greenback (US Dollar) Reaction:

U.S. Dollar ( “/DX” on thinkorswim platform) – Hourly Chart

Reserve Bank of New Zealand:

On October 28 (Wednesday), Reserve Bank of New Zealand (RBNZ) left rates unchanged at 2.75% after three consecutive rate-cuts since June. The central bank’s Governor Graeme Wheeler said that at present “it is appropriate to watch and wait.” “The prospects for slower growth in China and East Asia” remains a concern.

Housing market continues to pose financial stability risk. House price inflation is way higher. Median house prices are about nine times the average income. Short supply caused the house prices to increase significantly. “While residential building is accelerating, it will take some time to correct the supply shortfall.” RBNZ said in a statement. Auckland median home prices rose about 25.4% from September 2014 to September 2015, “House price inflation in Auckland remains strong, posing a financial stability risk.”

Further reduction in the Official Cash Rate (OCR) “seems likely” to ensure future CPI inflation settles near the middle of the target range (1 to 3%).

Although RBNZ left rates unchanged, Kiwi (NZD) fell because the central bank sent a dovish tone, “However, the exchange rate has been moving higher since September, which could, if sustained, dampen tradables sector activity and medium-term inflation. This would require a lower interest rate path than would otherwise be the case.” It’s a strong signal that RBNZ will cut rates to 2.5% if Kiwi continues to strengthening. I will be shorting Kiwi every time it strengthens.

“The sharp fall in dairy prices since early 2014 continues to weigh on domestic farm incomes…However, it is too early to say whether these recent improvements will be sustained.” RBNZ said in the statement. Low dairy prices caused RBNZ to cut rates. New Zealand exports of whole milk powder fell 58% in the first nine months of this year, compared with the same period in 2014. But, there’s a good news.

Recent Chinese announcement that it would abolish its one-child policy might just help increase dairy prices, as demand will increase. How? New Zealand is a major dairy exporter to China. Its milk powder and formula industry is likely to benefit from a baby boomlet in China.

BoJ expects to hit its 2% inflation target in late 2016 or early 2017 vs. previous projection of mid-2016. Again and Again. This is the second time BoJ changed its target data. The last revision before this week was in April. It also lowered its growth projections for the current year by 0.5% to 1.2%.

They also lowered projections for Core-CPI, which excludes fresh food but includes energy. They lowered their forecasts for this fiscal year to 0.1%, down from a previous estimate of 0.7%. For the next fiscal year, they expect 1.4%, down from a previous estimate of 1.9%. Just like other central banks, BoJ acknowledged that falling energy prices were hitting them hard.

Low inflation, no economic growth, revisions, revisions, and revisions. Nothing is recovering in Japan.

Haruhiko Kuroda, the governor of BoJ, embarked on aggressive monetary easing in early 2013. So far he hasn’t had much success.

In the second quarter (April-June), Japan’s economy shrank at an annualized 1.2%. Housing spending declined 0.4% in September from 2.8% in August. Core-CPI declined for two straight months, falling 0.1% year-over-year both in September and August. Annual exports only rose 0.6% in September, slowest growth since August 2014, following 3.1% gain in August.

Exports are part of the calculation for Gross Domestic Product (GDP). Another decline in GDP would put Japan into recession, which could force BoJ to ease its monetary policy again. Another recession would be its fourth since the 2008 financial crisis and the second since Shinzo Abe (Abenomics), the Prime Minister of Japan, came to power in December 2012.

Its exports to China, Japan’s second-biggest market after the U.S., fell 3.5% in September. The third-quarter (July-September) GDP report will be released on November 16.

April 2014 sales tax (sales tax increased from 5% to 8%) increase only made things worse in Japan. It failed to boost inflation and weakened consumer sentiment.

In April 2013, BoJ expanded its QQE (or QE), buying financial assets worth 60-70 trillion yen a year, including Exchange Traded Funds (ETF).

QQE stands for Quantitative and Qualitative Easing. Qualitative easing targets certain assets to drive up their prices and drive down their yield, such as ETF. Quantitative Easing targets to drive down interest rates. Possibility of negative interest rates has been shot down by BoJ. But, why trust BoJ for their word? Actions speak louder than words.

In October 2014, BoJ increased the QQE to an annual purchases of 80 trillion yen. When is the next expansion? December?

Did you know that the BoJ owns 52% of Japan’s ETF market?

For over a decade, BoJ’s aggressive monetary easing through asset purchases did not help Japan’s economy. Since 2001, the central bank operated 9 QEs and is currently operating its current 10th QE (or QQE). The extensions of its QE are beginning to become routine or the “new normal.”

Growth and prices are slowing in China, with no inflation in United Kingdom, Euro-zone, and the U.S. The chances that Japan will crawl out of deflation are very slim.

USD/JPY Reaction:

USD/JPY – Hourly Chart

US Market Reactions (ECB and FOMC):

S&P 500 (“SPX”) – Hourly Chart

Next week, both Reserve Bank of Australia (RBA) and Bank of England (BoE) will meet. Will be very interesting to watch.