It’s all magic. Anyone can become a millionaire without special anything. All you need is money, and … abracadabra … magic works itself. That magic is compounding, like a snowball rolling down the hill.

Albert Einstein – Compound Interest quote (not proven he actually said it)

As Einstein once said, “the most powerful force in the universe is compound interest.” Well actually, nobody can confirm the quote’s true author. It’s just credit to Einstein himself to give the quote more weight. More weight as in the snowball rolling down the hill. More weight as in your investment account balance increasing.

Past S&P 500 Returns

Over the past 40 years (1978 to 2017), S&P 500 has had an inflation-adjusted annualized return rate of 8.11%, after having dividends reinvested.

After dividends and compound interest, $1,000 investment in 1978 would be $22,661*.

Over the past 30 years (1988 to 2017), $1,000 investment would be $9,595*.

Over the past 20 years (1998 to 2017), $1,000 investment would be $2,623*.

Over the past 10 years (2008 to 2017), $1,000 investment would be $2,054*.

* Note the investment values above are before any brokerage fees and taxes.

That just includes the initial investment. It doesn’t include periodic investments. Let’s include periodic investments as an example.

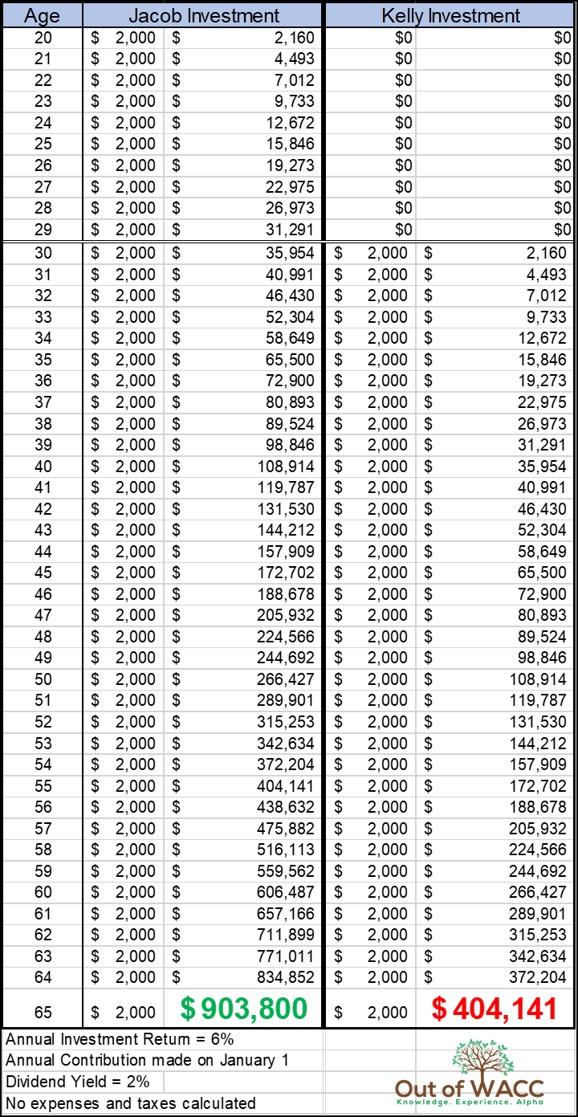

Time Is Power

Below you will see two people, Jacob and Kelly, making a periodic investment until they retire at age 65. The only difference is that Jacob starts investing at age 20. Kelly starts out late, at age 30.

Their investment will yield inflation-adjusted 5% annual return, and 2% dividend yield which automatically gets reinvested.

Jacob and Kelly, Investments

Jacob started out earlier and invested $20,000 more than Kelly. However, he came out way ahead of her by a whopping $499,659. Time is money. The power of time and compound is real. Very real!

Start investing as soon as you can. The earlier, the better.

Start investing as much as you can. The bigger, the better.

Before you close this article, one more thing. You notice how a male (Jacob) made way more money than a female (Kelly)? Highlighting income inequality.

Oh, wait! One more thing. You notice how a female started out so late than a male? Highlighting other gender gaps across four thematic dimensions: Economic Participation and Opportunity, Educational Attainment, Political Empowerment, and Health and Survival.

Anyway, thank you for listening today. I mean reading. Have a nice day.

Let’s get to the ugly truth. Since inception (July 2014), my passive portfolio is up only 2.18%, 19 times less than the market return during the period. For 2017, the portfolio returned only 3.82%, 6 times less than the market return. Um….um….um, let me try to justify the low returns.

My peers and people jealous of me would be laughing like this:

Kuroda’s evil laugh

2014-2015

When I opened the account in the summer of 2014, TD Ameritrade gave me 2 months to trade for free. So during that time, I wanted to fill the account with stocks. The only problem was I did not know which stocks to buy. At the same time, I did not know how to research potential investments.

Mostly guided by “expert” recommendations and positive headlines, I bought some stocks which destroyed my portfolio, including Ford (F), J.C.Penny (JCP), Cisco (CSCO), General Electric (GE), and General Motors (GM). In 2015, I still did not know which stocks to buy. I wanted to do my own research. I decided to research all the stocks that were bought the previous year.

From my research, I found CSCO, GE, and JCP attractive. So I decided to keep them in the portfolio. I even wrote about CSCO and GE on the blog. I did not write on JCP as I was not profoundly convinced. Funny thing is I have never shopped at JCP, just at its competitors. Even my mother did not like J.C. Penny.

I did not like F, yet I decided to keep F in the port because it was not worth getting rid of them at $10 commissions. For GM, I was on the fence. In addition to these names, I decided to research new names and bought some of them. 70% of my portfolio was in cash in January of 2015. In December, it was 42%.

The new stocks I bought in 2015 were non-dividend yielding risky names, such as Bellatrix Exploration (BXE), Twitter (TWTR), and GoPro (GPRO). All of which did not work out well to this day. BXE, because I tried to find a good energy company at the time every energy companies were distressed. I’m very active on Twitter and use GoPro most of the time. So I wanted to invest in them. At that time, I thought Twitter would get acquired, and GoPro management would start to turn things around, and the Karma Drone would be positive for the company’s financials.

2016-2017

In 2016, I continued to research new stocks. However, I did not invest in any of them. I deposited more money into the account during that year. At the end of 2016, 82% of the portfolio was in cash.

I always found real estate interesting. Used to read about them. My interest in the real estate market skyrocketed after my first ever internship, at a small real estate firm. In January of 2017, I decided to buy WPC, a Real Estate Investment Trust (REIT). During the year, I also bought Verizon (VZ). I did not want the remaining cash in the port to sit idle. So I decided to purchase free commission based short-term bond funds, very stable dividend yielding cash parking (and one high-yield ETF). At the end of 2017, 17% of the port was in cash.

Over the past month, I have been researching consumer goods companies. I’m looking to add one to the port. When I do, I will be sure to write about it.

10 Equities

I’m currently holding 10 companies; CSCO, GE, GM, BXE, WPC, JCP, F, TWTR, GPRO, and VZ.

All shares of 10 different companies belong to 1 class: domestic equity. 62% are in large cap., and 38% are in mid-cap.

On February 16, 2015, I recommended going long Microsoft (NASDAQ: MSFT) when the share price was $43.95. Since then, it is up 101%*. I made a mistake of not buying when I wrote about it. “Put your money where your mouth is, Khojinur.”

On April 12, 2015, I recommended going long General Electric (NYSE: GE). Since then, GE is down 33%*. Dividends are automatically invested in new shares. Average price I paid for the shares is $26. I’m down 29%. Despite the 50% dividend cut recently, I’m staying with the stock for two reasons. The cost-cutting will be the best bet for us the shareholders. The $7 commission fee won’t be worth it, especially since the stock was bought in 2015 when I had less money. If I can open second Robinhood account, I’ll transfer from Ameritrade to the free-commission based brokerage.

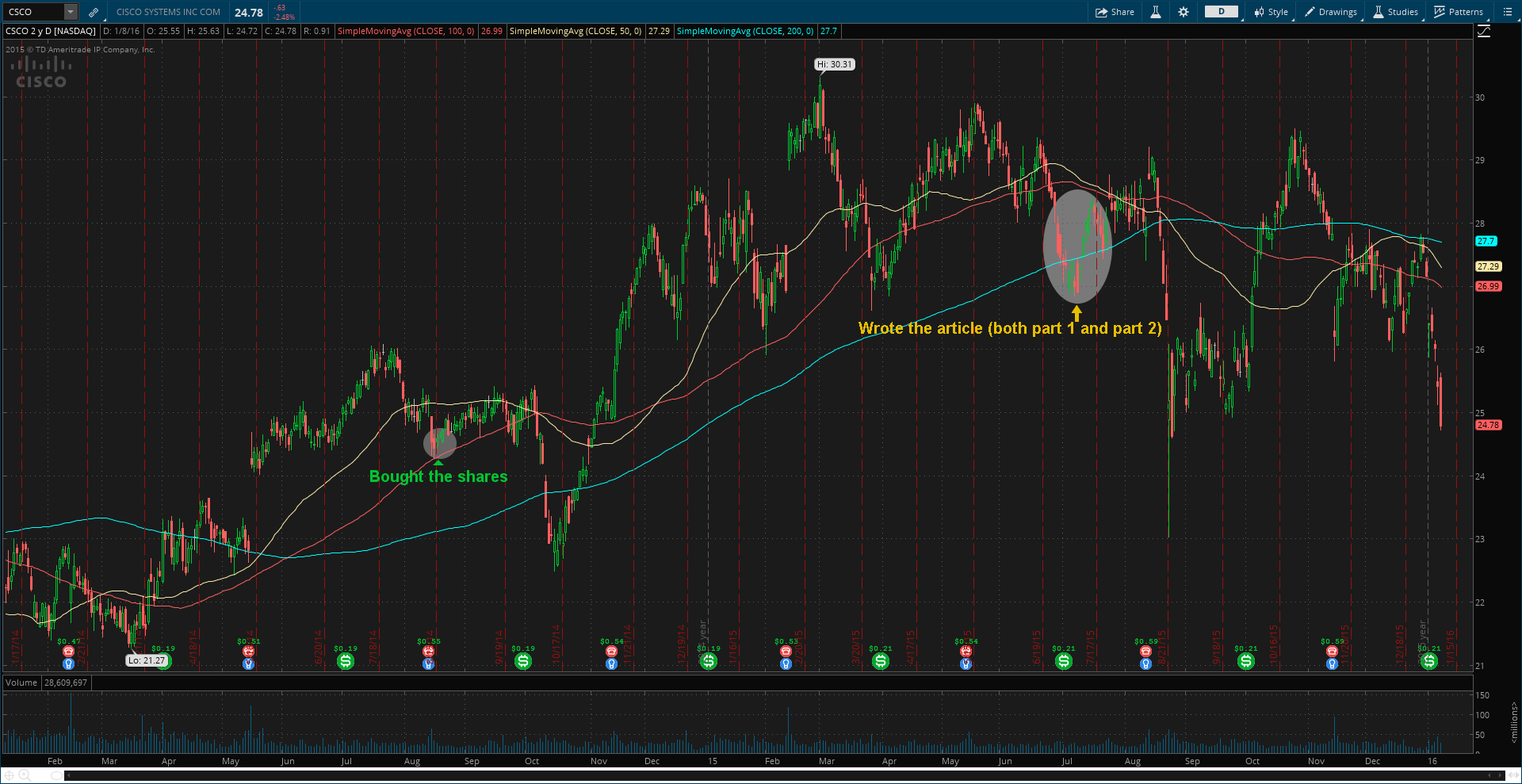

In the summer of 2015, I wrote about CSCO (part 1, part 2 AND 4Q FY’15 earnings report). Since the first article, the networking giant is up 44%*. Average price I paid for the shares is $25.11. I’m currently up 57%.

On November 21, 2015, I wrote my first article on LLY and believed it was overvalued (it still is). Since then, the pharmaceutical company is up a mere 1.25%*. The second article on LLY was posted a year after the first article. I personally am not short the stock as I cannot short.

On December 26, 2015, I recommended going long GoPro (NASDAQ: GPRO) and believed it was a buy. Since then, the action camera maker and I are down whopping 59%.

On May 2, 2016, I recommended holding FireEye (NASDAQ: FEYE). Since then, the cybersecurity firm is down 15%.

On January 20, 2017, I recommended going long W.P. Carey (NYSE: WPC). Since then, the REIT is up 11%*. Average price I paid for the shares is $61.44. I’m currently up 10%.

On May 9, 2017, I recommended going long Verizon (NYSE: VZ). Since then, the telecom is up 46%*. Average price I paid for the shares is $46.05. I’m currently up 47%.

*dividends not calculated

Estimated the portfolio dividend yield is 2.48% (that is very similar to the 10-year yield), with largest being 6% and lowest 0%. I plan to increase the portfolio dividend yield by getting rid of non-dividend yielding stocks and/or buying dividend-yielding stocks. That will happen fast, if I can make second Robinhood account and transfer the portfolio to there.

When I started doing research in-depth and writing down my findings and thoughts, everything started to improve. Writing is powerful!

Every new trade and investment will first be announced on Twitter. Almost always!

In the previous article, I talked about my performance for Forex portfolio in the first quarter of 2017. This article will lay out the equity investments portfolio performance for the 1st quarter. Unlike for forex, I don’t have much performance results for equity investment portfolio….at least for now.

Cash is trash.

For the first quarter of 2017, my stock investment portfolio was down 1.31%.

In the 1st quarter, I bought W.P. Carey (WPC). In this Seeking Alpha article, I laid out why I bought the diversified REIT.

First, I had a lot of cash sitting in my portfolio. Cash did not add any value to my portfolio.

Second, the ETFs barely moves and yet offers attractive dividends that would be distributed every month, with low expense ratio. Instead of having cash be lazy, the ETFs provided free money since they barely moved in price.

And lastly, the ETFs were commission-free through my broker, Ameritrade. When opportunities arise, I can freely liquidate the ETFs position(s).

All three reasons provided me with great flexibility and free money. The average SEC 30 Day yield from the “big four” is currently 2.43%.

And lastly, I also bought iShares Core Conservative Allocation ETF (AOK). I bought this ETF for the same reasons I bought the “big four” ETFs; low risk, low fees, and attractive dividends.

The portfolio of the five ETFs mentioned above returned 2.77% in the past 5 years, with the largest quarterly loss at 2.65% in the 4th quarter of last year and the largest quarterly gain at 1.70% in the 1st quarter of last year. Year-to-date, it’s up 1.32%.

Estimated investment portfolio dividend yield is 2.8%, with largest being 6.4% and lowest 0%. I plan to increase the portfolio dividend yield by getting rid of non-dividend yielding stocks and/or buying dividend-yielding stocks.

I did not sell anything in the portfolio during the first quarter. However, I’m planning to make some changes this quarter, which will be released in the 2nd quarter performance article. But first, I will probably tweet out the changes.

32.30% of my portfolio is currently in cash. I plan to cut that in half. How will I do it? I’m not sure yet. I’m doing research on multiple companies. The one that stands out will be bought and an article about it will be posted, mostly likely on Seeking Alpha.

Note: Equity/Commodity active trading portfolio (Robinhood) performance will be posted later.

In this post, I will be giving an update on the investment ideas I wrote about.

Note: “Average price” includes Dividend Reinvestment Plan (DRIP) – the dividends I received were used to buy additional shares in the company.

On February 16, 2015, I wrote about Microsoft (NASDAQ: MSFT) and believed it was a strong buy. Ever since then, MSFT is up 19.07%, from $43.95 to $52.33 (dividends not calculated). On December 29, 2015, MSFT reached $56.85, the highest since 2000. I do not own the shares of MSFT. Yes, I did miss the opportunity. At the time, I couldn’t afford it to buy enough shares and cover the commission fees.

Microsoft Corporation (MSFT) – Daily

On April 12, 2015, I wrote about General Electric (NYSE: GE) and believed GE was also a strong buy (it still is). Ever since then, GE is up only 1.39%, from $28.06 to $28.45 (dividends not calculated). On December 28, 2015, GE reached $31.49, the highest since May 2008. I do own the shares of GE. I bought it in August 2014. The average price I own at is $25.87. I’m currently up 9.97%.

Cisco Systems, Inc. (CSCO) – Daily

Last summer, I wrote about Cisco Systems (NASDAQ: CSCO) (article part 1 and part 2) and believed it was undervalued (it still is). Ever since then, CSCO is down 11.47%, from $27.99 to $24.78 (dividends not calculated). I do own the shares of CSCO. I bought it in August 2014. The average price I own at is $24.73. I’m currently up mere 0.2%. I will take advantage (buy more shares) of lower prices.

Cisco Systems, Inc. (CSCO) – Daily

On November 21, 2015, I wrote about Eli Lilly (NYSE: LLY) and believed it was overvalued (it still is). Since then, LLY is down 3.85% from $85.50 to $81.25 (dividends not calculated). I’m not short on LLY. I cannot afford to short it, due to my capital.

Eli Lilly and Company (LLY) – Daily

On December 26, 2015, I wrote about GoPro (NASDAQ: GPRO) and believed it is a buy (it still is). Since then, GPRO is down 12.10% from $18.34 to $16.12.

Ahh! GoPro (NASDAQ: GPRO). A stock that gravity took over. It crushed from $98.47 (early October 2014) all the way down to $15.90 (mid December 2015). Boy, was Citron Research right, when they predicted share-price would drop to $30 within a year, in November of the last year.

And what now? Is this end of GoPro or is there more?

As for me, I’m very skeptical of the market. I’m someone who loves to go against the investments of the crowd.

For example, when the Alibaba (NYSE: BABA) was launched, I was convinced that the market was hyped about it and I didn’t find any intrinsic value in BABA’s share price. Recent market sentiment about GoPro is SELL SELL SELL!!! Me being the skeptic, I say BUY BUY BUY!!!

And it’s not just because of my skepticism of the market, but because of Karma and more.

Karma is coming in 2016 for the short-sellers of GPRO. So take your profit while you can. GoPro has planned to launch its first drone, Karma in 2016. The introduction of a drone will expand camera maker’s product line, beyond making action cameras.

GoPro founder and CEO Nick Woodman said at the TechCrunch conference in September that the company is planning to launch a drone in the first half of 2016, “development is on track for the first half of 2016. We have some differentiations that are right in the GoPro alley.” Karma is finally coming.

Hollywood is eager to change the way they take aerial shots. Not long ago, they used helicopters (some still do) to shoot from bird’s point-of-view and it costs a lot. Drone makes it all cheaper. Not only cheaper, but also safer and opens more creative ways of shooting a video. In other words, drones can do what helicopters cannot do.

On May 28, GoPro announced at Google’s I/O conference that it will build a 360-degree camera array for stereoscopic spherical videos. With the help of Google Jump, Google’s virtual reality system, GoPro’s camera array, Odyssey can make videos like this. I believe the Odyssey can be very useful for real estate market. “360-Degree Real Estate Tour – Brought to you by GoPro.”

Oh, did I mention Odyssey has 16 cameras that work together as one? I repeat, 16. Hey GoPro, why don’t you knock out your useless and wasteful $300 million buyback program out of the park? According to its third-quarter SEC filing (10-Q), GoPro stated,

“To the extent that current and anticipated future sources of liquidity are insufficient to fund our future business activities and requirements, we may be required to seek additional equity or debt financing. In the event additional financing is required from outside sources, we may not be able to raise it on terms acceptable to us or at all.”

They spend 345x more on buybacks than they do on research and development. So GoPro, eliminate your worthless buyback program. “Customize” the money into research and development, and acquisitions. Customize the Odyssey. 16 cameras? Really? Reduce the size and improve the quality.

I strongly believe GoPro should acquire a small thermal imaging company. Thermal imaging can be a perfect fit for drones. I suggest GoPro acquires Seek Thermal, designer and manufacturer of high quality thermal imaging products. If GoPro acquires Seek Thermal or a different thermal imaging tech company, they will be able to reach sectors such as firefighting and agriculture. Diversified!

Another great acquisition can be Vuzix (NASDAQ: VUZI), a Google Glass rival, and a leading developer and supplier of smart glasses and video eyewear products in the consumer enterprise and industrial markets. Vuzix holds over 41 patents and 10 additional patents pending. Market cap. is currently $104.39 million. With $513 million cash on hand, GoPro can afford the acquisition. In January, Vuzix received a $24.8 million investment from Intel (NASDAQ: INTC). Intel bought preferred stock that is convertible into common shares equivalent to 30% of Vuzix.

In the third-quarter, GoPro’s revenue increased 43% year-over-year (Y/Y) to $400.3 million. On non-GAAP basis, its net income, operating income, and operating expenses increased 103.9% Y/Y, 71.7% Y/Y, and 44.3% Y/Y, respectively. On GAAP basis, it increased 28.58%, 105.36%, and 43.78%, respectively. The growth isn’t bad for a company with a market cap. of $2.49 billion. However, its inventory days increased 80.6% Y/Y from 67.7 to 122.3.

There are buyout rumors and one of the potential suitors being Apple (NASDAQ: AAPL). While this is a great news, it is not likely to happen in the first half of 2016. I believe the management of GoPro would not want to sell the company until they see the outcome of Karma. If the outcome is positive, the company will not be sold next year. If it is negative, the company will be sold unless they have something up in their sleeves. Management’s actions should a sign of what’s to come.

I’m confident the founder of GoPro will turn things around next year. GoPro can be a leader in its field if it eliminates the buyback program and invests into the future. According to Futuresource Consulting, the global action camera market grew by 44% Y/Y in 2014. It is expected to grow at a compound annual growth rate (CAGR) of 22.2% between 2014 and 2019. GoPro should target not only sport enthusiasts, but the film and television industry, real estate, and other sectors such as, firefighting and agriculture. In order to do that, GoPro should first create a product that suits the sector’s needs. First impressions are important.

Disclosure: I’m currently long on the stock, GPRO, at this time (December 26, 2015).

Note: All information I used here such as revenue, net income, etc are found from GoPro’s official investor relations site and its SEC filings.

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.