On June 23rd, Britain people will vote to stay in or leave (Brexit) the European Union. The verdict matters a lot since it is a life-changing decision. I will briefly address some of the pros and cons of Brexit, but will further address it after the vote, especially if UK leaves EU.

Brexit Pros:

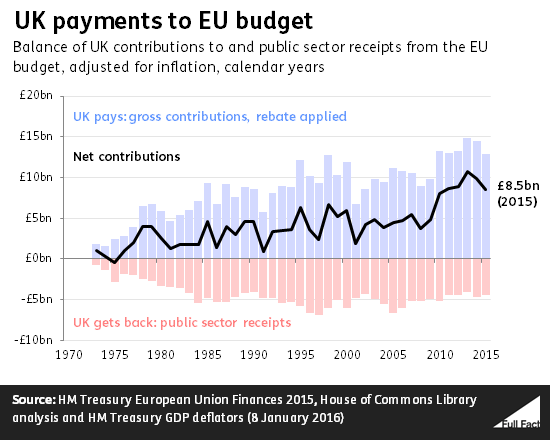

The European Union costs United Kingdom 350 million pounds ($503 million) a week. That’s $26.2 billion a year, 4.6 times less the UK education budget of $121.1 billion in 2015. That $26.2 billion is 1% of 2015 GDP of $2.63 trillion. That $26.2 billion is 2.45% of 2015 total spending of $1.07 trillion.

Note: That 350 million pounds a week cost is before “the rebate.” In 2015, Britain actually paid under 250 million ($359 million) pounds a week. But hey, UK does not control the rebates. The cost of membership has been increasing over the years, especially after the financial crisis.

What happened with Greece and is still happening, is a warning sign of more economic troubles to come in Europe. That possibly will continue to increase the cost of EU membership.

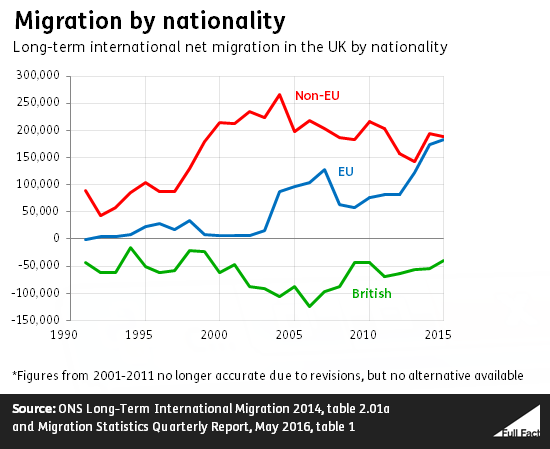

Under EU fundamental right of free movement, Britain cannot prevent anyone from another member state coming in to the country. This has resulted in a huge increase in immigration into Britain from Europe.

In 2015, 270,000 EU citizens immigrated to the UK and 85,000 EU citizens emigrated aboard. Net-migration was 185,000.

2.94 million people living in the UK in 2014 were citizens of another EU member country. Those people account for 4.7% of the UK population.

2.2 million citizens of another EU member country are in work, 7.02% of working population. Majority of EU member citizens are coming to the UK for work reasons. 61% of the migration who came for work reasons were EU citizens.

See how EU citizens coming to the UK for work reason started to accelerate in 2013. This can be related to economic difficulties such as Greece, Spain, Portugal and Italy. As I mentioned above, “What happened with Greece and is still happening, is a warning sign of more economic troubles to come in Europe.” That should lead to even more upsurge in migration for work reason, making it more competitive for UK citizens to find jobs and possibly lowering wages.

If UK decides to leave EU, the country would be able to reform immigration laws without input from the EU and increase jobs and wages for UK citizens (hopefully they have the skills).

Brexit Cons:

EU membership makes UK attractive for international investment and provides access to trade deals with more than 50 countries around the world (expensivemakeup, isn’t it?). Because EU institutions have the ability to prevent the UK from negotiating its own trade deals outside Europe, it would have to re-negotiate some trade deals, with EU and non-EU countries including the US, China, Japan and India. It is extremely possible the Brexit will impair confidence and investment for few years.

In 2015, the EU accounted for (pdf download) 43.7% of exports and 53.1% of imports

In 2014, the EU accounted for 496 billion pounds ($712 billion) of the stock of inward Foreign Direct Investment (FDI), 48% of the total. Globally, the UK is the third largest country in terms of its absolute value of inward FDI stock ($1.7 trillion), followed by China ($2.7 trillion) and U.S. ($5.4 trillion).

Why is FDI so important? It has the potential for job creation and productivity, increasing both output and wages.

If UK were to leave EU, it would dampen FDI due to uncertainty of the future. Firms would reduce investment in UK, leading to lay offs and so on (domino effect).

3.3 million UK jobs are linked to UK exports to other EU countries. Auto industry would be particularly at risk. In 2015, 77.3% of cars built in the UK were exported, a record high. EU demand grew 11.3%, with 57.5% of exports destined for the continent. In 2014, the motor vehicle manufacturing accounted for 7.9% (pdf download) of total manufacturing, up from 5.4% in 2007. The end of free trade agreements would definitely hurt UK automotive industry.

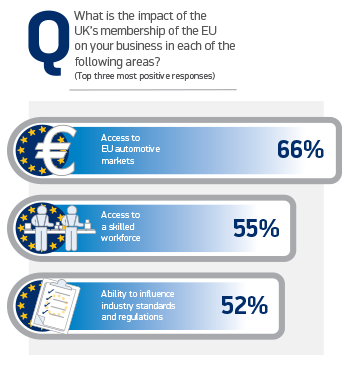

If UK were to leave the Single Market (EU), locating production in the UK would be less attractive because it would become more costly to ship to EU members. 77% of members of SMMT (Society of Motor Manufacturers and Traders) – the voice of the UK motor industry – believes remaining in EU would be the best for their business. 9% believes Brexit is the best path. 14% doesn’t know, like economists don’t know the real impact of Brexit due to a large base of issues and views.

66% believes EU important to them because of its access to EU automotive markets.

Why The EU Is Important To SMMT Members

Brexit would send a ripple effect. For the government (less tax revenue), for businesses (rising costs) and for consumers (lower income).

There’s also the issue of UK citizens in the other EU member countries. They have the right to live, work, vote, run a business, buy a property, and use public services such as health. Some, if not all, of these rights could vanish if UK leaves the EU.

Sure, UK will try to protect them. Since one of the main goals of Brexit is stop the inflows of immigrants into UK from EU, EU might retaliate against it.

UK (the wife) has been married to EU (the husband) for 43 years (UK joined EU in 1973). Part of her wants to get out of the cage. Other part of her wants to keep some of the benefits. If Brexit, it will be very expensive and messy divorce, but may be for the good.

There are so many views on this “monumental” and “out-of-focus” complicated issue. Not every issue is covered in this article. If UK is the first country to leave EU, I will do much more research and analyze it.

If you have any views, I would love to know in the comments below. If you have any questions about any issues related to Brexit, I would be happy to answer them ASAP. Don’t be surprised if the answer is 5 paragraphs long. Thank you.

12….11…10…9….IGNITION SEQUENCE START….6….5….4….3….2….1….0….ALL ENGINES RUNNING….LIFTOFF….WE HAVE A LIFTOFF!

The Fed finally raised rates after nearly a decade. On December 16, the Fed decided to raise rates – for the first time since June 2006 – by 0.25%, or 25 basis points. It was widely expected by the markets and I only expected 10bps hike. Well, I was wrong on that.

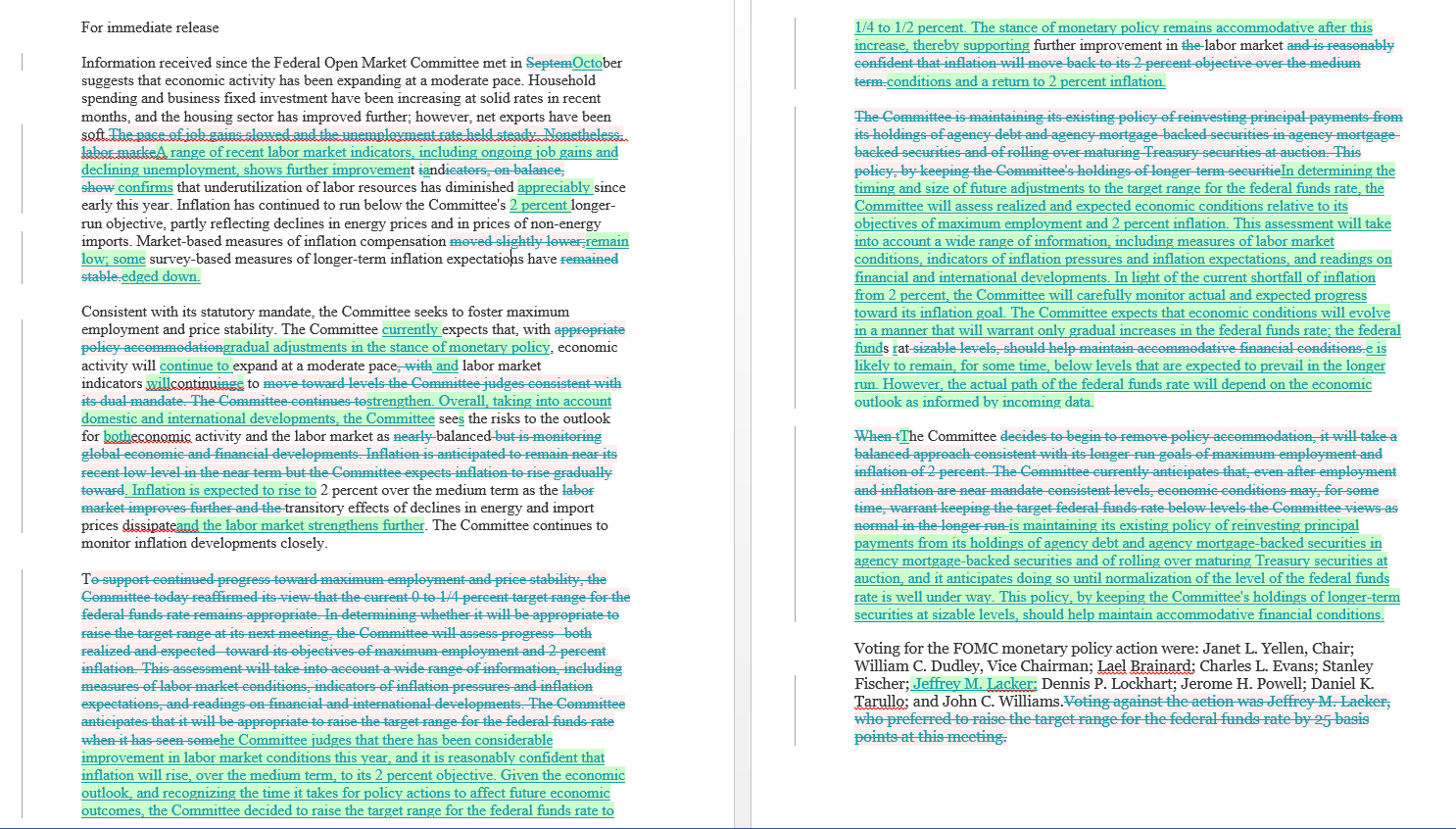

The Federal Open Market Committee (FOMC) unanimously voted to set the new target range for the federal funds rate at 0.25% to 0.50%, up from 0% to 0.25%. In the statement, the policy makers judged the economy “has been expanding at a moderate pace.” Labor market had shown “further improvement.” Inflation, on the other hand, has continued to “run below Committee’s 2 percent longer-run objective” mainly due to low energy prices.

Remember when the Fed left rates unchanged in September? It was mainly due to low inflation. What’s the difference this time?

In September, the Fed clearly stated “…survey—based measures of longer-term inflation expectations have remained stable.”

Now, the Fed clearly states “…some survey-based measures of longer-term inflation expectations have edged down.”

So…umm…why did they raise rates this time?

Here is a statement comparison from October to December:

Fed Statement Comparison – Oct. to Dec. Source: WSJ

On the pace of rate hikes looking forward, the FOMC says:

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. In light of the current shortfall of inflation from 2 percent, the Committee will carefully monitor actual and expected progress toward its inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

They clearly stated one of the things they look for, which is inflation expectations. But, they also did state that “inflation expectations have edged down.”

It seems to me that the Fed did not decide to raise rates. The markets forced them. Fed Funds Futures predicted about 80% chance of a rate-hike this month. If the Fed did not raise rates, they would have lost their credibility.

I believe the Fed will have to “land” (lower back) rates this year, for the following reasons:

Growing Monetary Policy Divergence

On December 3, European Central Bank (ECB) stepped up its stimulus efforts. The central bank decided to lower deposit rates by 0.10% to -0.30%. The purpose of lower deposit rates is to charge banks more to store excess reserves, which stimulates lending. In other words, free money for the people so they can spend more and save less.

ECB also decided to extend Quantitative Easing (QE) program. They will continue to buy 60 billion euros ($65 billion) worth of government bonds and other assets, but until March 2017, six months longer than previously planned, taking the total size to 1.5 trillion euros ($1.6 trillion), from the previous $1.2 trillion euros package size. During the press conference, ECB President Mario Draghi said the asset eligibility would be broadened to include regional and local debt and signaled QE program could be extended further if necessary.

ECB might be running out of ammunition. ECB extending its purchases to regional and local debt raises doubts about its program.

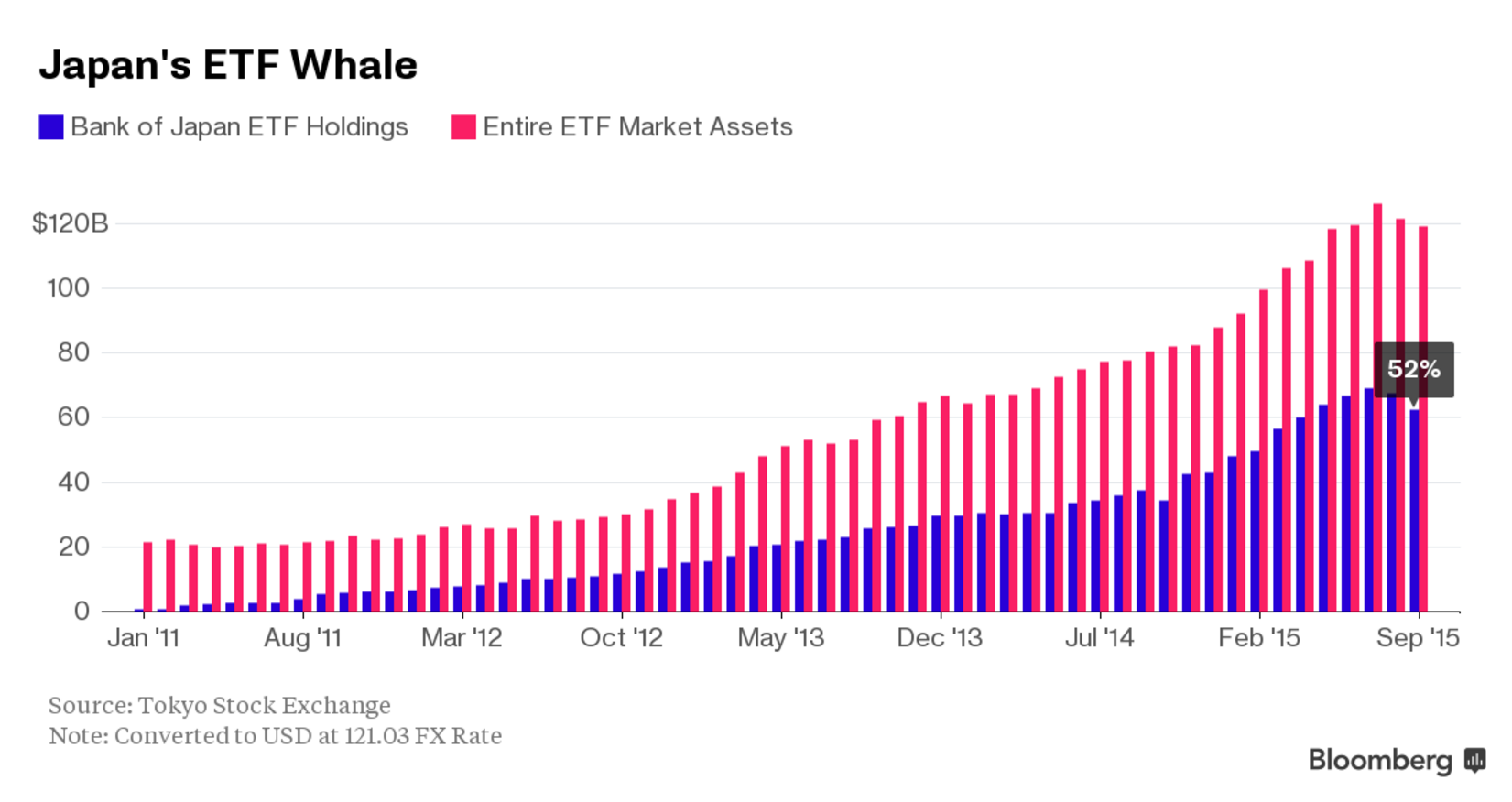

Not only ECB is going the opposite direction of the Fed. Three weeks ago, Bank of Japan (BoJ) announced a fresh round of new stimulus. The move was hardly significant, but it is still a new round of stimulus. The central bank decided to buy more exchange-traded fund (ETF), extend the maturity of bonds it owns to around 7-12 years from previously planned 7-10 years, and increase purchases of risky assets.

The move by BoJ exposes the weakness of its past actions. It suggests the bank is also out of ammunition. Already owning 52% or more of the Japan’s ETF market and having a GDP-to-Debt ratio around 245%, it is only a matter of time before Japan’s market crashes. Cracks are already beginning to be shown. I expect the market crash anytime before the end of 2019.

So, what are the side-effects of these growing divergence?

For example, the impact of a US dollar appreciation resulting from a tightening in US monetary policy and the impact of a depreciation in other currencies resulting from easing in its monetary policies. Together, these price changes will shift global demand – away from goods and services produced here in the U.S. and toward those produced abroad. In others words, US goods and services become more expensive abroad, leading to substitution by goods and services in other countries. Thus, it will hurt the sales and profits of U.S. multinationals. To sum up everything that is said in this paragraph, higher U.S. rates relative to rates around the global harms U.S. competitiveness.

Emerging Markets

Emerging markets were trouble last year. It is about to get worse.

International Monetary Fund (IMF) decided to include China’s currency, renminbi (RMB) or Yuan, to its Special Drawing Rights (SDR) basket, a basket of reserve currencies. Effective October 1, 2016, the Chinese currency is determined to be “freely usable” and will be included as a fifth currency, along with the U.S. dollar, euro, Japanese yen, and pound sterling, in the SDR basket.

“Freely useable” – not so well defined, is it?

Chinese government or should I say People’s Bank Of China (PBOC), cannot keep its hands off the currency (yuan). It does not want to let market forces take control. They think they can do whatever they want. As time goes on, it is highly unlikely. As market forces take more and more control of its exchange-rate, it will be pushed down, due to weak economic fundamentals and weak outlook.

China, no need to put a wall to keep market forces out. Let the market forces determine the value of your currency. It is only a matter of time before they break down the wall.

In August, China changed the way they value their currency. PBOC, China’s central bank, said it will decide the yuan midpoint rate based on the previous day’s close. In daily trading, the yuan is allowed to move 2% above or below the midpoint rate, which is called the daily fixing. In the past, the central bank used to ignore the daily moves and do whatever they want. Their decision to make the midpoint more market-oriented is a step forward, but they still have a long way to go.

China saw a significant outflows last year. According to Institute of International Finance (IFF), an authoritative tracker of emerging market capital flows, China will post record capital outflows in 2015 of more than $500 billion. The world’s second largest economy is likely to see $150 billion in capital outflow in the fourth quarter of 2015, following the third quarter’s record $225 billion.

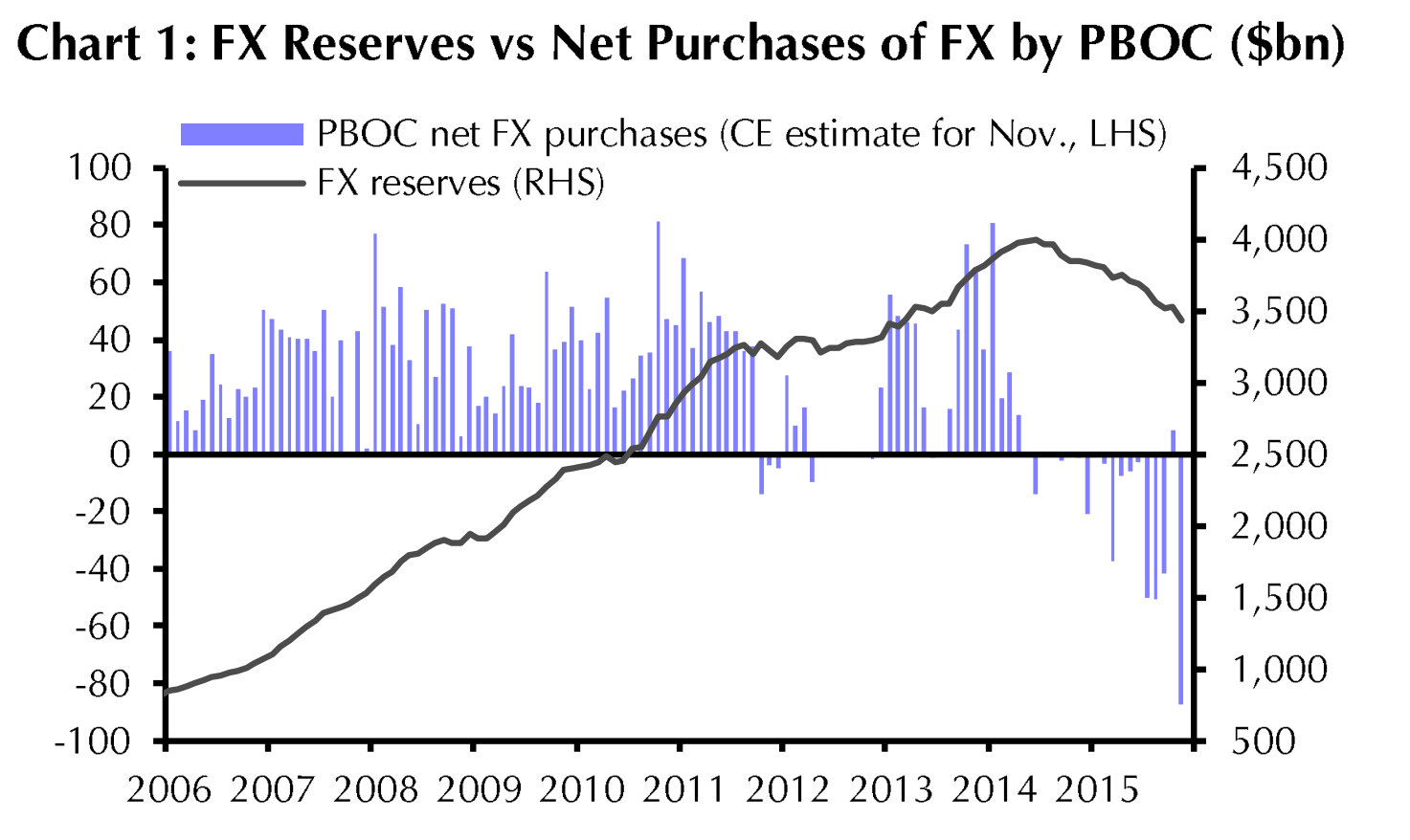

Ever since the devaluation in August, PBOC has intervened to prop yuan up. The cost of such intervention is getting expensive. The central bank must spend real money during the trading day to guide the yuan to the level the communists want. Where do they get the cash they need? FX reserves.

China’s foreign-exchange reserves, the world’s largest, declined from a peak of nearly $4 trillion in June 2014 to just below $3.5 trillion now, mainly due to PBOC’s selling of dollars to support yuan. In November, China’s FX (forex) reserves fell $87.2 billion to $3.44 trillion, the lowest since February 2013 and largest since a record monthly drop of $93.9 billion in August. It indicates a pick-up in capital outflows. This justifies increased expectations for yuan depreciation. Since the Fed raised rates last month, I would not be surprised if the capital flight flies higher, leading to a weaker yuan.

Depreciation of its currency translates into more problems for “outsiders,” including emerging markets (EM). EMs, particularly commodities-linked countries got hit hard last year as China slowed down and commodity prices slumped. EMs will continue to do so this year, 2016.

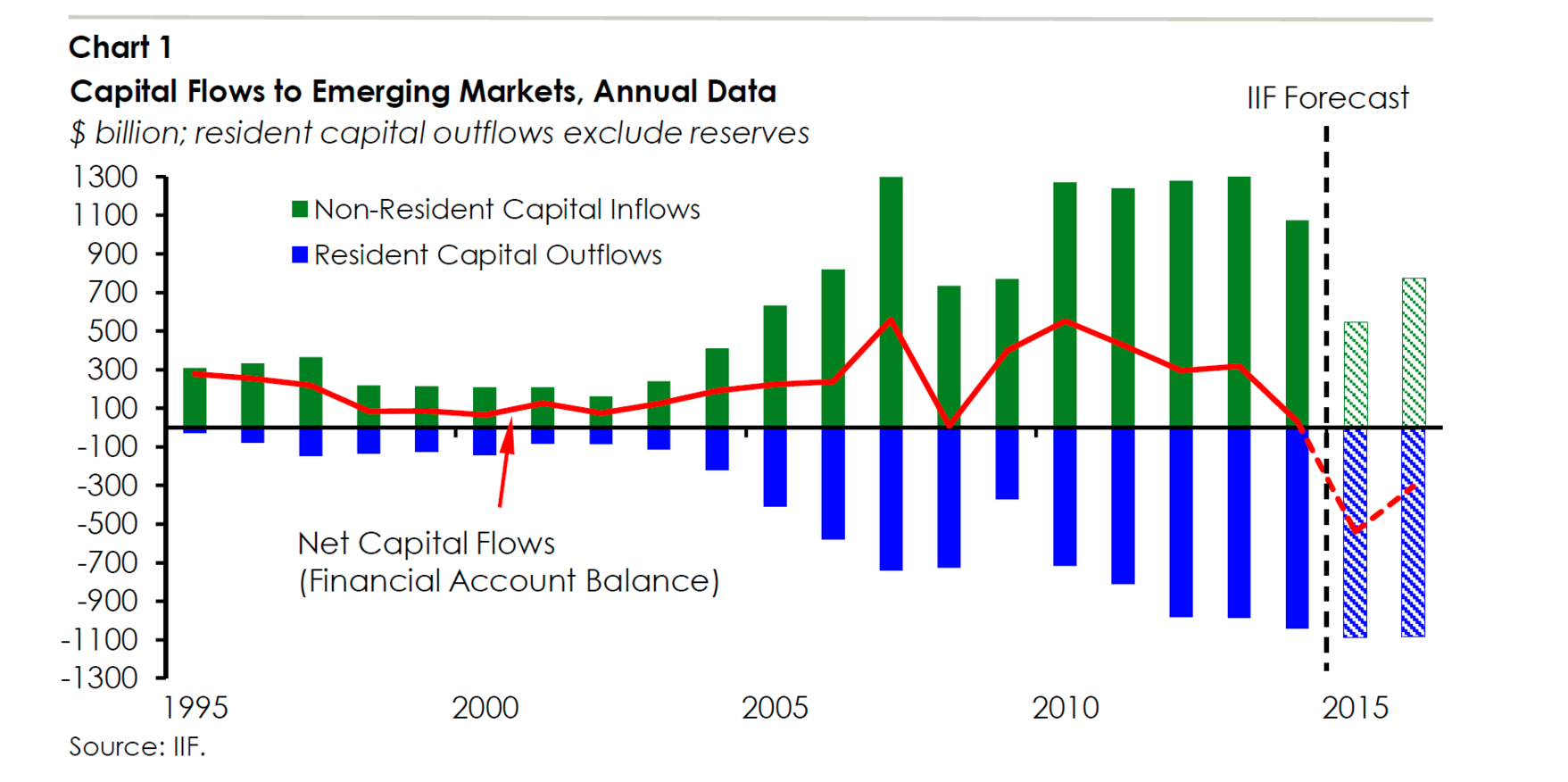

The anticipation of tightening in the U.S. and straightening dollar put a lot of pressure on EM. EM have seen a lot of significant capital outflows because they carry a lot of dollar denominated debt. According to the October report from IFF, net capital flows to EM was negative last year for the first time in 27 years (1988). Investors are estimated to pull $540 billion from developing markets in 2015. Foreign inflows will fall to $548 billion, about half of 2014 level and lower than levels recorded during the financial crisis in 2008. Foreign investor inflows probably fell to about 2% of GDP in emerging markets last year, down from a record of about 8% in 2007.

Capital Flows to Emerging Markets, Annual Data Source: IFF, taken from Bloomberg

Also contributing to EM outflows are portfolio flows, “the signs are that outflows are coming from institutional investors as well as retail,” said Charles Collyns, IIF chief economist. Investors in equities and bonds are estimated to have withdrawn $40 billion in the third quarter, the worst quarterly figure since the fourth quarter of 2008.

A weaker yuan will make it harder for its main trading partners, emerging markets and Japan, to be competitive. This will lead to central banks of EM to further weaken their currencies. Japan will have no choice but to keep extending their QE program. And to Europe. And to the U.S. DOMINO EFFECT

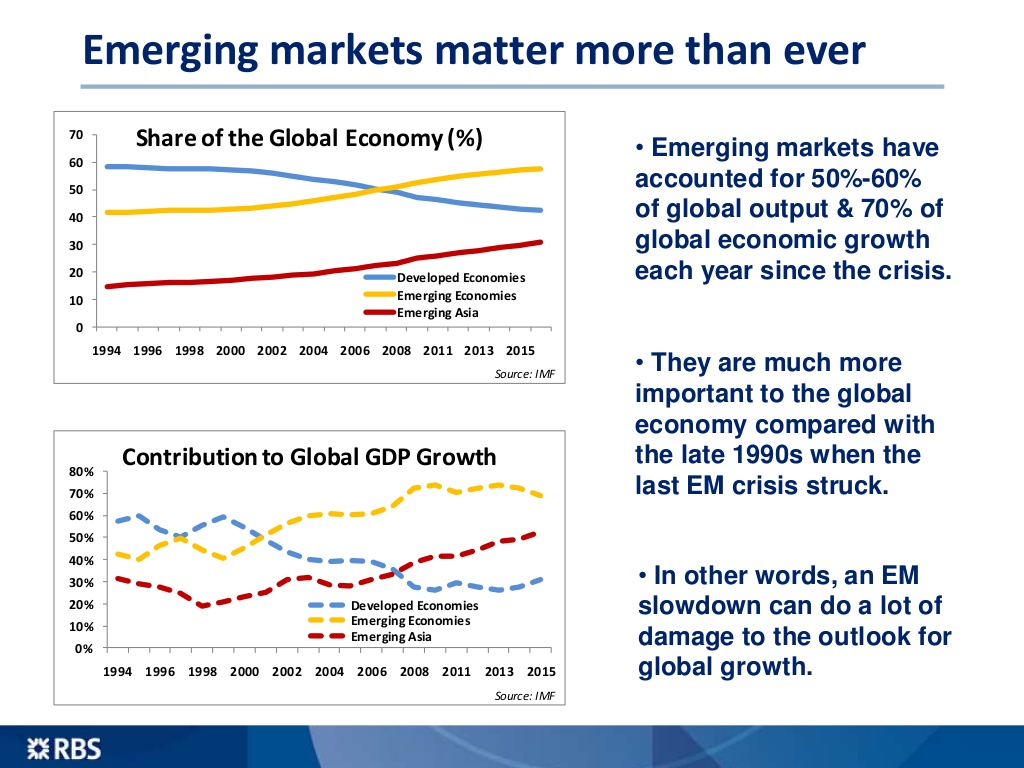

Why are EMs so important? According to RBS Economics, EMs have accounted for 50%-60 of global output and 70% of global economic growth each year since the 2008 crisis.

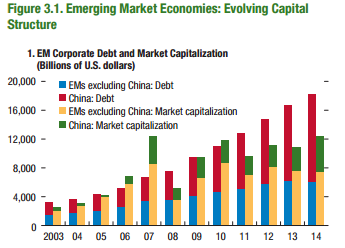

Some EM investors, if not all, will flee as U.S. rates rise, compounding the economic pain there. Corporate debt in EM economies increased significantly over the past decade. According to IMF’s Global Financial Stability report, the corporate debt of non-financial firms across major EM economies increased from about $4 trillion in 2004 to well over $18 trillion in 2014.

When you add China’s debt with EM, the total debt is higher than the market capitalization. The average EM corporate debt-to-GDP ratio has also grown by 26% the same period.

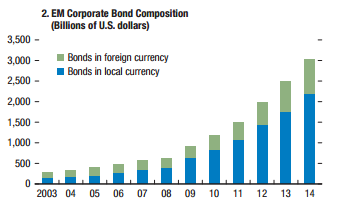

EM Corporate Debt (percent of GDP) – Page 84

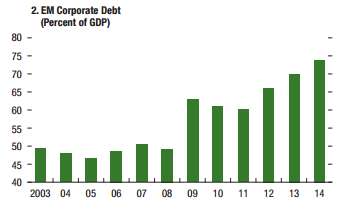

The speed in the build-up of debt is distressing. According to Standard & Poor’s, corporate defaults in EM last year have hit their highest level since 2009, and are up 40% year-over-year (Y/Y).

According to IFF (article by WSJ), “companies and countries in EMs are due to repay almost $600 billion of debt maturing this year….of which $85 is dollar-denominated. Almost $300 billion of nonfinancial corporate debt will need to be refinanced this year.”

I would not be surprised if EM corporate debt meltdown triggers sovereign defaults. As yuan weakens, Japan will be forced to devalue their currency by introducing me QE which leaves EMs with no choice. EMs will be forced to devalue their currency. Devaluations in EM currencies will make it much harder (it already is) for EM corporate borrowers to service their debt denominated in foreign currencies, due to decline in their income streams. Deterioration of income leads to a capital flight, pushing down the value of the currency even more, which leads to much more capital flight.

“Firms that have borrowed the most stand to endure the sharpest rise in their debt-service costs once interest rates begin to rise in some advanced economies. Furthermore, local currency depreciations associated with rising policy rates in the advanced economies would make it increasingly difficult for emerging market firms to service their foreign currency-denominated debts if they are not hedged adequately. At the same time, lower commodity prices reduce the natural hedge of firms involved in this business.”

According to its Global Financial Stability report, EM companies have an estimated $3 trillion in “overborrowing” loans in the last decade, reflecting a quadrupling of private sector debt between 2004 and 2014.

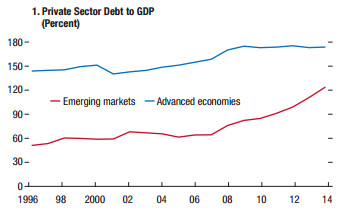

EM Corporate Bond Composition (Billions of U.S. dollars) – Page 86Private Sector Debt to GDP (Percent – Page 11

Rising US rates and a strengthening dollar will make things much worse for EMs. Jose Vinals, financial counsellor and director of the IMF’s Monetary and Capital Markets Department, said in his October article, “Higher leverage of the private sector and greater exposure to global financial conditions have left firms more susceptible to economic downturns, and emerging markets to capital outflows and deteriorating credit quality.”

I believe currency war will only hit “F5” this year and corporate defaults will increase, leading to the early stage of sovereigns’ defaults. I would not be surprised if some companies gets a loan denominated in euros just to pay off the debt denominated in U.S dollars. That’s likely to make things worse.

Those are some of the risks I see that will force the Fed to lower back the rates. I will address more risks, including lack of liquidity, junk bonds, inventory, etc, in my next article. Thank you.

EXTRA: Market reactions,

EUR/USD:

EUR/USD – Hourly Chart

USD/JPY:

USD/JPY – Hourly

10-Year Treasury Index:

10-Year Treasury Index ( “TNX” on thinkorswim platform) – Hourly

2-Year U.S. Treasury Note Futures:

2-Year U.S. Treasury Note Futures ( “/ZT” on thinkorswim platform) – Hourly

On October 22, Eli Lilly (LLY) reported an increase in the third-quarter profit, as sales in its animal health segment and new drug launches offset the effect of unfavorable foreign exchange rates and patent expirations. Indianapolis-based drug maker posted a net income increase of 60% to $799.7 million, or to $0.75 per share, as its revenue increased 33% in animal health segment. In January 2015, Eli Lilly acquired Norvartis’s animal health unit for $5.29 billion in an all-cash transaction. The increase in the animal-health revenue helped offset sharp revenue decreases in osteoporosis treatment Evista and antidepressant Cymbalta, whose revenue fell 35% and 34% year-over-year, respectively. Eli Lilly lost U.S. patent protection for both drugs last year, causing patent cliffs. Lower price for the Evista reduced sales by about 2%.

Total revenue increased 2% to $4.96 billion even as currency headwinds, including strong U.S. dollar, shaved 8% off of the top line in revenue. Recently launched diabetes drug Trulicity and bladder-cancer treatment Cyramza helped increase profits, bringing a total of $270.6 billion in the third-quarter. Eli Lilly lifted its guidance for full-year 2015. They expect earnings per share in the range of $2.40 and $2.45, from prior guidance of $2.20 to $2.30.

Despite the stronger third-quarter financial results, I believe Eli Lilly is overvalued. Eli Lilly discovers, develops, manufactures, and sells pharmaceutical products for humans and animals worldwide. The drug maker recently stopped development of the cholesterol treatment evacetrapib because the drug wasn’t effective. Eli Lilly deployed a substantial amount of capital to fund Evacetrapib, which was in Phase 3 research, until they decided to pull the plug on it. The suspension to the development of Evacetrapib is expected to result in a fourth-quarter charge to research and development expense of up to $90 million pre-tax, or about $0.05 per share after-tax. Eli Lilly’s third-quarter operating expense declined 7% year-over-year, mainly due to spending on experimental drugs that failed in late-stage testing trials.

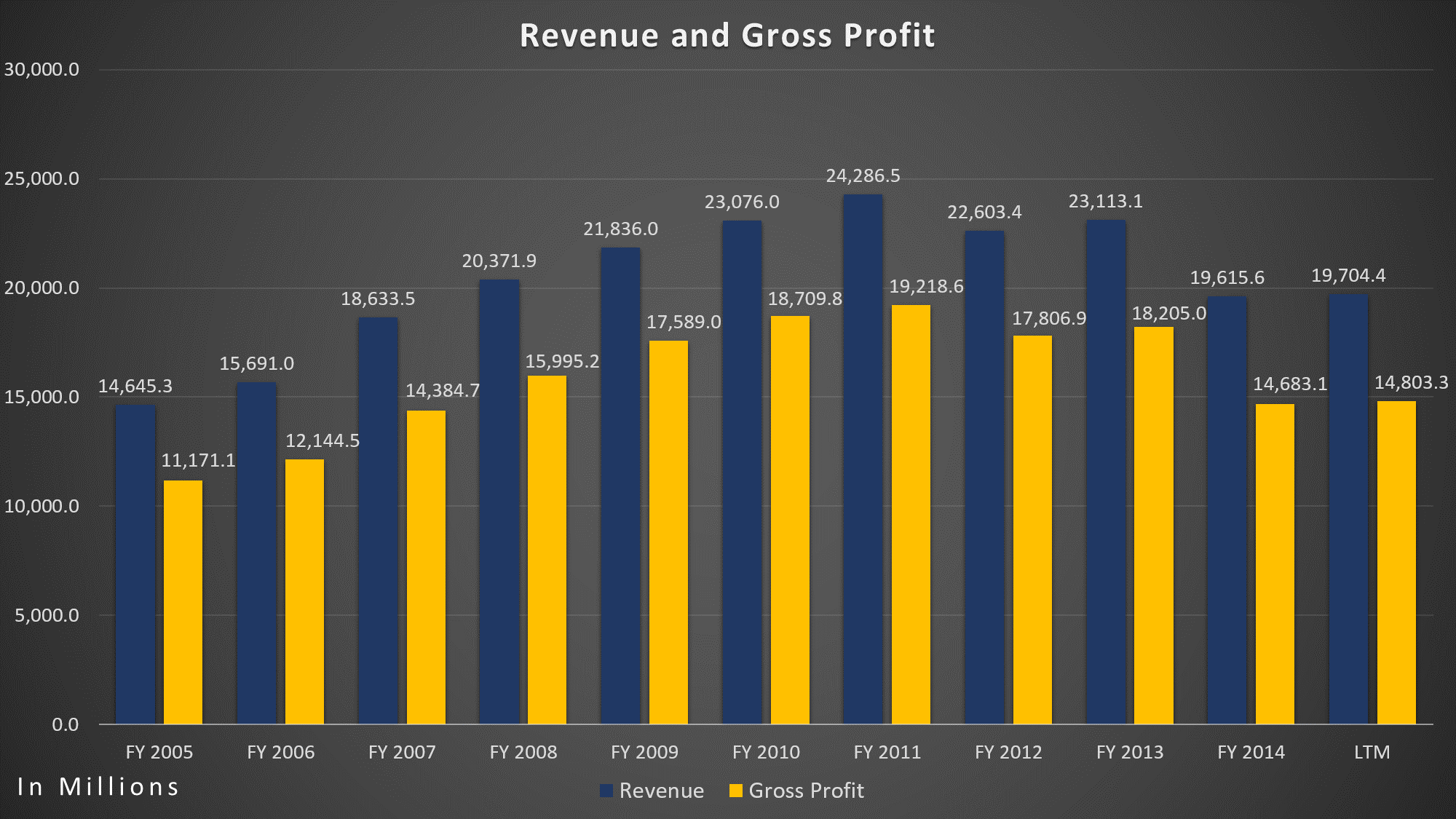

Eli Lilly’s market capitalization skyrocketed over the past five years by 122.76% to $90 billion, but their revenue, gross profit, net-income, operating income, as well as EBITDA, declined significantly. Over the past five years, its revenue decreased 14.61% from $23.08 billion to $19.70 billion (LTM), largely due to patent expirations. Gross profit and net-income declined 26.06% and 53.48%, respectively. Its operating income fell 59.18% over the past five years.

Eli Lilly – Revenue/Gross Profit

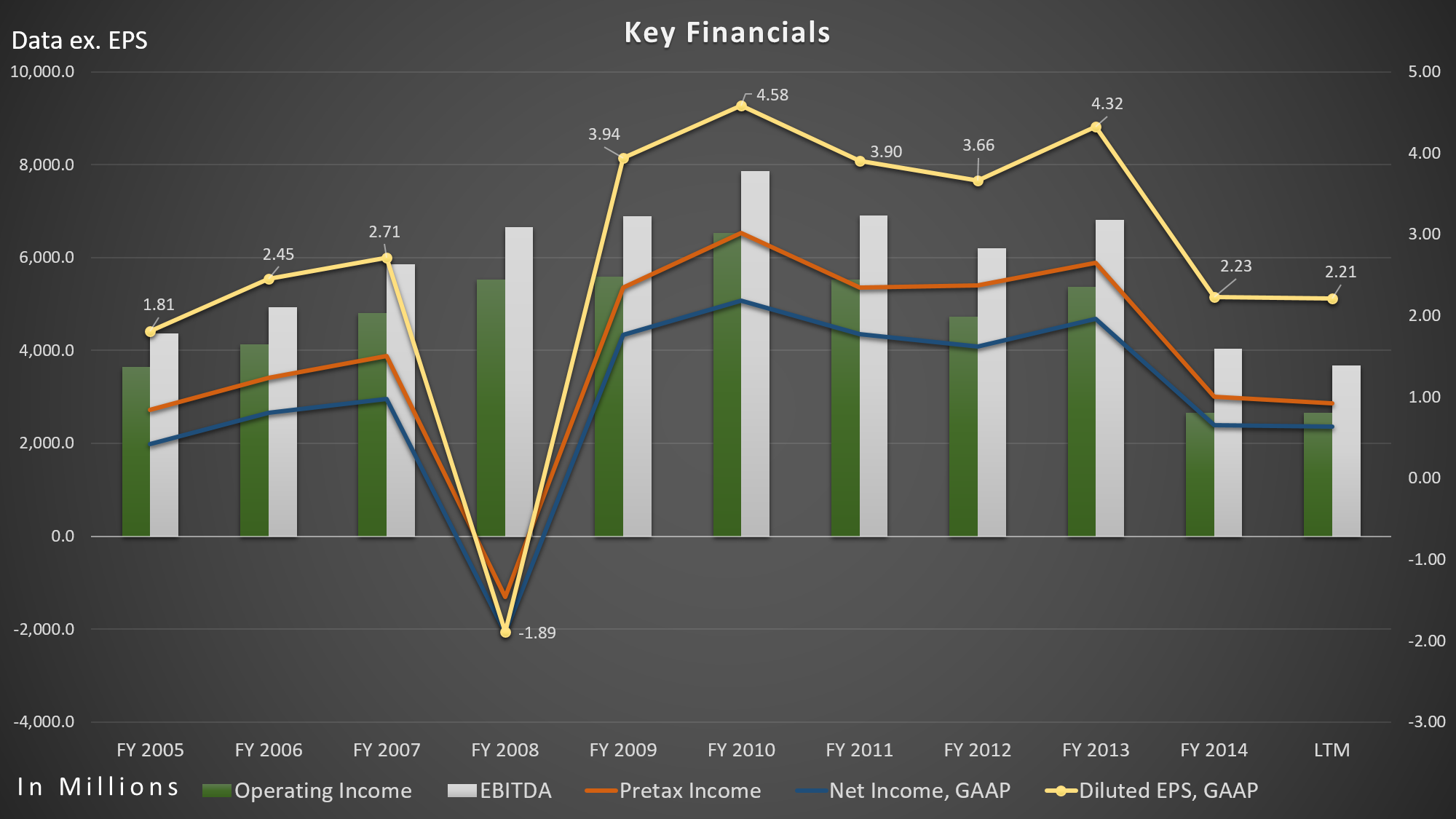

Eli Lilly – Key Financials

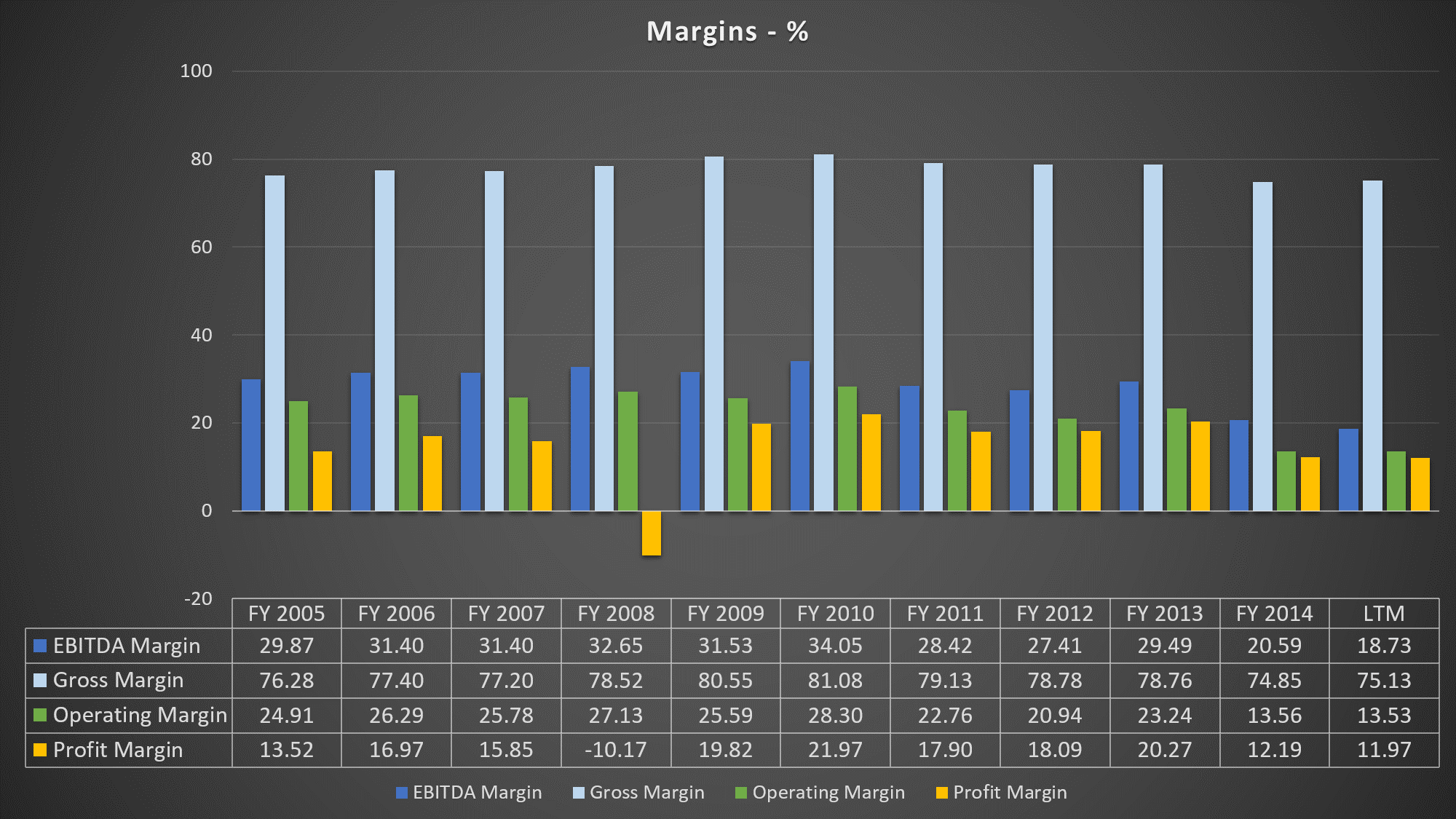

Its operating margin fell a halfway over the past five years from 28.30% to 13.53% (LTM). EBITDA margin, on the other hand, fell all the way to 18.73% (LTM) from 34.05%.

Eli Lilly – Key Margins

Meanwhile, shares of Eli Lilly gained 144.49% over the past five years. Its price-to-sales ratio too high compared to its history and to S&P 500. Its Price/Sales ratio currently stands at 4.6, vs. at 1.7 in 2010, while S&P 500 currently stays at 1.8 and industry average at 3.9. In addition to the falling revenue, gross profit, net-income, and EBITDA, its free cash flow fell significantly over the past five years by 72.24%, or fell 22.61% on a compounded annual basis.

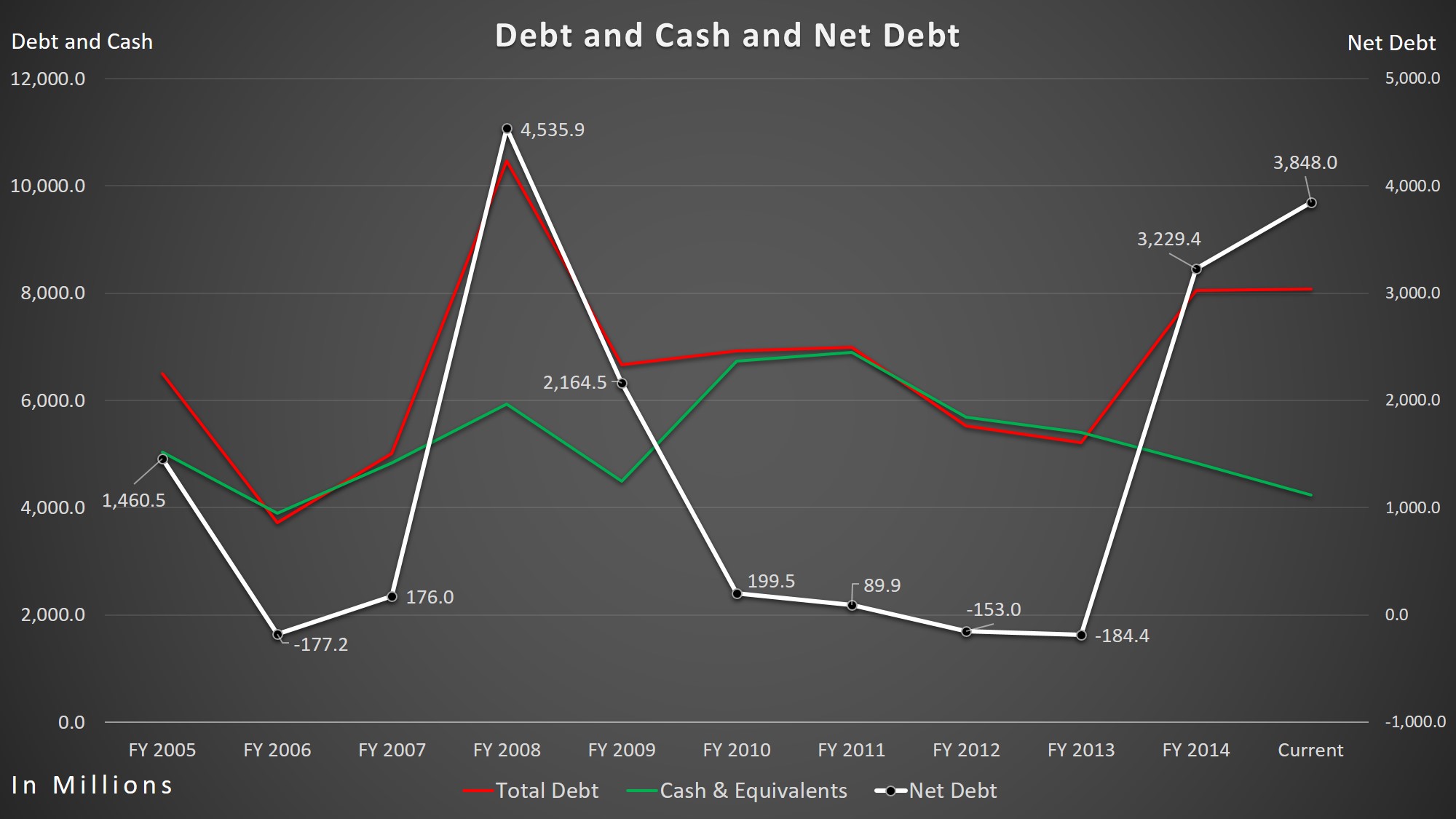

Not only did their cash flow fall, but their net-debt increased significantly. Its net-debt increased by a whopping 1789.87% over the past five years from $199.5 million to $3.85 billion. They now have almost twice as much of total debt than they do in cash and equivalents. I believe Eli Lilly is at a risk for poor future ratings by rating agencies, which will increase their borrowing costs.

Eli Lilly – Total Cash/Total Cash/Net-Debt

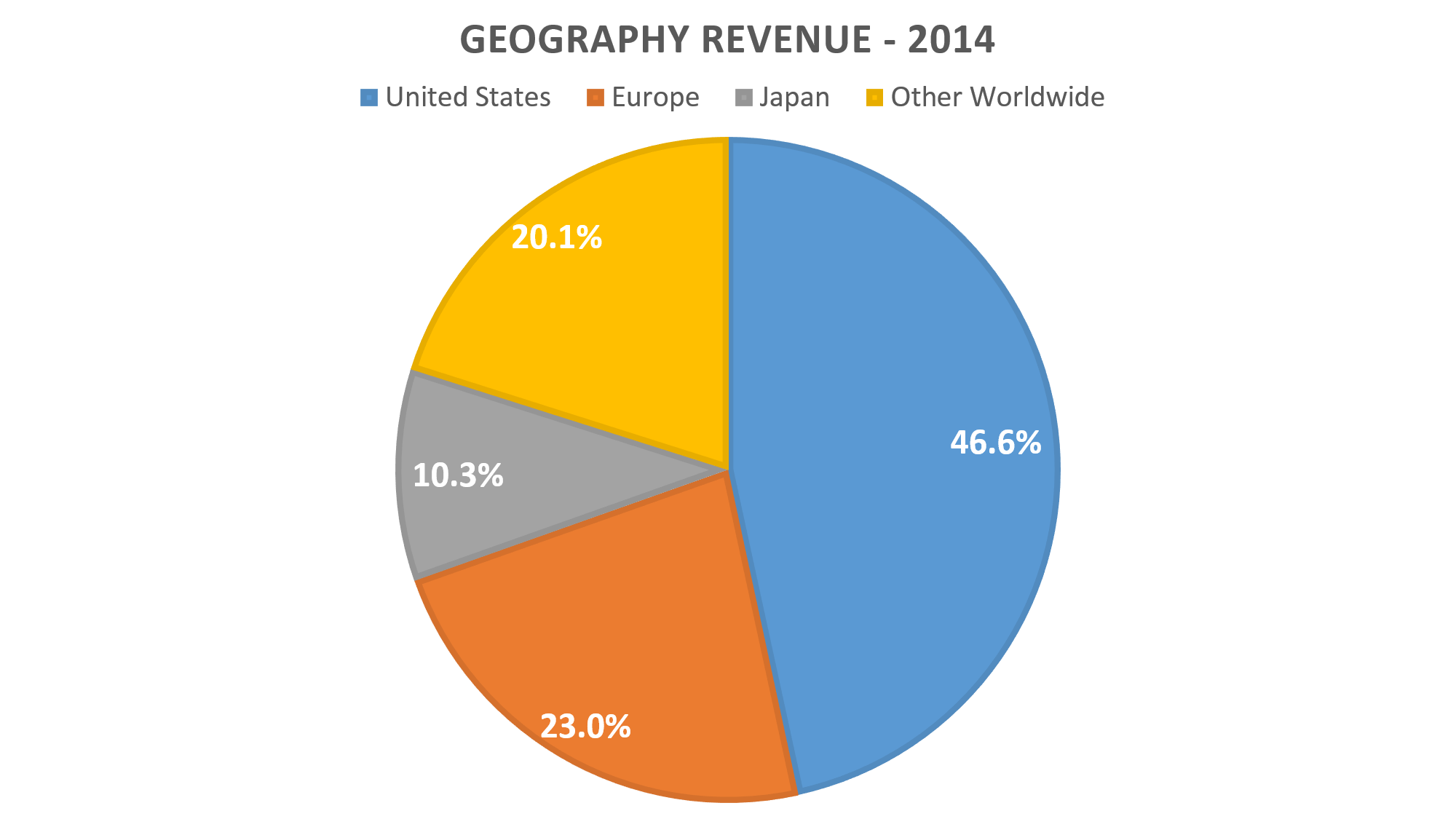

Strong U.S. dollar is an issue for Eli Lilly. Over the past five years, the dollar index increased 26.75%. Last quarter, its 49.2% of revenue came from foreign countries. Its revenue in the U.S. increased 14% to $2.54 billion, while revenue outside the U.S. decreased 9% to $2.42.

Eli Lilly – 2014 Geography Revenue

Eli Lilly’s dividend yield of 2.55% or 0.50 cents per share quarterly can be attractive, but it is undesirable. From 1995 through 2009 (expectation of 2003-2004), Eli Lilly raised its dividend. Payouts of $0.26 quarterly in 2000 almost doubled to $0.49 in 2009. Then, the company kept its dividend payment unchanged in 2010, the same year when its net-income, EBITDA and earnings per share (EPS) reached an all-time high. About four years later (December 2014), Eli Lilly increased the dividend to $0.50 quarterly. I still don’t see a reason to buy shares of Eli Lilly. The frozen divided before the recent increase was a signal that the management did not see earnings growing. With expected patent expiration of Cymbalta, their top selling drug in 2010, it is no wonder Eli Lilly’s key financials declined and dividends stayed the same. Cymbalta sales were $5.1 billion in 2013, the year its patent expired. In 2014, its sales shrank all the way down to $1.6 billion. Loss of exclusivity for Evista in March 2014 immensely reduced Eli Lilly’s revenue rapidly. Sales decreased to $420 million in 2014, followed by $1.1 billion in 2013. Pharmaceuticals industry continues to lose exclusivities, including Eli Lilly.

In December 2015, Eli Lilly will lose a patent exclusivity for antipsychotic drug Zyprexa in Japan and for lung cancer drug Alimta in European countries and Japan. Both of the drugs combined accounted for revenue of $866.4 million in the third-quarter, or 17.5% of the total revenue. They will also lose a patent protection for the erectile dysfunction drug Cialis in 2017, which accounted for $2.29 billion of sales in 2014, or 11.68% of the total revenue.

Besides the pressure from patent expirations, there is also regulatory pressures on drug pricing. According to second-quarter 10Q filing, Eli Lilly believes “State and federal health care proposals, including price controls, continue to be debated, and if implemented could negatively affect future consolidated results of operations.” During the third-quarter earnings call, CEO of Eli Lilly, John C. Lechleiter, said that price increases reflects many of medicines going generic and “deep discounts” government mandates for large purchasers.

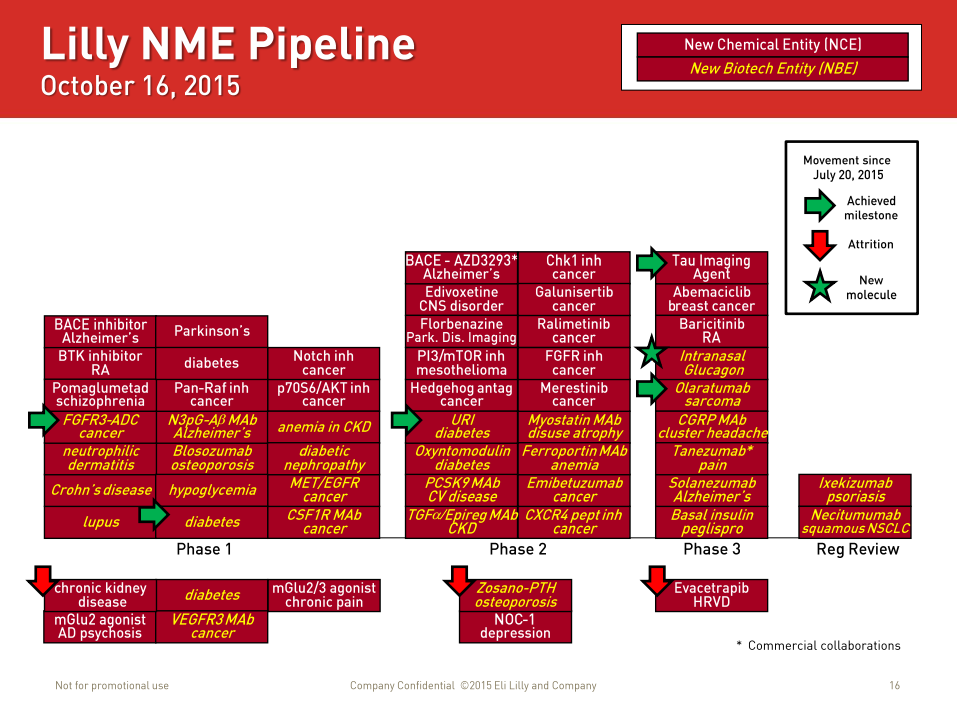

As of October 16, Eli Lilly had two drugs under regulatory review, nine drugs in Phase 3 testing, and 18 drugs in Phase 2 testing. Since the end of July, the drug maker terminated the development of few drugs, including evacetrapib in Phase 3, two drugs in Phase 2, and five in Phase 1. Out of total eight drug termination, only five drugs moved to the next stage of testing. I view the recent termination of evacetrapib as a major setback.

Compared to its peers, LLY’s Price-to-Earnings ratio is too high. Its P/E ratio (on GAAP basis) stands at 38.22 while industry average stands at 17.7. Four of its main peers, Pfizer (PFE), Johnson & Johnson (JNJ), Merck (MRK), and Sanofi (SNY) P/E ratio stands at 24.08, 19.63, 14.41, and 22.38, respectively.

Negative trends, tighter regulations, increasing competition and slowing growth makes Eli Lilly’s current valuation unjustified. I believe it will reach an average P/E ratio of its four main competitors, at 20.12, in the next three years. I expect EPS (GAAP) to contract. With current EPS of $2.21 (LTM, GAAP) and P/E ratio of 20.12, share price would be worth $44.46, down 47.37% from current share-price of $84.47. As EPS contracts, the share price of Eli Lilly will be much further down from $44.46 in the next three years.

Disclosure: I’m not currently short on the stock, LLY, at this time (October 21, 2015).

Note: All information I used here such as revenue, margins, EBITDA, etc are found from Eli Lilly and Company’s official investor relations site, Bloomberg terminal and morningstar. The pictures you see here are my own, except “Eli Lilly Pipeline – Third Quarter Earnings Presentation – Page 16”

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.

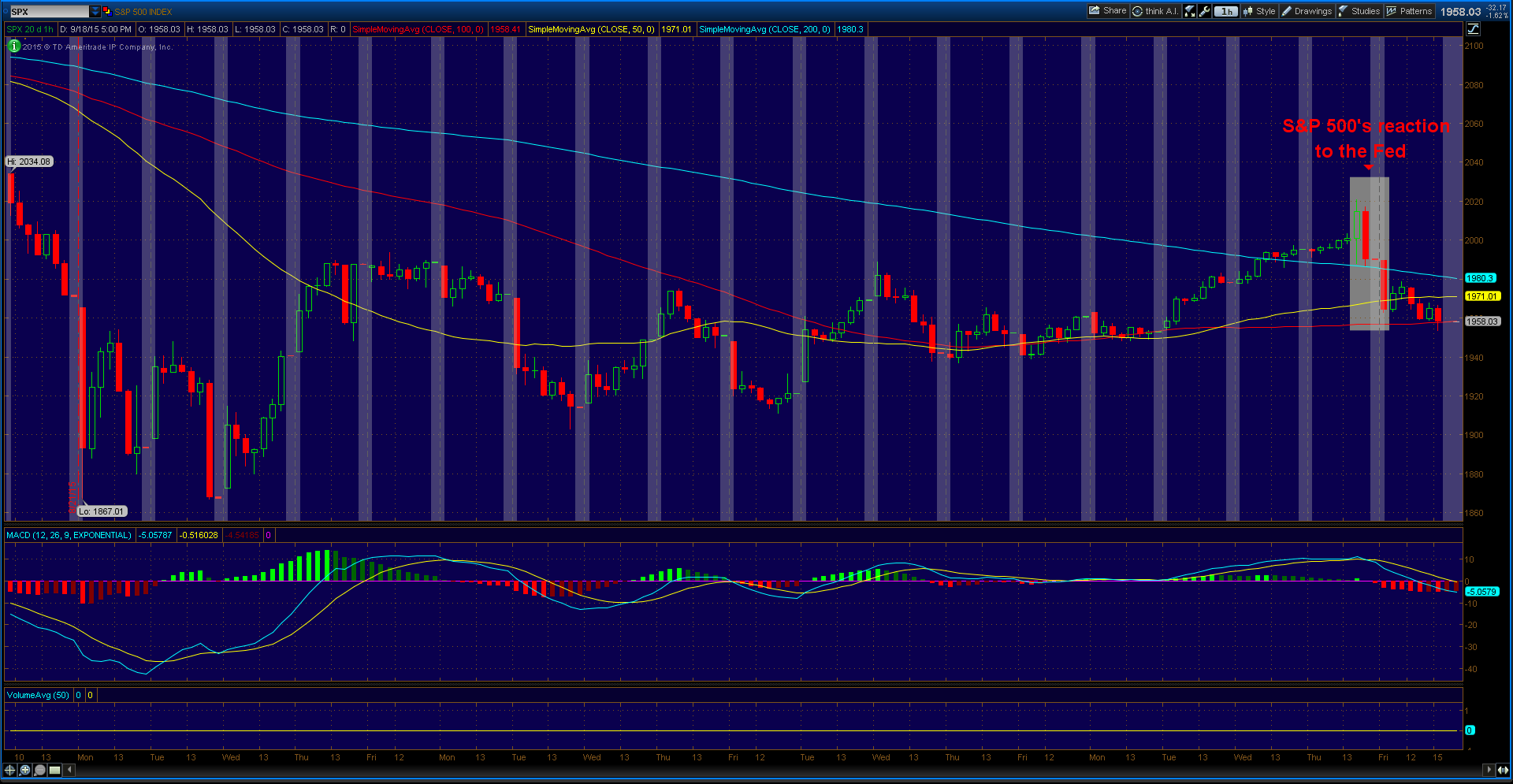

Last Thursday (September 17), the Federal Reserve left rates unchanged due to low inflation, recent turmoil in financial markets and in economies abroad, particularly China.

Markets were pricing less than 30% chance of rate-hike and most people in the financial markets were not expecting rate-hike. Well, not me. I was actually expecting 0.25%, 10 basis points rate increase, as I stated in my previous post.

“Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.” Federal Open Market Committee (FOMC) said in statement. They are referring to events that took place in August, that can be described in one word; uncertainty.

Before we go any further, let’s compare the last two Fed statements.

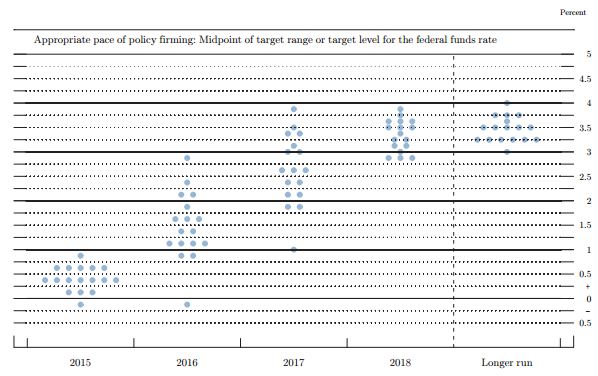

Federal Reserve “Dot Plot” – September 2015 Meeting

According to the Fed’s famous “Dot Plot” – that is where committee members think interest rates are going – one committee member, for the first time ever, thinks the U.S needs to move to negative interest rates until the end of 2016.

During the press conference, Janet Yellen – the chairwoman of the Fed – indicated that negative rates were not “seriously considered at all today” and that the policymaker in question was “concerned by the inflation outlook”. The Fed looks at a model “Phillips Curve” which states that inflation and unemployment have a stable and inverse relationship. It hasn’t been working lately.

She said something that I found very interesting, “That’s something we’ve seen in several European countries. It’s not something we talked about today. Look. If not– I don’t expect that we’re going to be in the path of providing additional accommodation but if the outlook were to change in a way that most of my colleagues and I do not expect and we found ourselves with a weak economy that needed additional stimulus, we would look at all of our available tools and that would be something that we would evaluate in that kind of context.” This shows that even the Fed is uncertain about the future and another quantitative easing is a possibility.

If you want to see the body language from Yellen as she said it, go watch the press conference video. It can be very interesting. Any body language experts here?

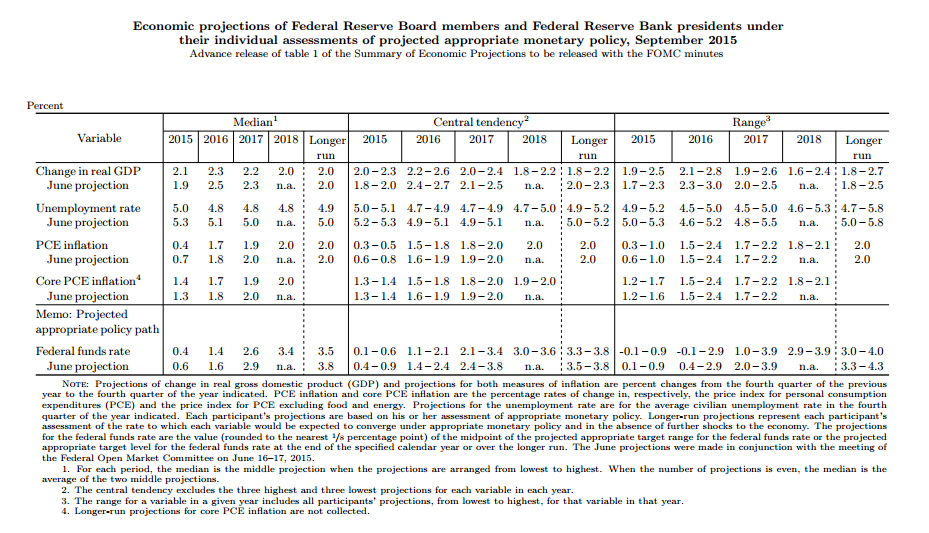

The Fed also raised growth forecast for the year and cut unemployment projection.

Federal Reserve Economic Projections – September 2015 Meeting

Yellen expressed that some countries other than China are also danger to the U.S, “…we saw a very substantial downward pressure on oil prices and commodity markets…significant impact on many emerging market economies that are important producers of commodities, as well as more advanced countries including Canada, which is an important trading partner of ours that has been negatively affected by declining commodity prices, declining energy prices….important emerging markets have been negatively affected by those developments. And we’ve seen significant outflows of capital from those countries, pressures on their exchange rates and concerns about their performance going forward. So, a lot of our focus has been on risks around China but not just China, emerging markets, more generally in how they may spill over to the United States.”

Back to “wait and see” mode again. Weak start in the year hammered the chances of rate-hike in June. Now, outsiders hammered the chances of rate-hike in September. Next stop?

If the current situation stays unchanged, I expect rate increase of 0.10% (again) in October (FOMC press conference will be called if the Fed decides to change rates). But, the current situation might get much worse. The bad news might come from China again.

Xi Jinping, China’s president and Communist Party chief, will arrive in the U.S next week to meet President Obama and business leaders. After the meeting when Mr. Xi is back in China, unpredictability arrives.

China would not want to create tension with the U.S before they meet face-to-face. Thus, unpredictability comes in two or three weeks. China might devalue their currency again, by 5% or more. They might even dump much more U.S Treasuries again.

It’s reported that China dumped U.S Treasurys of $83 billion and $94 billion in the month of July and August, respectively. Why would China sell U.S Treasurys? China is in dire need of cash. Capital outflows are increasing substantially and their stock market are declining substantially. China would want to cut its holdings of treasurys to support the yuan.

According to latest data from the U.S Treasury Department, China’s holdings of U.S Treasuries was $1.240 trillion in the end of July (is probably much less now), the smallest since February 2015. In end-June, China held $1.271 trillion. China remains the world’s largest holder of U.S debt. What does that mean for the U.S?

If U.S’s #1 lender stops supporting or stops buying U.S debt, the cost of everything that depends on Treasury rates could rise, putting pressure on the Federal Reserve and prevent the Fed from raising rates. Treasury yields (inverse relationship with prices) are the benchmark that sets the cost of borrowing.

China’s abandonment of U.S Treasury debt is a warning.

Imagine if China’s major trading partner, Japan, joins China in selling U.S Treasuries. Japan is the second-largest holder of U.S. Treasuries, with $1.197 trillion in July. The devaluation of Yuan will make Japanese exports less competitive. Japan’s economy is still suffering despite Abenomics. As I stated in my post “Global Markets Crash + Asian Crisis Part 2“, Abenomics has failed. Soon enough, Japan might also be in dire need of cash and they might start cutting their holdings of U.S Treasuries.

Recently, Standard & Poor’s slashed its ratings on Japanese debt from AA- to A+ because of weak economic growth, blaming Abenomics “…we believe that the government’s economic revival strategy–dubbed “Abenomics”–will not be able to reverse this deterioration in the next two to three years.” According to Standard & Poor, Japan’s Debt/GDP ratio currently stands at 242.4%, a dangerous level for developed country.

I believe Bank of Japan (BoJ) will increase its purchases of government debt to cover the danger of Japan’s Debt/GDP ratio and will sell portion of U.S Treasurys.

We can conclude everything will probably get much worse. The Fed will have no other choice, but to start another round of quantitative easing. In other words, debt monetization, a process of buying Treasury and corporate debt on the open market, increasing money supply. When increasing money supply, interest rates should fall.

The Fed is being held hostage by outsiders, such as China and Brazil. It probably won’t end well for the U.S, promoting another round of Quantitative Easing.