It’s all magic. Anyone can become a millionaire without special anything. All you need is money, and … abracadabra … magic works itself. That magic is compounding, like a snowball rolling down the hill.

Albert Einstein – Compound Interest quote (not proven he actually said it)

As Einstein once said, “the most powerful force in the universe is compound interest.” Well actually, nobody can confirm the quote’s true author. It’s just credit to Einstein himself to give the quote more weight. More weight as in the snowball rolling down the hill. More weight as in your investment account balance increasing.

Past S&P 500 Returns

Over the past 40 years (1978 to 2017), S&P 500 has had an inflation-adjusted annualized return rate of 8.11%, after having dividends reinvested.

After dividends and compound interest, $1,000 investment in 1978 would be $22,661*.

Over the past 30 years (1988 to 2017), $1,000 investment would be $9,595*.

Over the past 20 years (1998 to 2017), $1,000 investment would be $2,623*.

Over the past 10 years (2008 to 2017), $1,000 investment would be $2,054*.

* Note the investment values above are before any brokerage fees and taxes.

That just includes the initial investment. It doesn’t include periodic investments. Let’s include periodic investments as an example.

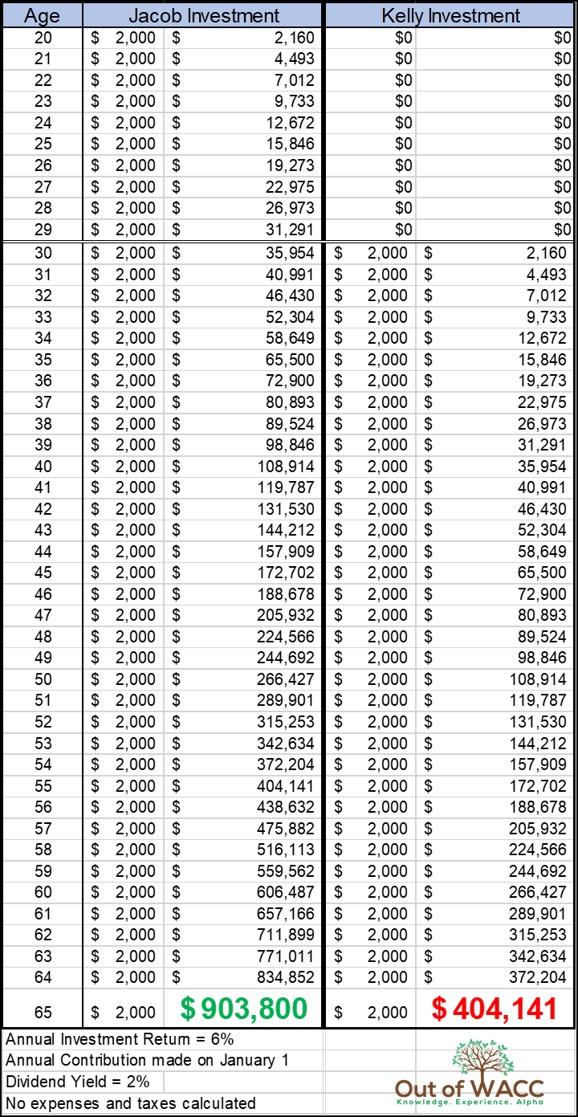

Time Is Power

Below you will see two people, Jacob and Kelly, making a periodic investment until they retire at age 65. The only difference is that Jacob starts investing at age 20. Kelly starts out late, at age 30.

Their investment will yield inflation-adjusted 5% annual return, and 2% dividend yield which automatically gets reinvested.

Jacob and Kelly, Investments

Jacob started out earlier and invested $20,000 more than Kelly. However, he came out way ahead of her by a whopping $499,659. Time is money. The power of time and compound is real. Very real!

Start investing as soon as you can. The earlier, the better.

Start investing as much as you can. The bigger, the better.

Before you close this article, one more thing. You notice how a male (Jacob) made way more money than a female (Kelly)? Highlighting income inequality.

Oh, wait! One more thing. You notice how a female started out so late than a male? Highlighting other gender gaps across four thematic dimensions: Economic Participation and Opportunity, Educational Attainment, Political Empowerment, and Health and Survival.

Anyway, thank you for listening today. I mean reading. Have a nice day.

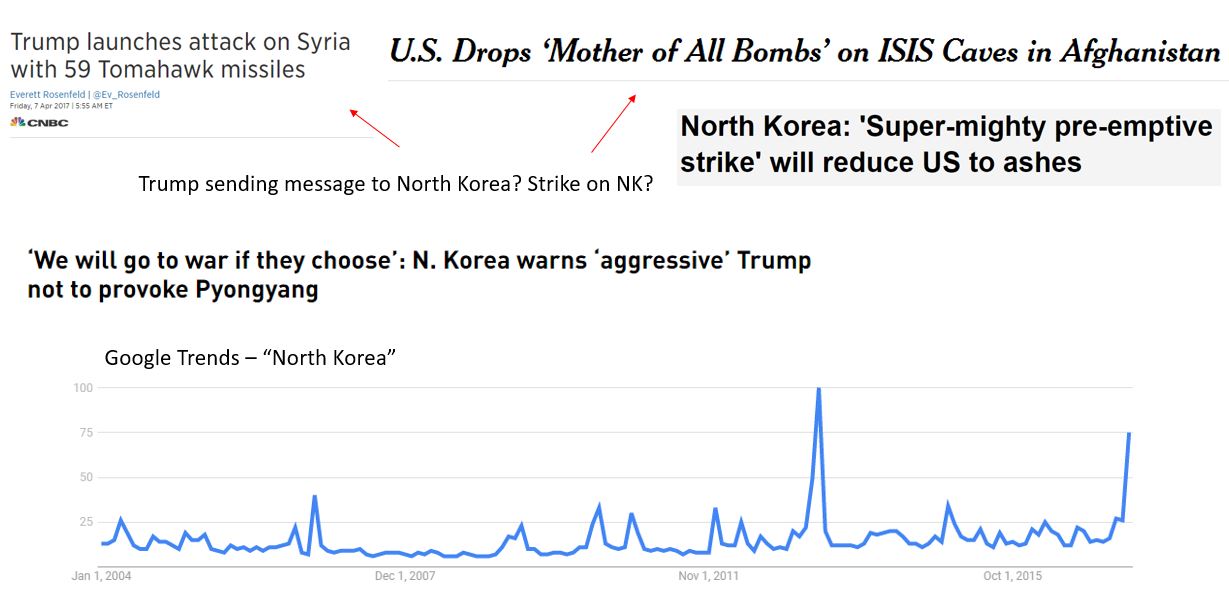

Figure 1: Trump Military Headlines. Google Trends – “North Korea”

At 17-years-old, Donald Trump was named a captain for his senior year at a military boarding school. Spending five years at New York Military Academy, the school taught Trump to channel his aggression into achievement.

Under the Trump budget, almost every budget increase goes to military departments, 10% increase Y/Y in the budget for military spending. It’s not a rocket science to figure out Trump madly loves force.

Even Trump’s Secretary of Defense loves force. Mad Dog James Mattis once said, “It’s fun to shoot some people. I’ll be right up there with you. I like brawling.”

At his confirmation hearing in January, Mattis said, “My belief is that we have to stay focused on the military that is so lethal that on the battlefield, it is the enemy’s longest day and worst day when they run into that force.”

Then there came 59 Tomahawk missiles to military bases in Syria and “Mother of All Bombs” on Daesh tunnels in Afghanistan. All of those came during the heightened tensions with North Korea.

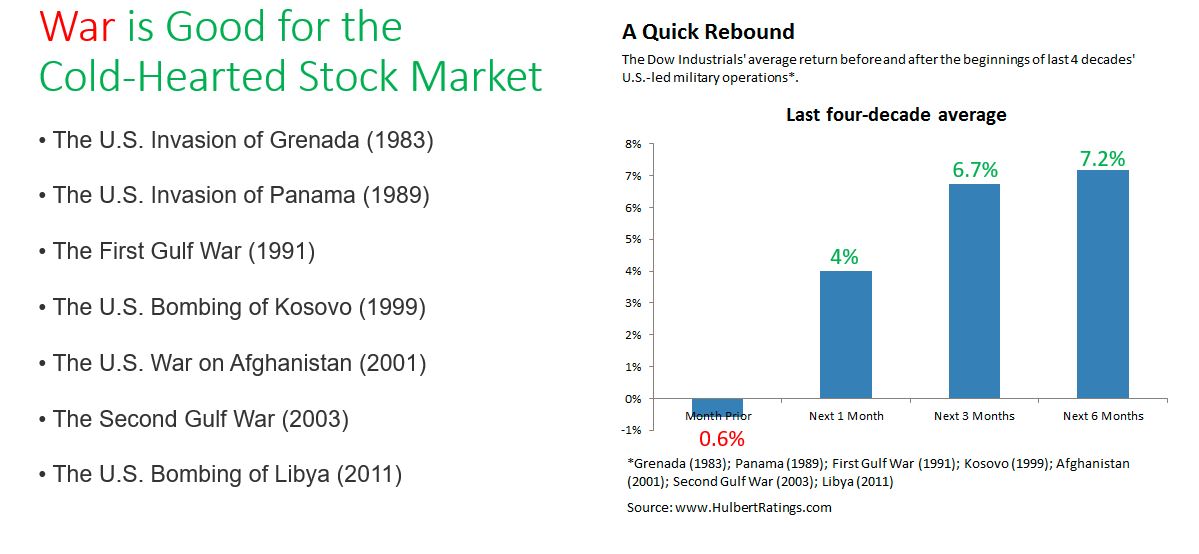

War is Good for the Cold-Hearted Stock Market

North Korea acting out is a good thing for America. War throughout the history has made us united. Not to mention that the stock market goes up.

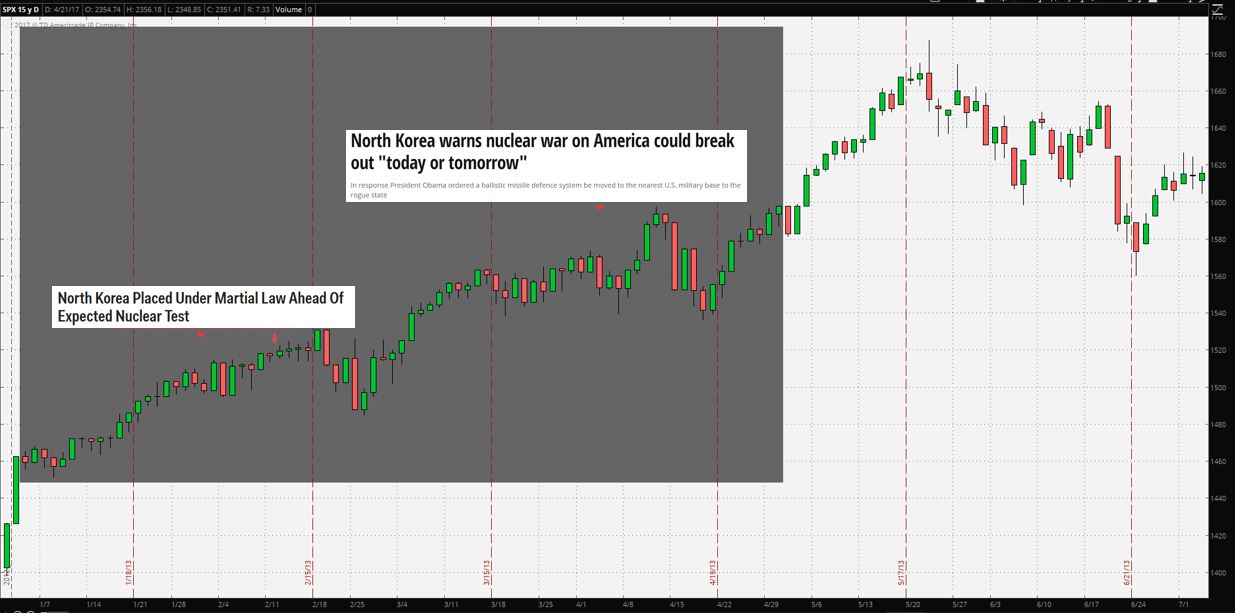

Figure 2: S&P 500 Index (SPX) – Daily Chart. The first circle represents the time of news reports on U.S. airstrikes on Syrian bases. The second circle represents the time of news reports on most powerful non-nuclear bomb being dropped in Afghanistan

As you can see in figure 2, the stock market barely reacted to the recent U.S. military actions that Trump gave a green light to.

As a trader and investor, I wouldn’t be concerned about the potential war with North Korea. (Although I would be concerned about the loss of human lives and loss of limbs.)

In early 2013, there were increased tensions with North Korea, similar to today. At the time, the stock market did not give a damn about the threats from DPRK.

Figure 3: S&P 500 Index – Daily The first headline shows two arrows. The first arrow represents when the headline came out. The second arrow represents February 12 when NK conducted the nuclear test. The second headline represents North Korea threatening the west as usually.

Not only does the stock market not care about North Korea, but also for any other war in the past century. War is good for the cold-hearted stock market.

Over the past 4 decades, Dow Industrials on average was turned on by U.S.-led military operations, returning 4% in a month after the beginning of military operations and more afterward.

Figure 4: War is Good for the Cold-Hearted Stock Market

Recent Three Wars

When the U.S., with support from allies, started bombing against Taliban forces in Afghanistan on October 7, 2001, the stock market went up, not down. Even after 12 days later when the first wave of conventional ground forces arrived, the stock market kept going up. By the year-end when Taliban collapsed, S&P 500 was up about 14.5%.

Figure 5: S&P 500’s reaction to the U.S. military action in Afghanistan – Weekly Chart

When the U.S. began the major combat operations in Iraq on March 20, 2003, the stock market skyrocketed as shown in the candlestick bar on the highlighted portion of S&P 500 Weekly chart in figure 6 below. By the time the operations ended on May 1, the stock market was up about 11.5%.

Figure 6: S&P 500’s reaction to the U.S. military action in Iraq – Weekly Chart

Figure 5: S&P 500 reaction’s to the U.S. military action in Libya – Weekly Chart

The only difference this time is we got leaders who very much loves forces and are violent themselves. Another difference is that North Korea is little powerful today than they were in 2013. But they are very weak compared to China, Russia, Europe, and U.S. It’s better to act now before North Korea gets even stronger. Although lives and limbs will be lost, I think there’s a greater cost if we allow North Korea to get even stronger.

China and North Korea

With China possibly increasingly going against North Korea, Kim Jong-un might act even more violent. I don’t think China really wants to break off its relationship DPKR due to the geographic proximity and China’s willingness to make more friends in the region. Besides being a military and diplomatic ally, China is also an economic ally. In 2015, the second largest economy accounted for 83%, or $2.34 billion, of the North Korea’s exports.

In late February, China sanctioned coal shipments from North Korea, who is a significant supplier of coal. Instead, China has been ordering the coal from the U.S. In the past, Trump said he wants to help the country’s struggling coal sector.

As Reuters reported, Thomson Reuters Eikon data shows “no U.S. coking coal was exported to China between late 2014 and 2016, but shipments soared to over 400,000 tonnes by late February.”

Is China having a change of heart on its relationship with North Korea? I don’t think as China’s trade with North Korea still increased by almost 40% in the first quarter of this year. China also buys other stuff, such as minerals and seafood. Looks like China wants to be on the good side of North Korea and Trump. The Art of the Deal.

Is this time is also different when it comes to the stock market? I don’t believe so. I’m not worried about the negative impact on the stock market due to North Korea, even though they were to be invaded.

However, I’m watching very cautiously China and Russia getting into an armed conflict with the U.S because of the North Korea situation. Armed conflict between the superpowers is a game changer. Although that’s very unlikely as superpowers argue all the time.

Suggestion For Your Portfolio

The situations might affect the markets for a very short period of time, especially if there’s uncertainty. But investors shouldn’t worry about it. The market could care less about a war, specifically when it’s aboard.

During the times of war, don’t reduce your holdings because of misconception war is bad. If you do, you will miss the gains.

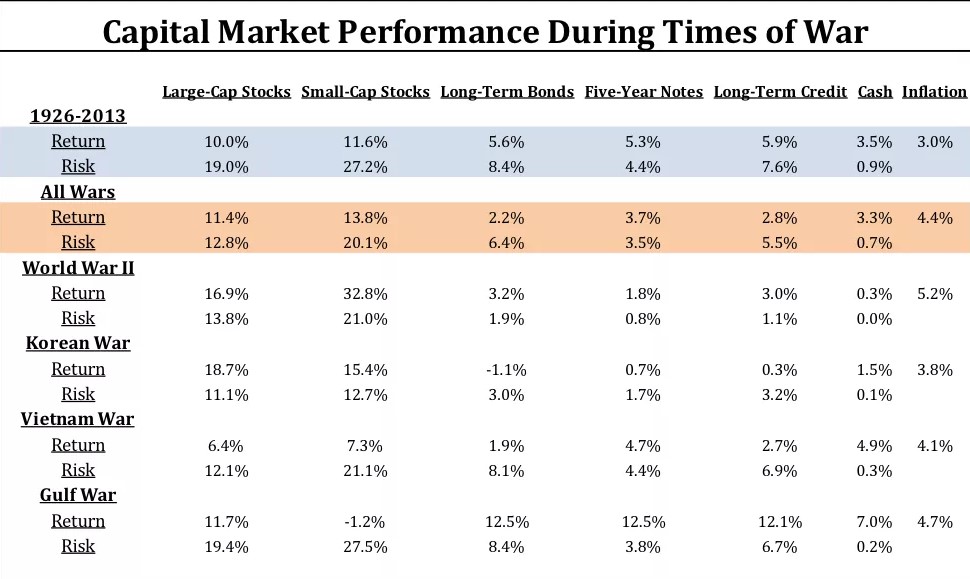

Figure 6: Capital Market Performance During Times of War Sources: The indices used for each asset class are as follows: the S&P 500 Index for large-Cap stocks; CRSP Deciles 6-10 for small-cap stocks; long-term US government bonds for long-term bonds; five-year US Treasury notes for five-year notes; long-term US corporate bonds for long-term credit; one-month Treasury bills for cash; and the Consumer Price Index for inflation. All index returns are total returns for that index. Returns for a war-time period are calculated as the returns of the index four months before the war and during the entire war itself. Returns for “All Wars” are the annualized geometric return of the index over all “war-time periods.” Risk is the annualized standard deviation of the index over the given period. Past performance is not indicative of future results.

Over the past 40 years (1977 to 2016), S&P 500 has had inflation-adjusted annualized return rate of 7.20%, that’s having dividends reinvested. That means $1 grew to $16.14.

Without dividend reinvestment, S&P 500 has had annualized return of 4.12%, which means $1 grew to $5.02.

Can you see the power of time and compounding? I hope you see it.

S&P 500: Inflation-Adjusted, With Dividend Reinvestment

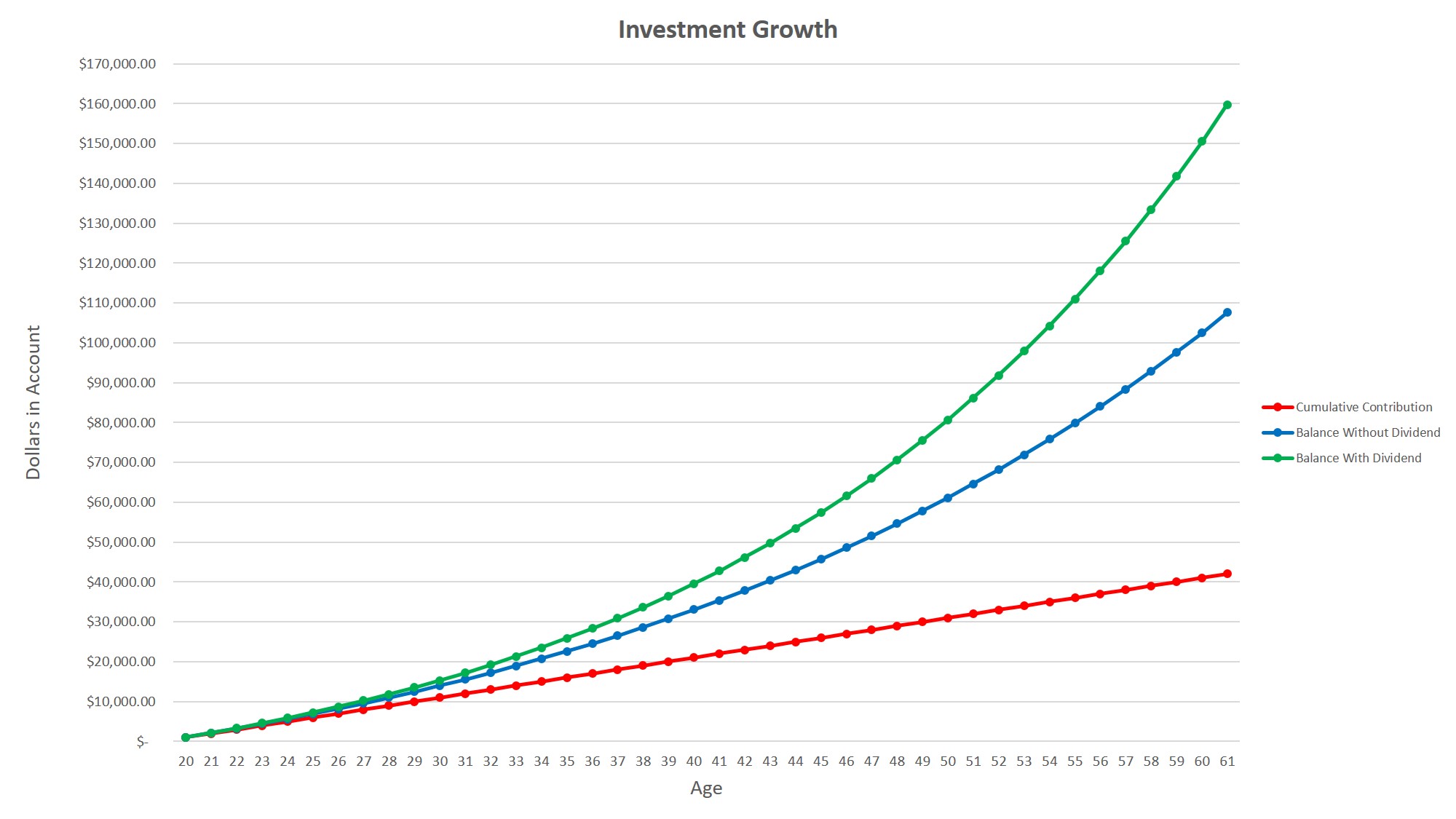

Let’s assume you’re 20-years-old, saving $1,000 each year for the next 40 years. When you’re 59, you will have $40,000 in cash. That is considering zero inflation.

Now, let’s assume you invest in the market that will give you inflation-adjusted annualized return of 5%, without dividends. When you’re 59, you will have $97,622.30.

Lastly, let’s assume you invest in the market that will give you inflation-adjusted annualized return of 5%, with 1.5% annual dividend. When you’re 59, you will have $141,731.09.

Oh My God! The Power of Time and Compounding!

If you want to invest, invest now. Don’t let all-time highs scare you.

S&P 500 is currently yielding 1.93% dividend. Since the late 1800s, the lowest dividend yield was 1.11% in August 2000. The average dividend yield is 4.38%.

The returns you see above and below are before taxes. Tax laws might be different in 2056.

In this post, I will outline some of my plans to be a very long-term investor. I’m mostly trader and investor with less than the 5-year horizon.

Money Should Not Be Emotional

Over a year ago, I tried to open a ROTH IRA (retirement) account. After filling out the answers to countless questions, the application asked me to provide a proof of income. At the time, I did not have a job. So I just gave up on the application and did not think about it until last January.

I spent so much money in December and January alone, the expense amount freaked me out. I asked myself two key questions:

What can I do to save more?

What are the non-mandatory expenses?

One of the ways I can save more is, believe it or not, recycling bottles/cans (I don’t consider it income). In a family house of 6, we drink a lot, especially water. I drink about 12 bottles of water a day….using the same bottle. I fill the bottle with boiled water. Others just waste the bottles. I rather profit from people’s mistakes.

All those bottles collected in about two weeks made me $5.65, worth almost 6 pizzas, 2 each day. Or 6 yogurts, 3 each day.

Figure 3: Bottles + Cans = Cash

If I make $10 every month for two hours of work, I can make $120 a year. That money can add up over the long term once invested in dividend-yielding ETFs.

I will not continue collecting bottles/cans (side hustle) once I get a full-time job/live on my own. I’m doing this now because I don’t even do my own laundry….yet.

I also figured out the non-mandatory expenses to cut back on, specifically on “ex”-food items I used to buy on a pulse. Small purchases (gum, candy, etc), for example, can add up over time. Those purchases are paid in cash. Well, I don’t carry a lot of cash. I carry reasonable amount. How you define ‘reasonable’ is up to you.

Why I don’t carry a lot of cash:

No track of cash flow. Credit card allows that

Risk of theft

Worried about losing the wallet

To avoid small purchases

Savings and Investing on Auto-Pilot

In January and February, I decided to open multiple accounts to keep my cash, rainy day savings, investments and deposited more money into my Robinhood brokage account.

Why multiple accounts? Because I don’t trust FDIC, which “protects” or “insurances” depositors to at least $250,000 per bank. I’m paranoid someday FDIC won’t be able to protect every depositor, after a major hack or something. Who knows, it might even take a long time to get depositors’ money back.

What if I lose my debit card? I wouldn’t want all/most of my cash in that account. At most, I keep 30% of my cash in the checking account. Now, my cash and short-term securities (stocks, etc) are diversified among multiple accounts.

Besides the savings account (almost 1% interest), I opened two more investments accounts. These accounts are different than Ameritrade/Robinhood.

Financial Literacy Is Very Important

The first account is Acorns, an investment app that rounds up user purchases and invests the change in a robo-advisor managed portfolio. For me, there’s no fee since I’m a student and under 24. I don’t trust robo-advisers, but this case is different. There are only 6 ETFs which I have looked into and decided they were good for the long-term in a diversified portfolio. 75% of its users are millennials.

79% of millennials are not invested in the stock market. I find that as a real concern.

The second account is Stash, an investment app that allows users to pick stocks in themed based investments around wants (Clean & Green, Defending America, Uncle Sam, etc). This app is also targeted toward millennials. Unlike Acorns, Stash charges you even if you are a student. But, the first three months are free. Like Acorns, Stash has a subscription fee of $1 per month for accounts under $5,000 and 0.25% a year for balances over $5,000.

Studies show 48% of Americans cite a lack of sufficient funds as their main barrier to investing. Luckily, technology is transforming the way people invest. Start small. Before you know it, it is big.

Both of the micro-investing apps are like savings/IRA accounts for me since I can grow my portfolio through dividends. I have checked out the ETFs Acorns invests in, they are good. I have checked out the ETFs Stash offers. Most of them are good. I have invested in the stable ones with low expense ratio relatively to its dividends.

Unlike ROTH IRA, I will need to pay taxes on realized capital gains, dividends and income interest.

Whopping 69% of Americans have less than $1,000 in a savings account and 50% of them have $0 in that account. All these people playing Candy Crush should be thinking about their future. Be a Robo-Saver and Be a Robo-Investor.

Note: All of my $$$ comes from off-book jobs, scholarships, prizes, and living under mommy and daddy’s roof (Can’t wait to move out). This post doesn’t mean I will stop trading. I will continue to trade forex, stocks, and commodities.