In this post, I will be giving an update on the investment ideas I wrote about.

Note: “Average price” includes Dividend Reinvestment Plan (DRIP) – the dividends I received were used to buy additional shares in the company.

On February 16, 2015, I wrote about Microsoft (NASDAQ: MSFT) and believed it was a strong buy. Ever since then, MSFT is up 19.07%, from $43.95 to $52.33 (dividends not calculated). On December 29, 2015, MSFT reached $56.85, the highest since 2000. I do not own the shares of MSFT. Yes, I did miss the opportunity. At the time, I couldn’t afford it to buy enough shares and cover the commission fees.

Microsoft Corporation (MSFT) – Daily

On April 12, 2015, I wrote about General Electric (NYSE: GE) and believed GE was also a strong buy (it still is). Ever since then, GE is up only 1.39%, from $28.06 to $28.45 (dividends not calculated). On December 28, 2015, GE reached $31.49, the highest since May 2008. I do own the shares of GE. I bought it in August 2014. The average price I own at is $25.87. I’m currently up 9.97%.

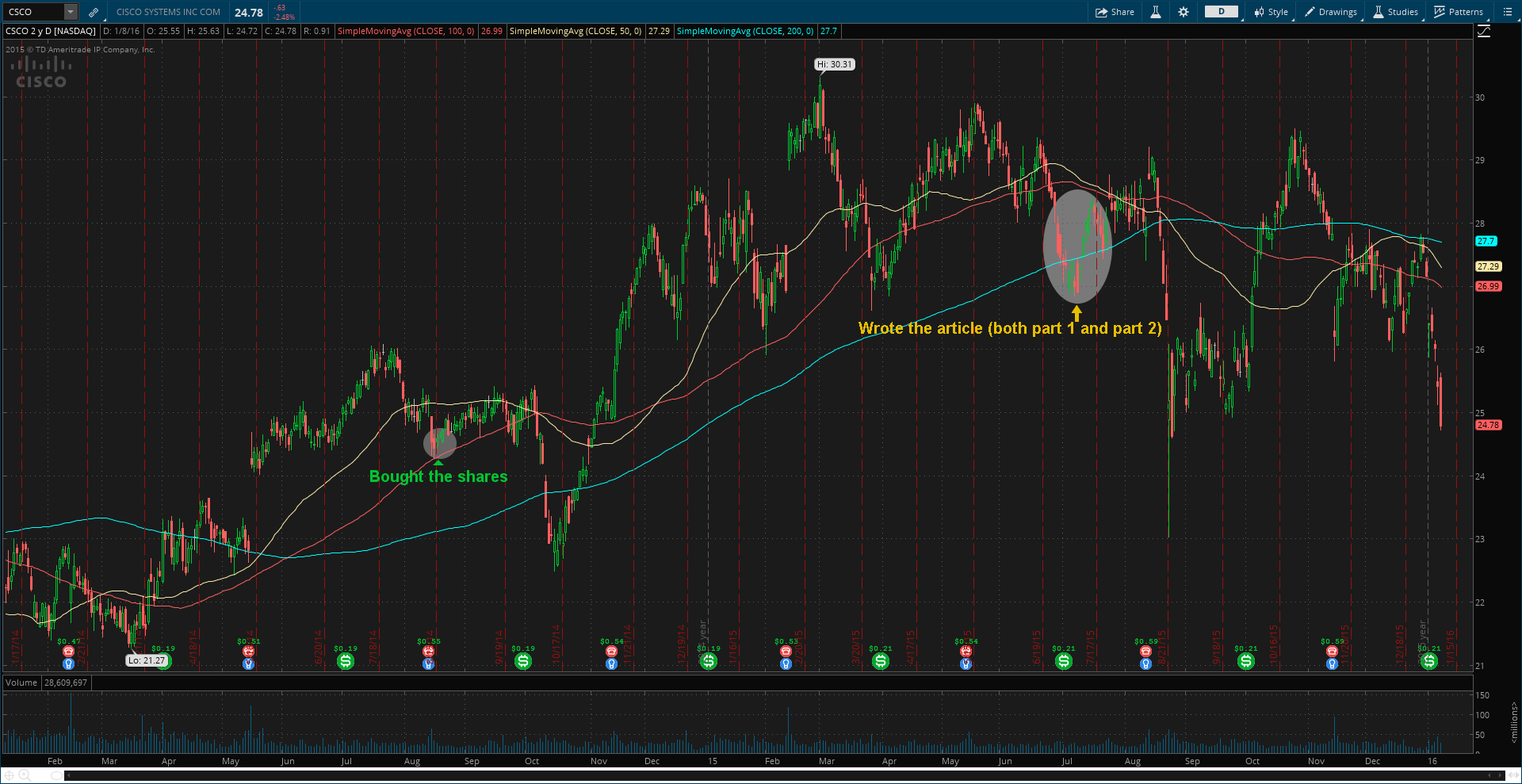

Cisco Systems, Inc. (CSCO) – Daily

Last summer, I wrote about Cisco Systems (NASDAQ: CSCO) (article part 1 and part 2) and believed it was undervalued (it still is). Ever since then, CSCO is down 11.47%, from $27.99 to $24.78 (dividends not calculated). I do own the shares of CSCO. I bought it in August 2014. The average price I own at is $24.73. I’m currently up mere 0.2%. I will take advantage (buy more shares) of lower prices.

Cisco Systems, Inc. (CSCO) – Daily

On November 21, 2015, I wrote about Eli Lilly (NYSE: LLY) and believed it was overvalued (it still is). Since then, LLY is down 3.85% from $85.50 to $81.25 (dividends not calculated). I’m not short on LLY. I cannot afford to short it, due to my capital.

Eli Lilly and Company (LLY) – Daily

On December 26, 2015, I wrote about GoPro (NASDAQ: GPRO) and believed it is a buy (it still is). Since then, GPRO is down 12.10% from $18.34 to $16.12.

Before I go any further, let me tell you what led to Cisco in the first place. I strongly believe in technology and Internet of Things (loT). I believe the market will increase significantly as there are unlimited demand for it and will continue to have unlimited demand.

Cisco’s gross margin, operating income, operating cash flow, and total cash are strong and of course impressive.

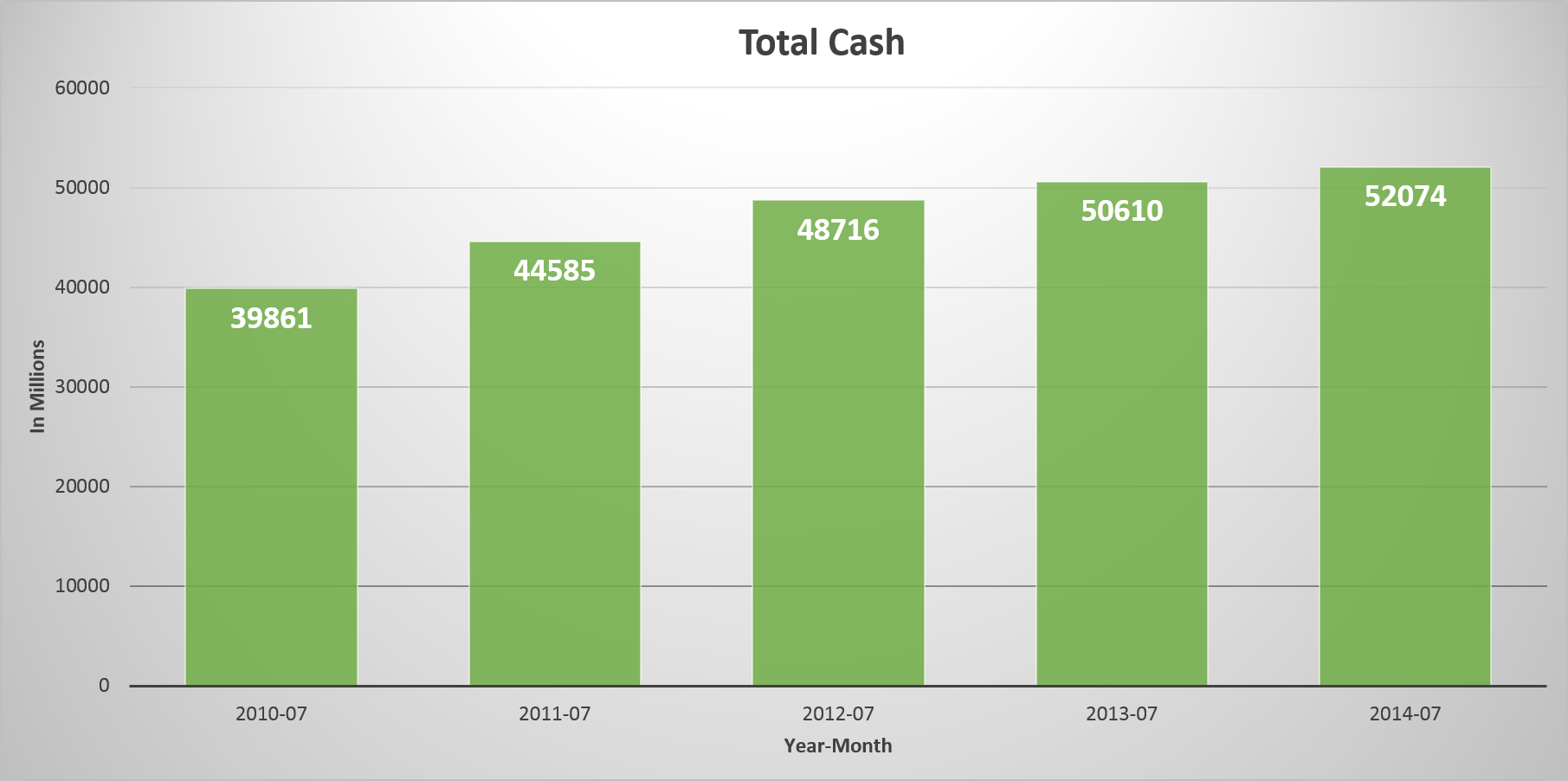

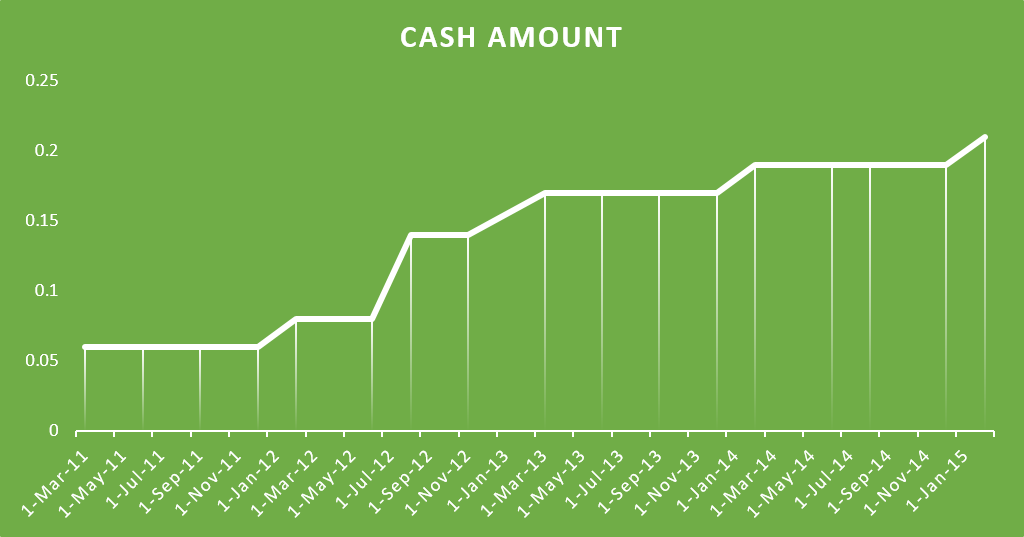

As of April 25, 2015, Cisco had almost $54.5 billion cash on hand. If you look at the “Total cash” chart below (Cash as of April 2015 not shown), you will see that Cisco had slightly over $52 billion cash as of July 2014. In a year, they managed to increase their cash about 5%. Over the last five years (2010-07 to 2015-04), they managed to increase their total cash amount by 36.25%. For company that’s so large and has a market capitalization of $136.9 billion, total cash appreciation is pretty impressive.

Cisco’s Total Cash – Annually

As of April 25, they had current assets of $69.4 and total assets of $106.2 billion. They have total liabilities of $47.4 billion. With strong amount of cash and assets, liabilities are not an issue and should not be in the future as the company continues to trim down liabilities.

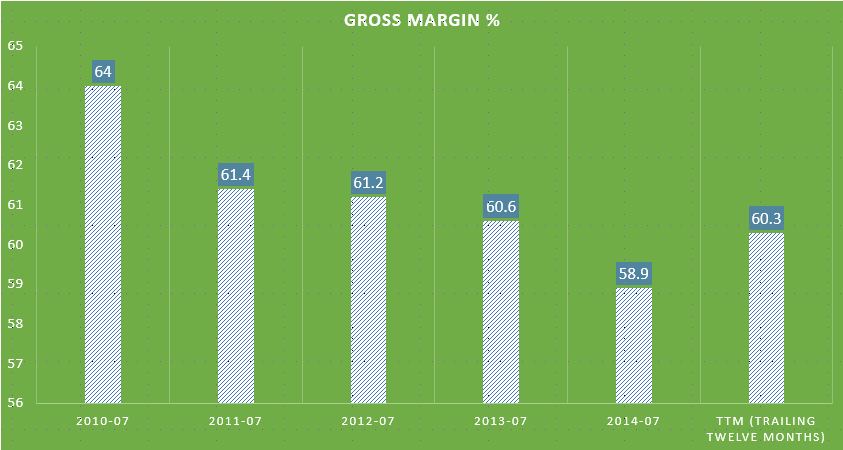

Gross Margin is very strong, although it has declined 3.7% in the last five years (see chart below)

Gross Margin % – Annual (2005 to Present)

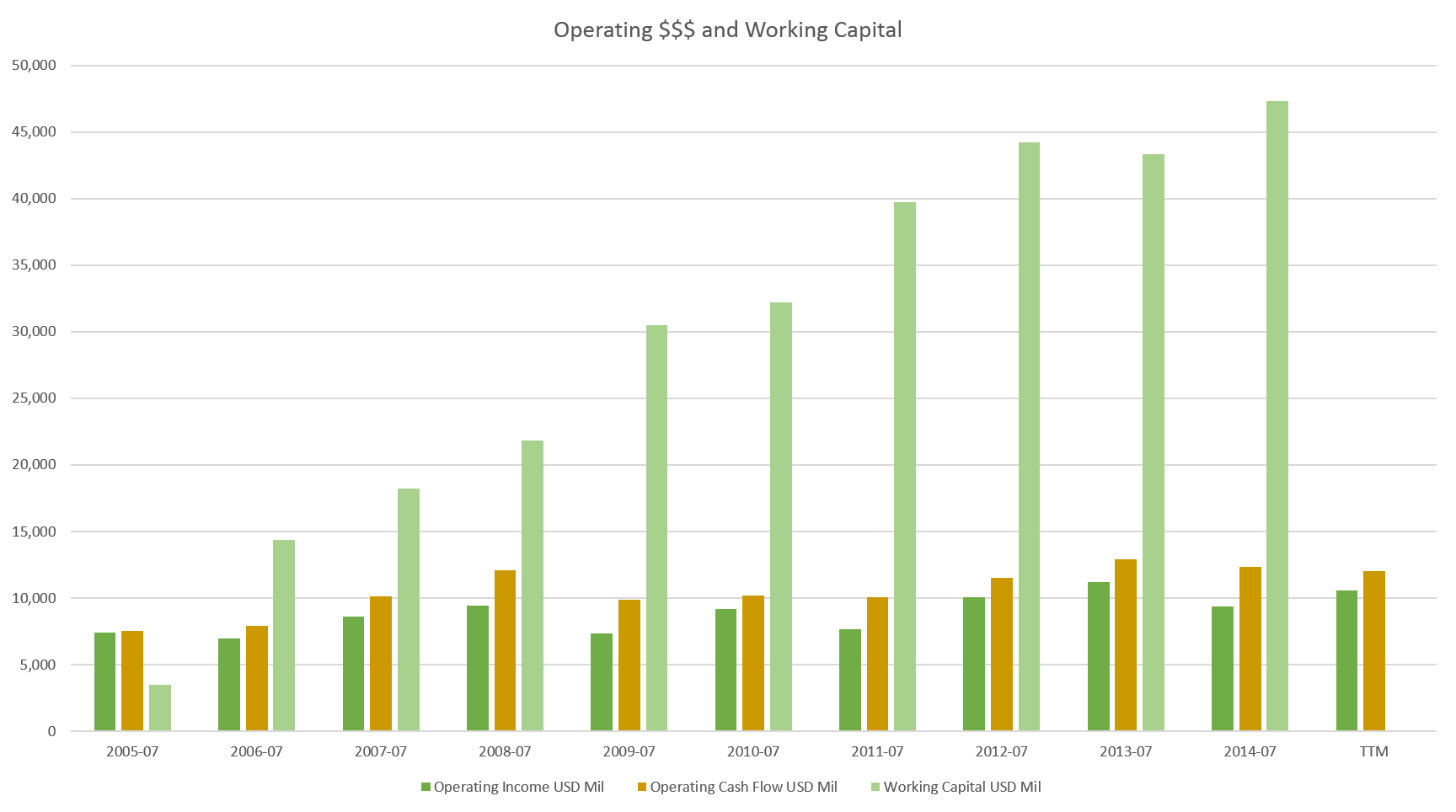

Over the 10 years, operating income has increased significantly while both operating cash flow and working capital has doubled. It shows that Cisco cares about longer-term success instead of focusing on short-term maximization. Long-term investors will benefit from the minds of the management.

Operating $$$ and Working Capital – Annual (2005 – Present)

Comparable Company Analysis:

Below, you see a Comparable Company Analysis chart. I chose one major peer, Qualcomm. The reason I only chose Qualcomm is because all other peers such as Juniper Networks and Palo Alto Networks are too small.

Company Comparable Analysis – One Major PeerCompany Comparable Analysis – One Major Peer

Dividends and Stock Repurchase Program:

During the 3rd quarter of fiscal 2015, Cisco paid a dividend of $0.21 per share, or $1.1 billion. As of today, the divided is still the same. However, it’s expected to increase in the future. They pay a dividend of $0.84 annually, or 3% yield.

CSCO Dividend – 2011 to 2015

In the same quarter, Cisco repurchased approximately 35 million shares of common stock under the stock repurchase program for an aggregate purchase price of $1.0 billion. The remaining authorized amount for stock repurchases under the program is approximately $5.3 billion with no termination date. I believe they will issue new share buyback program after the current program ends, probably in about five quarters if they keep spending approximately $1.0 billion each quarter.

I love that Cisco is aggressively buying back stock. Not only that, but they pay divided to their shareholders which I expect to increase in the future.

Conclusion: From my analysis on Cisco, I have my stock price targets.

By 3rd quarter of fiscal 2016: Net income from 3Q fiscal 2014 to 3Q fiscal 2015 grew 11.74%. Let’s assume, it grows 5% from 3Q fiscal 2015 to 3Q fiscal 2016, net income would be $2,558.85 (in $billions), or GAAP EPS of $0.50 ($0.4971 to be exact). It would be $0.03 EPS increase year-over-year. When Cisco buys back shares, EPS will be higher depending on the amounts of shares purchased back.

Now, let’s assume GAAP EPS for the next 3 quarters stayed the same as 3Q fiscal 2015 which is at $0.47. After the 3Q fiscal 2016, Cisco would have EPS (TTM) of $1.91. At the current share price, the P/E ratio would then be 14.82x. But at this rate of growth, $CSCO would be worth $32, 13% higher than current price ($28.32), at P/E ratio of 16.75x, just 2.82% higher than the current P/E ratio of 16.29x.

My target price might change when Cisco reports 4Q fiscal 2015 earnings on August 12, 2015. I expect better than expected results. US Dollar (greenback) strength might hurt foreign sales. About 40% of their sales are aboard.

Disclosure: I’m currently long on the stock, CSCO. I went long last year at price just below $25. I will continue to be long.

Note: All information I used here such as revenue, gross margin, etc are found from Cisco’s official investor relations site, Bloomberg terminal and morningstar. The pictures you see here are my own.

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.

Cisco is undervalued (target price will be revealed in part 2)

Cisco Systems Inc. (NASDAQ: CSCO) – 5 Year Daily

Cisco (NASDAQ: CSCO) – networking giant – designs, manufactures, and sells networking equipments. Founded in 1984, Cisco has grown exponentially over the years. In May, Cisco announced that Chuck Robbins will be the new Chief Executive Officer (CEO) effective July 26, 2015, replacing John Chambers who will assume the role of Executive Chairman and will continue to serve as the Chairman of Cisco’s board. John Chambers is confident Chuck Robbins will continue the positive momentum. I, too, am confident because Chuck Robbins has a great history.

In the past, Robbins has been Senior Vice President (SVP) of Worldwide Field Operations, SVP of the Americas, SVP of Worldwide Sales, SVP of US Enterprise, SVP of Commercial Business, Head of North American Channels, Group Vice President (GVP) of US and Canada channels, and has been a Director of Cisco since May 1, 2015.

Chambers stated “Chuck’s vision, strategy and execution track record is exactly what Cisco needs as we enter our next chapter, which I am confident will be even more impactful and exciting than our last.” Well, I’m also confident that Chuck will do a great job at Cisco, benefiting shareholders.

For someone who has been committed to Cisco for a long time, and held high level roles, I believe he’s the right person for the job. He will be ethical and care about the longer-term at Cisco, instead of short-term maximization.

On May 13, 2015, Cisco reported third quarter earnings and it was relatively strong. Revenue was $12.1 billion, increase of 5% year over year. Net income was $2.4 billion or $0.47 per share on Generally Accepted Account Principles (GAAP), up from previous fiscal year third quarter earnings of $2.2 billion or $0.42 per share.

Cisco Earnings – Quarterly

Revenue for the first nine months of fiscal 2015 year was $36.3 billion and net income, on a GAAP basis, was $6.7 billion or $1.29 per share, compared with $34.8 billion revenue and $5.6 billion or $1.06 per share for the first nine months of fiscal 2014 year.

In 5-year average, Cisco’s revenue and net income has been growing at more than 5%. For company that is so large, 5-year average growth rate is pretty impressive. Not only revenue and net income are impressive, but also gross margin, operating income, operating cash flow, cash on hand, and dividends.

Note: All information I used here such as revenue, gross margin, etc are found from Cisco’s official investor relations site, and Bloomberg terminal. The pictures you see here are my own.

Disclaimer: The posts are not a recommendation to buy or sell any stocks, currencies, etc mentioned. They are solely my personal opinions. Every investor/trader must do his/her own due diligence before making any investment/trading decision.